Clown Show Continues (April Sleepy Portfolio Update)

“There are decades where nothing happens; and there are weeks where decades happen.”

―Vladimir Ilyich Lenin

Hi everyone,

It’s a busy time in the markets, so I apologize if this monthly update is longer than usual. The first section covers my general thoughts on the markets, and in the second section, I dive into changes to the Sleepy Portfolios and my thought process.

We’re 3 months down and 45 months to go (1,376 days, give or take) into Trump’s second presidency. The saying “it’s a marathon, not a sprint” is apt because we investors have been sprinting hard the last two weeks since “Liberation Day”. But we’ve got a long ways to go still.

And I think the markets have only gotten a tiny taste of the chaos that is to come.

Back in early February, I recommended selling all US assets and have been holding the proceeds in cash. I’d like to be smug here, but even the Sleepy Portfolios have been hit hard (particularly the Canadian portfolio due to its exposure to oil and gas).

The markets continue to hope that Trump will send out a magical tweet (or whatever you call a post on his Truth Social), and all will be well again. But I keep saying there is no putting the toothpaste back into the tube (not that Trump wants to either).

George W Bush once famously said, “Fool me once, shame on me. Fool me twice, shame on me”. And that’s what a lot of international investors, politicians, and citizens are feeling right now (and maybe even some Americans). Most non-Americans thought that once Trump lost in 2020, it would be over and just an aberration.

How wrong we all were!

And this time seems far forse.

Not only does Trump seem determined to blow up the entire world order (which the United States created over the last ~80 years). But he’s also blowing up much of the laws and norms of the United States as well.

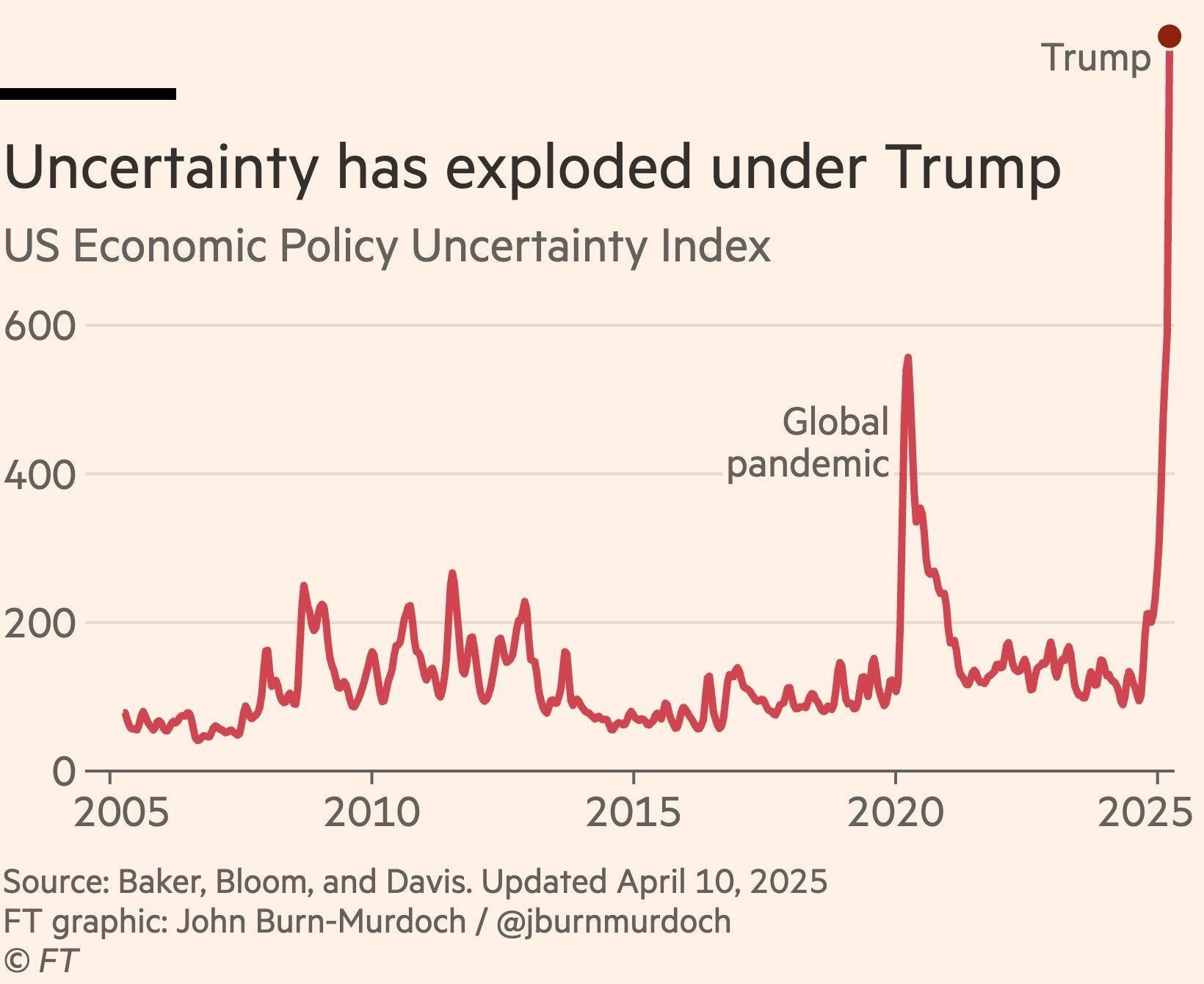

Let’s rewind two weeks to “Liberation Day” and the rollout of tariffs that was a complete farce. Between the nonsense “formula” to justify the tariffs, using ChatGPT to do much of the “work”, and the complete incoherence day to day from everyone within the White House post April 2nd. The only result has been a massive increase in uncertainty.

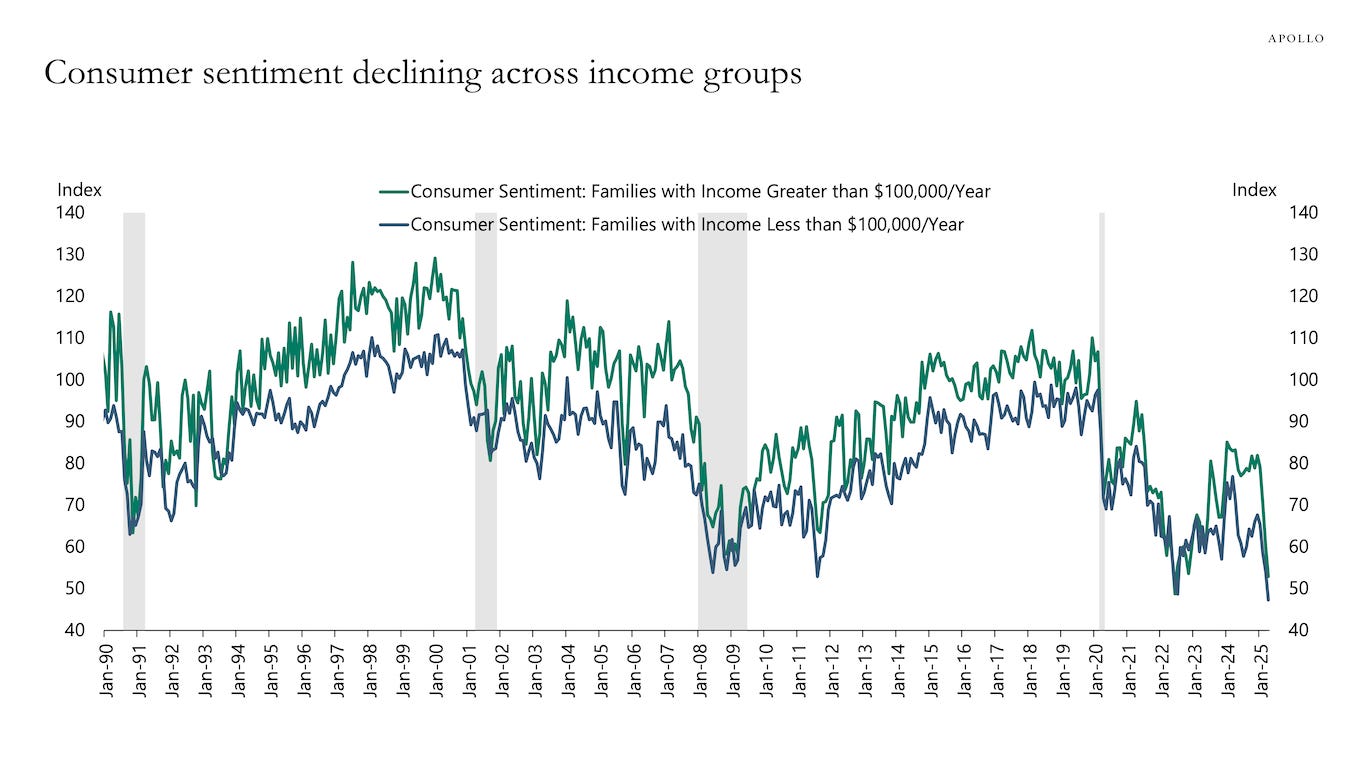

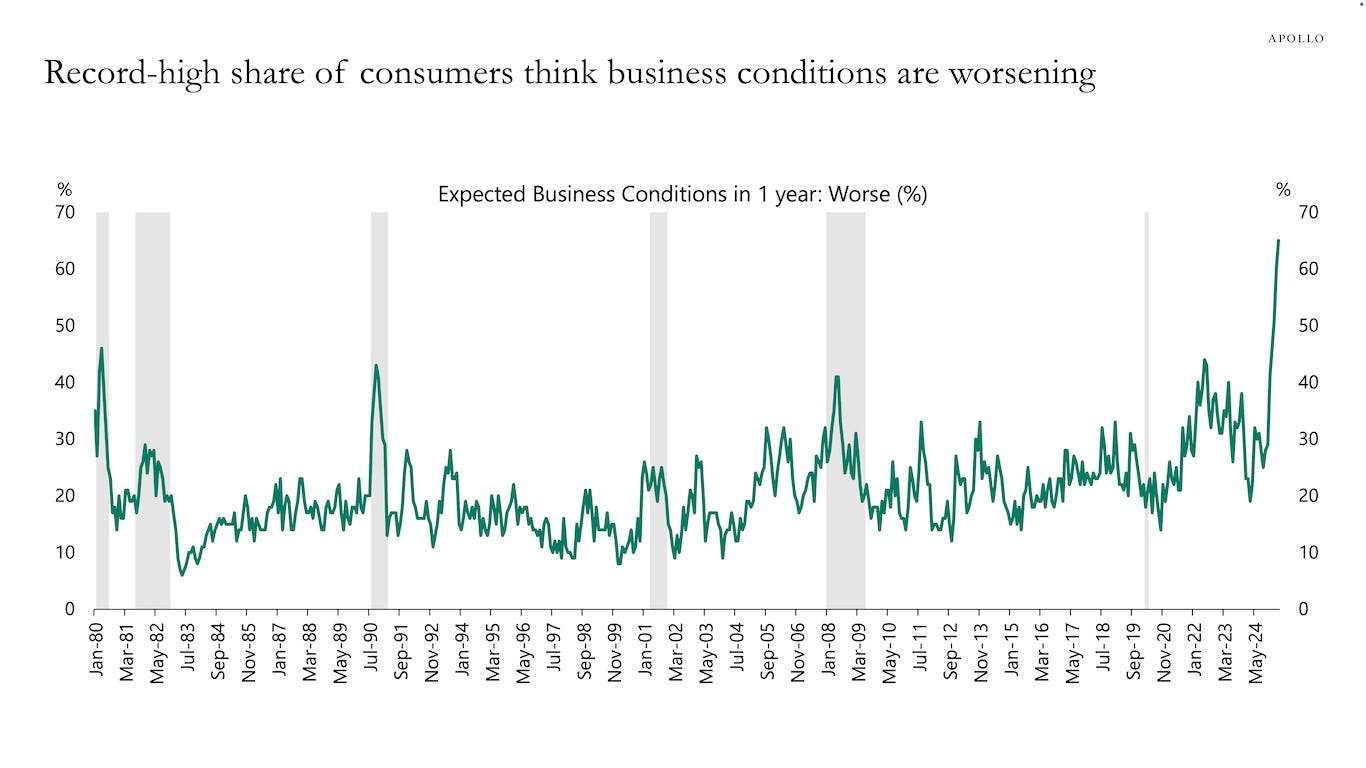

And a big decline in both business and consumer confidence:

Trump is crashing the United States into a recession, but it’s unclear what (if anything) the United States stands to gain. I doubt Trump will keep these tariffs for long. Not because of the “Art of the Deal” but because they would represent the largest tax hike on Americans in history.

But the damage has been done. Whether that’s to international relations. Or to business confidence (many who will now just bunker up and wait out the next 4 years).

To make matters worse. The US budget deficit increases significantly during recessions due to lower tax receipts and automatic stabilizers (such as unemployment insurance, etc.).

The US budget deficit is running at over 7% of the GDP, but once you add recession, we’ll be looking at a double-digit budget deficit. And that’s before all of Trump’s proposed tax cuts (both the renewal of his previous tax cuts plus a whole host of new tax cuts).

And the cherry on top is that the US is already at the precipice of a constitutional crisis.

The markets have focused on the court case of two Democrat FTC Comissioners (Federal Trade Comission) whom Trump fired. Both given its dubious legality but also what it means for other Federal Agencies, particularly the Federal Reserve and Jerome Powell.

But there’s a much bigger case that investors and the market are ignoring. That’s the case of Kilmar Abrego Garcia, a legal resident of Maryland who was illegally deported to El Salvador. The Supreme Court ruled 9-0 that the Trump administration had to bring him back. Not only has Trump refused to do so, but the White House has also tried to spin the loss as some kind of win.

If Trump and the White House will thumb their nose at the courts, including the Supreme Court. What value of the rule of law is there?

Given the trends, this will be one (of many) avenues for a Democrat controlled Congress to impeach Trump in 2027 (and mean more volatility and uncertainty for markets).

And yet the major indices such the S&P 500 are only ~11% off their all-time highs.

What’s even more incredible (for me) is that analysts’ earning estimates still expect significant earnings growth this year.

Here are the NASDAQ earnings estimates for 2025 (orange line), which a buddy pulled for me a couple of days ago:

Analysts are still expecting the NASDAQ 100 to have ~16% earnings growth this year. The ratcheting down of these earnings expectations will be (another) headwind for US equities.

If you assume flat earnings growth and an 18x multiple (closer to historical norms), the NASDAQ is still ~30% overvalued here.

But if we have a recession, earnings probably fall 30% (or more on average), and multiples contract down to some kind of trough of 12x to 15x. It gets really ugly.

I don’t think the markets will fall in a straight line. But instead will slowly bleed out. Similar to when the Dotcom bubble burst (albeit not as extreme), where over a ~2.5 year period, the NASDAQ dropped 80% peak to trough.

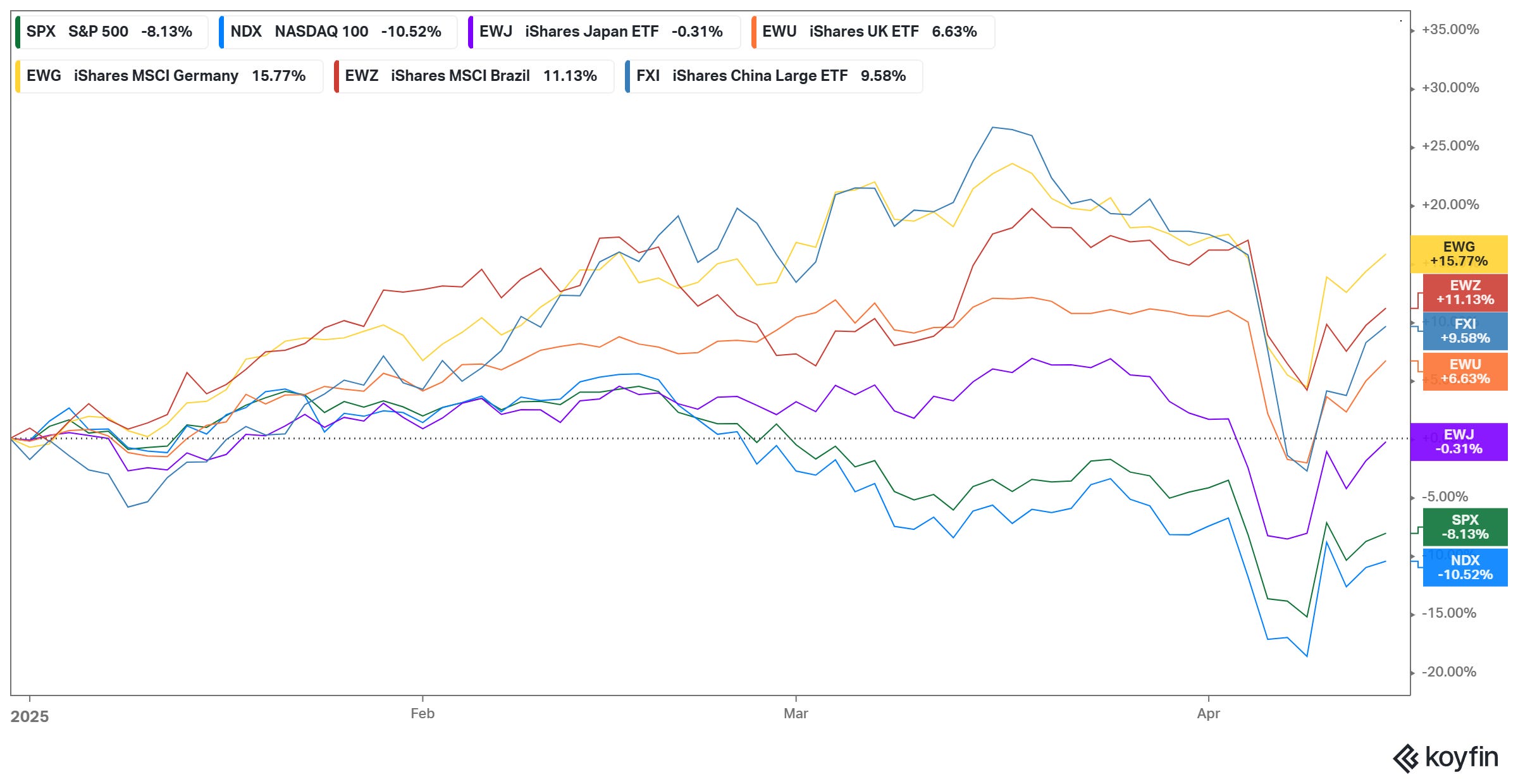

All is not lost. As the saying goes, “there’s always a bull market somewhere in the world”. Investors will start to look beyond the US to put capital to work, and it’s already started.

It was at the beginning of my investing career. But in the 2000s, US equities went sideways for a long time, but international and emerging markets soared.

It looks like something similar is already starting to happen. Year to date, the US dollar has fallen ~10% as capital flees the US and equity markets around the world start to significantly outperform (something we haven’t seen in ~15 years).

Investors big and small pilled into US assets over the last 15 years because they were “the only game in town”. Now the tide is going the other way, and don’t expect it to stop any time soon.

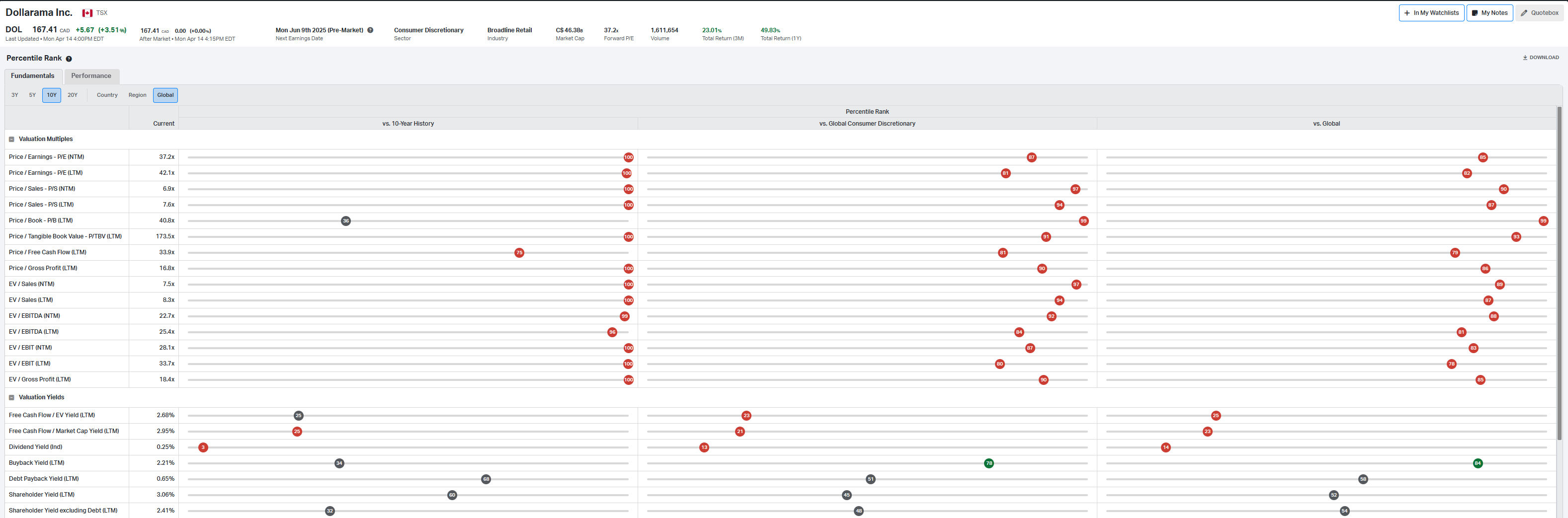

As for the Sleepy Portfolios, let’s start with the Canadian portfolio, which has quite a few changes. First off, I’m selling Dollarama (DOL) and Empire Co (EMP.A). These are great businesses, but far too many investors (especially institutional investors that are required to always be fully invested) are hiding in consumer staples, and the valuations have become extremely stretched.

The valuations are extremely rich, not just versus their history but also against the broader market. Koyfin has a handy tool, and using Dollarama as an example and we can see just how expensive it is.

So that leaves the Canadian portfolio with roughly 20% cash. I’ll be adding 3 new names: Equinox Gold (EQX), Hammond Power (HPS.A), and Tourmaline Oil (TOU).

All the gold miners have had a decent run (although they’ve underperformed gold), so it’s hard to buy, but with gold prices continuing to rise and oil prices declining (diesel is the #2 or #3 largest expense) I think there’s still a lot of upside potential in gold miners long-term.

Hammond Power is a small electrical manufacturer in Canada specializing in transformers across Canada, the US, and India. Transformers have a 3+ year backlog, so the business is probably as close to immune to tariffs as there is. And significant stimulus spending in Canada should benefit them.

The third addition is Tourmaline needs no introduction as it’s been in the portfolio before. But natural gas prices have hardly been impacted by the sell-off. LNG Canada will be coming online within months and should give all natural gas producers a huge lift.

Lastly, I’ll be increasing the weight in Canadian Natural Resources (CNQ) to 10%. I know a lot of investors have been disappointed with its performance recently. But I think the shares just got too expensive for a while.

And now that it’s the largest E&P in Canada, it’s also become something of a liquidity sponge. Great during the good times. But in the bad times, people “sell what they can, not what they want to,” and CNQ is now on that list. CNQ has also quietly become the 2nd largest natural gas producer in Canada and will likely see an even greater benefit from LNG Canada than Tourmaline.

For the Global Portfolio, I’ll be adding Komatsu (KMTUY) and Ecopetrol (EC), which I wrote about last month. But I’ve changed my mind about Novartis. There’s just too much news flying around of countries threatening to void or ignore patent laws to start buying pharmaceuticals (at least for me). So I’ll be picking up shares of Gold Fields (GFI).

Finally, I’ll be rebalancing the portfolios to top up all of the oil and gas positions on the Canadian side. While in the Global Portfolio, I’ll be topping up the mega-cap miners BHP & Rio Tinto as well as TotalEnergies with the remaining cash.

Thanks for reading, and stay safe in these crazy markets!

Trades

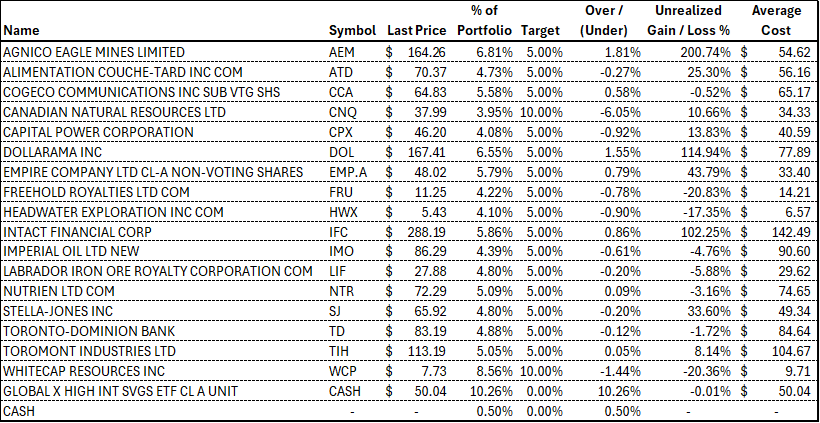

Canadian Portfolio

Sales:

Dollarama (DOL)

Empire Company (EMP.A)

Buys:

Equinox Gold (EQX)

Hammond Power Solutions (HPS.A)

Tourmaline Oil Corp (TOU)

Top up to target:

Freehold Royalties (FRU)

Headwater Exploration (HWX)

Canadian Natural Resources (CNQ)

Whitecap Resources (WCP)

Trims to target:

Agnico Eagle (AEM)

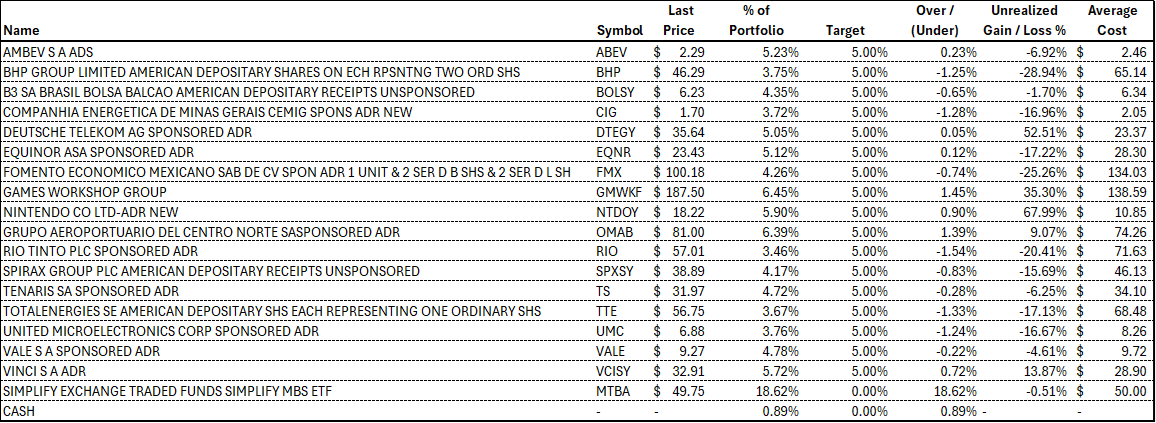

Global Portfolio

Sales:

Simplify MBS ETF (MTBA)

Buys:

Ecopetrol (EC)

Gold Fields Limited (GFI)

Komatsu Ltd (KMTUY)

Top up to target:

BHP Group (BHP)

Rio Tinto (RIO)

TotalEnergies (TTE)

Portfolio Holdings

Canadian Portfolio

Global Portfolio

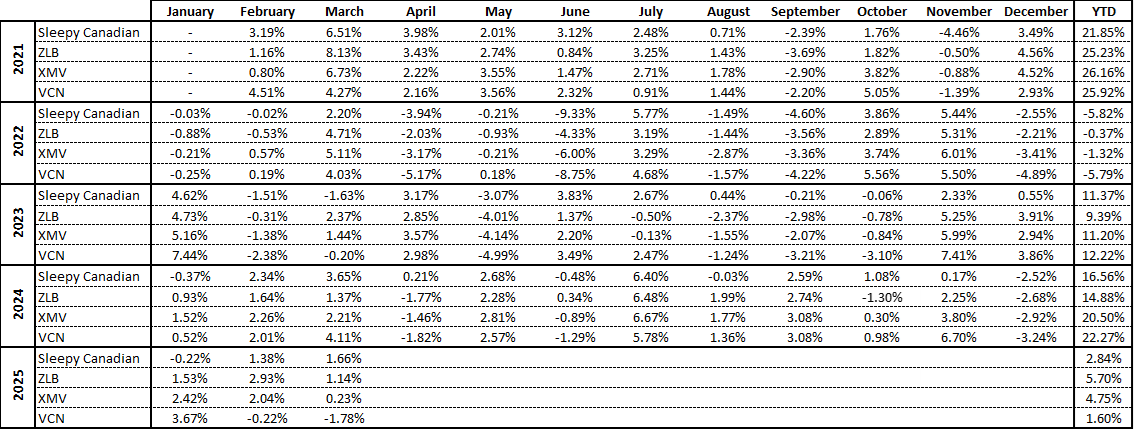

Performance

Canadian Portfolio

Global Portfolio

Disclosure: I am long and have a beneficial interest in all of the above-mentioned securities. I may change my holdings at any time post-publication.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor, and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.

Hi Jonatan. Have you written about EQX before, or could you point towards a note that influenced your decision. tx