Company Highlight - Winning With Whitecap Resources

Company Highlight - Winning With Whitecap Resources

Summary: Whitecap Resources is a Canadian mid-cap oil and gas company with operations in Alberta and Saskatchewan. The reasons I like the company are the following:

High-quality management team that has consistently done what was best for the company's (and shareholder’s) long-term interests.

Has a ~5.3% dividend yield, repurchasing ~60bps a month of shares (~7.4% annualized) and guiding to grow production organically by 12% this year and 5% to 8% over the next 5 years.

Management and corporate insiders have a significant financial stake in the company and regularly purchase additional shares in the open market with their own funds.

Large untapped inventory of oil and gas reserves with low decline rates and negative Scope 1 & 2 emissions.

A long history of consistent per-share growth in all of the important metrics: production, profits, free cash flow, and dividends.

Hi everyone,

Two months ago I discussed becoming bullish again on oil (which you can find here). I guess I top-ticked the short-term move because right after publishing WTI crashed down to the low 70s. And then there was a banking crisis and WTI crashed further down to $65.

I remain bullish on oil and gas over the next 3-5 years and reiterated my bullishness with an update two weeks ago (which can be found here). WTI is now solidly back above $80/bbl and we’ve seen some absolutely massive oil & product draws in recent weeks (historically we would be building inventories ahead of the summer driving season).

So while the first little bit of the run has already played out, I still think there’s plenty of upside still to be had. Of course, if we do end up having a deep recession then all bets are off. But until then I think the short & medium-term trend is up.

So I thought now would be a good time to highlight one of my favorite energy companies.

(Full Disclosure: I am long and have a beneficial interest in Whitecap Resources at the time of writing this).

What is Whitecap Resources and why is it a company you should consider?

Whitecap Resources is a Canadian mid-cap oil and gas producer with production in Alberta and Saskatchewan. The company is exceptional in a number of ways.

The company’s management team, led by its founder, president & CEO Grant Fagerheim, is very high quality and has a long record of doing what’s in the shareholder’s (long-term) best interests.

Second, the company has negative Scope 1 & 2 emissions. This is thanks to their largest oil field, Weyburn, which is an EOR (enhanced oil recovery) play in Saskatchewan. Whitecap purchases CO2 (much to their chagrin) from a local coal power plant and pumps it underground to recover oil and gas (Whitecap has a full explanation here).

Third, the company has been an aggressive acquirer of other E&Ps and energy assets during the tough times (“buy when there’s blood on the streets”). And has a track record of successfully integrating them into the company.

Since the Covid-induced oil crash, Whitecap has acquired privately owned NAL Resources and XTO Canada as well as the publicly listed TORC Oil & Gas and Kicking Horse Oil & Gas.

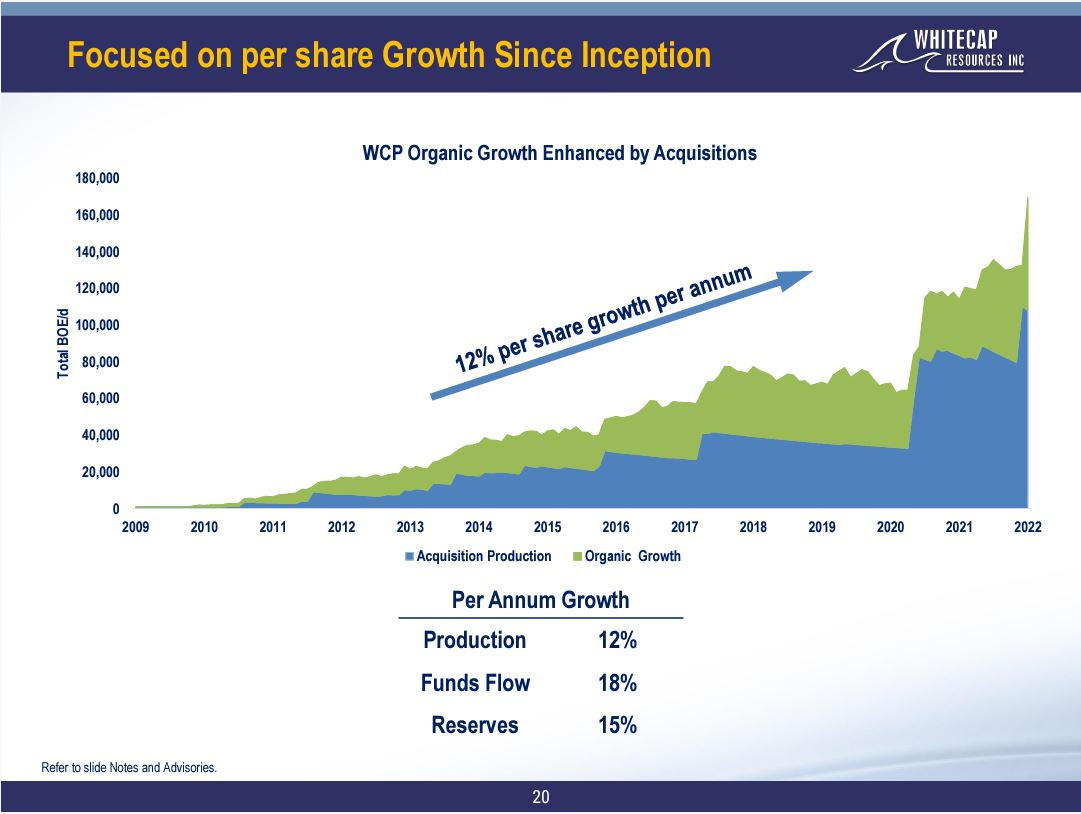

The net result is that Whitecap’s production has grown from 74,650 boepd at the end of 2019 to 166,390 boepd at the end of 2022 (~30% CAGR over 3 years). Meanwhile, outstanding shares have only grown by 14% CAGR.

So on the metric that matters the most, per share, Whitecap’s production per share has been about 15% CAGR over the last 3 years. You might think that this is an aberration but it’s only slightly higher than their 10+ year operating history.

After 2023, Whitecap is only projecting to only grow production by 5% CAGR organically (i.e. without acquisitions). But combined with a modest amount of share repurchases, investors should still see high single-digit per-share production growth.

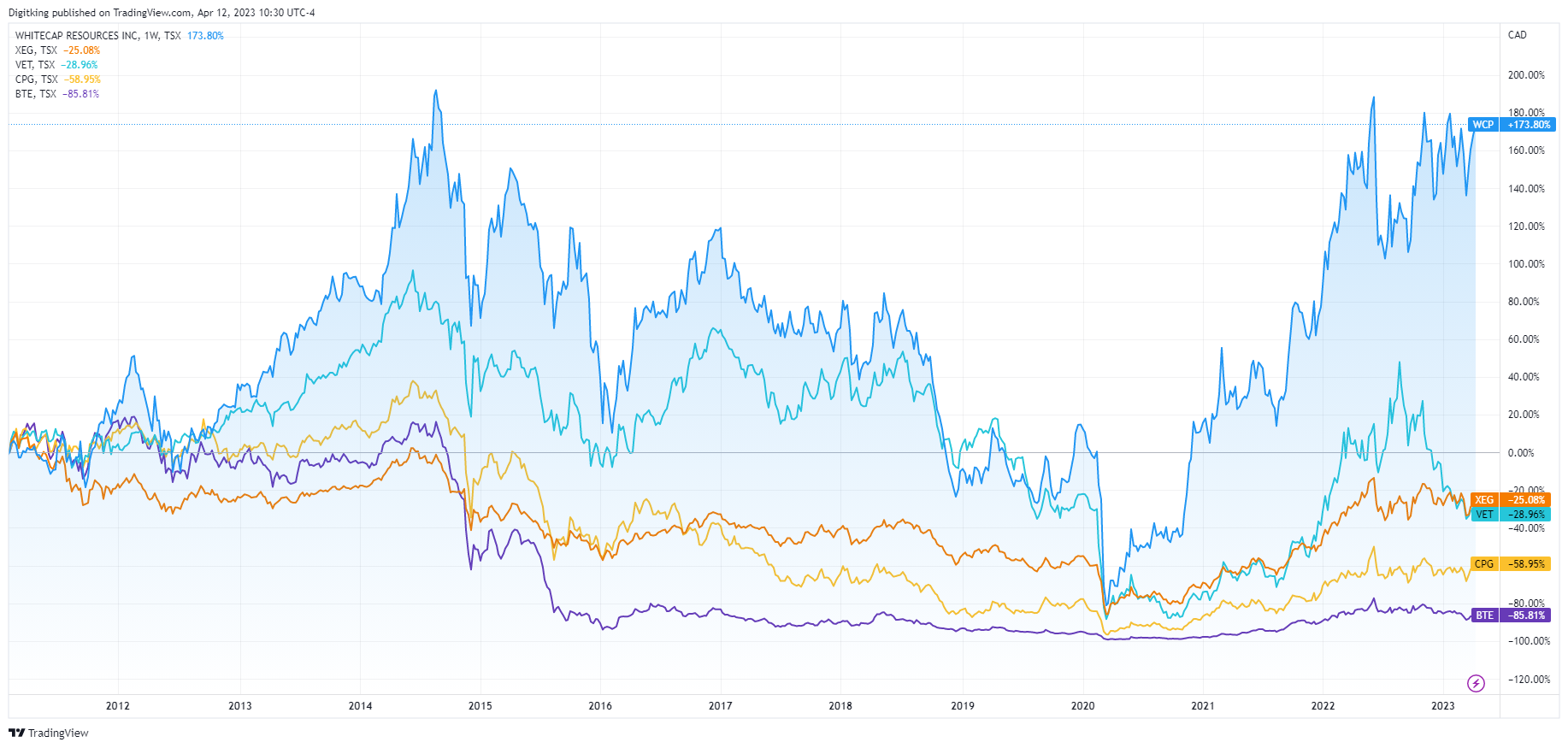

Over the long term, investors have rewarded the company handsomely. Here is a chart of Whitecap’s total return (in blue) versus the energy index (XEG - orange line) and a couple of its peers; Vermilion (teal), Crescent Point (yellow), and Baytex (purple).

However, on a more recent (and shorter time frame) Whitecap’s share price hasn’t experienced the same kind of outperformance. Here is a chart for the last 2 years:

Why has Whitecap underperformed? I think it largely comes down to two reasons.

First, the current crop investors in oil gas are predominantly retail investors and hedge funds. And they want one thing above all else. And that’s capital return (although it’s hotly debated whether that should be in the form of dividends or share buybacks).

Whitecap has been a laggard on this front. The company has steadily increased the dividend and has spent ~$416mm repurchasing ~52mm shares (approximately 8.5% of current shares outstanding) over the last two years. But for many, this hasn’t been enough (and has trailed many of its peers).

The second reason and somewhat related to the first is the company’s purchase of XTO Canada which was announced last June and closed in August.

The company purchased XTO Canada for $1.9 billion of cash (although the cash came from debt). The deal was massively accretive to shareholders (although it was based on commodity prices that are higher than current spot prices).

But many investors were not thrilled.

First, it further delayed capital returns. However, the company is forecasting that it will hit its net debt targets by this summer so this is a problem in the rearview mirror.

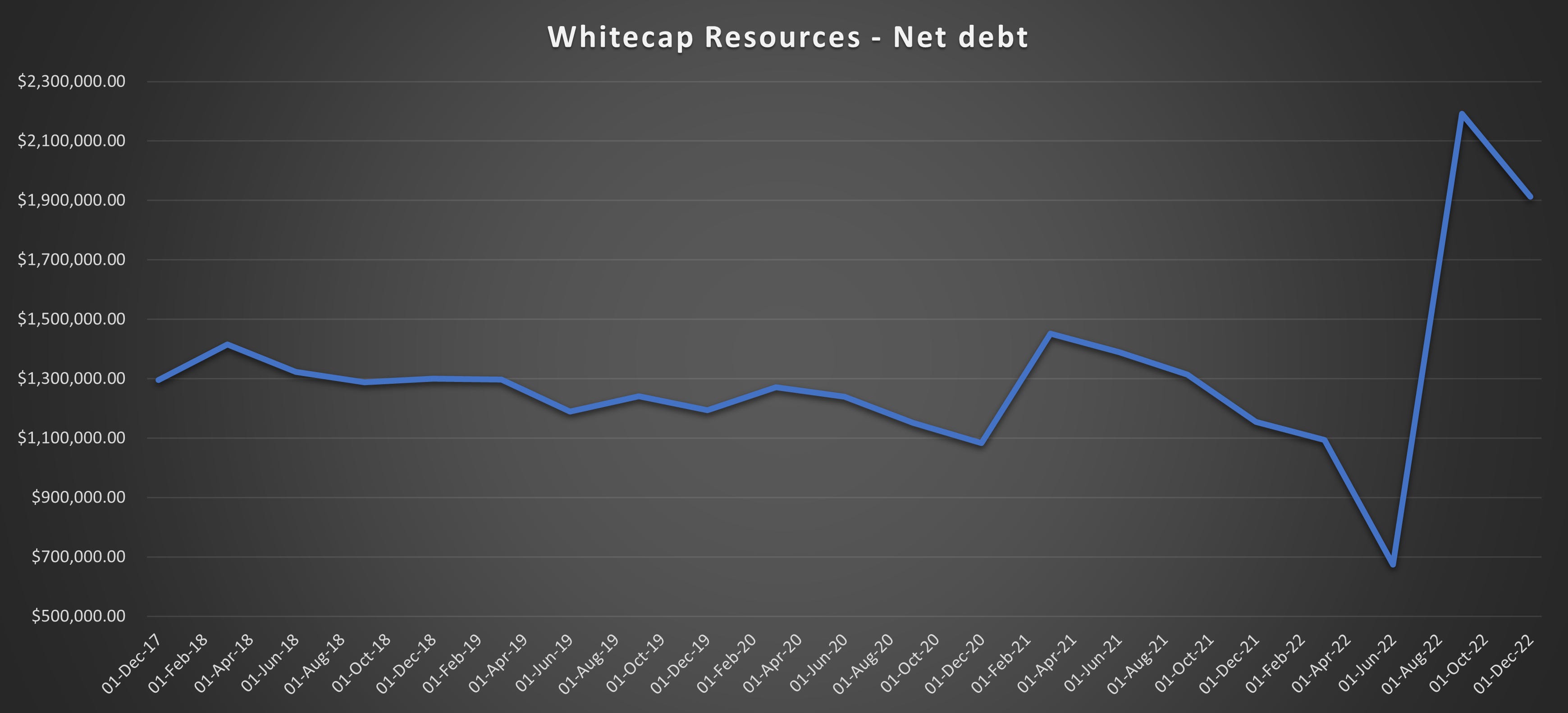

Second, the deal added a lot of debt to the company’s balance sheet. Many investors and energy executives are still scared by the Covid crash and now loath debt. While Whitecap’s net debt looks to be high by historical standards:

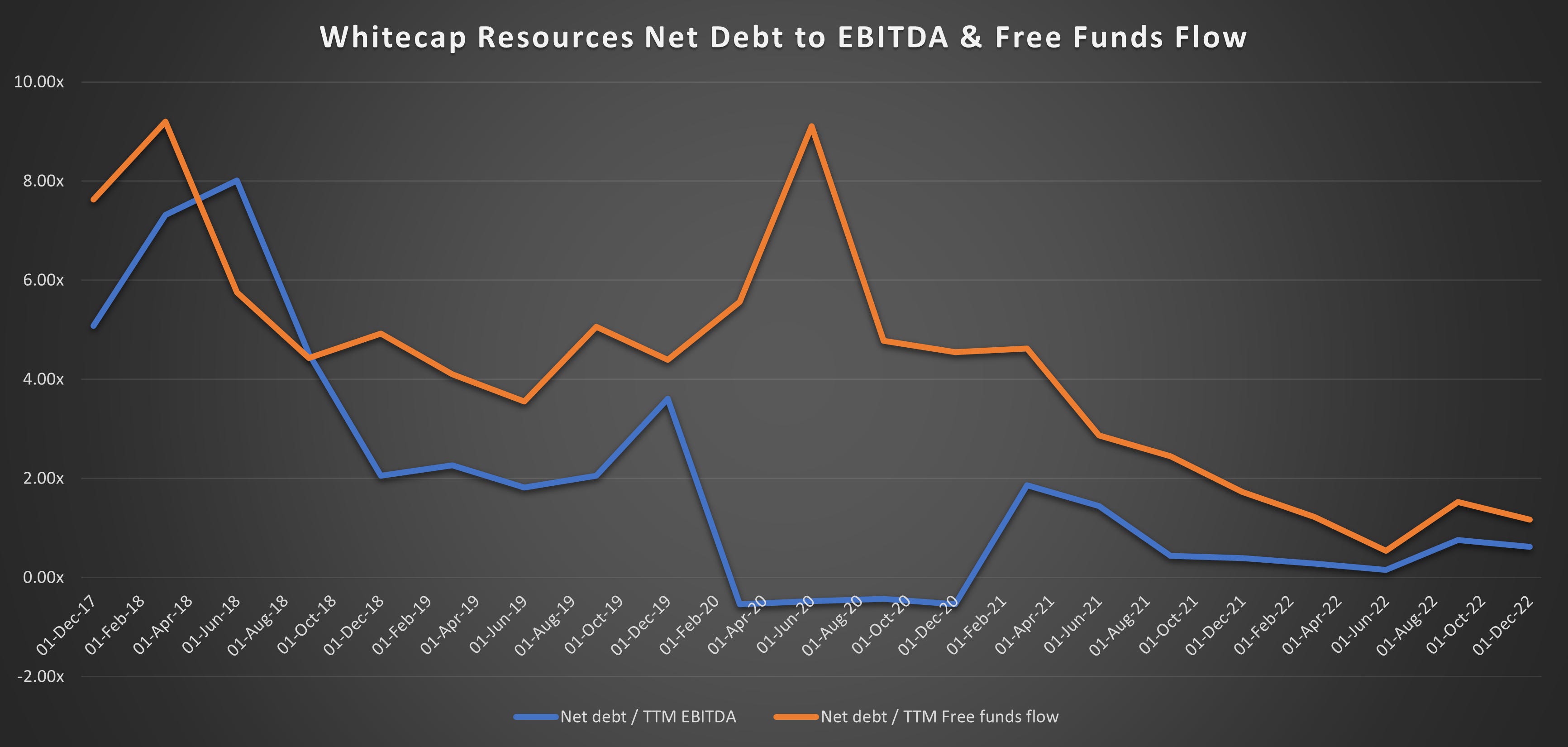

But Whitecap is a much, much larger (and more profitable) company today so its capacity to carry debt is significantly higher. Here we can see Whitecap’s net debt to EBITDA (which is used for debt covenants) and Free Funds Flow (the industry’s standard for calculating free cash flow). As you can see, both are at 5-year lows (net debt / TTM EBITDA went negative in 2020 due to losses):

So when taking a step back, we can see that Whitecap’s debt levels shouldn’t be much of a cause for concern.

The last issue with the XTO acquisition is that it has shifted Whitecap’s production mix more towards more gas and NGLs (natural gas liquids) and away from oil. For instance, they assumed a C$4.50/GJ AECO nat gas price for assuming accretion at the time the deal was announced. But nat gas prices have collapsed due to the extremely mild winter (AECO is currently just over $2).

But the XTO Canada acquisition highlights why I think Whitecap is such a great long-term investment. Grant and the rest of the management team have always done what they believe to be in the company’s best long-term interests.

So yes, natural gas prices have dropped by half since the acquisition closed. But long-term I think the trend is up for North American natural gas prices. As more LNG export facilities come online both along the Canadian West Coast and the US Gulf of Mexico, I think that nat gas prices will slowly converge with the rest of the world.

I doubt we’ll see gas prices sustained above $9/mcf but if prices remain consistently in the $5 or $6 range then it’ll make the XTO acquisition will turn out to be extremely rewarding to shareholders.

In the recent Q4 conference call, Grant also discussed that Whitecap is now a significant nat gas producer, they were investigating whether they could pursue a similar marketing deal that Tourmaline signed with Cheniere Energy (a large US LNG company).

The details of the Tourmaline deal can be found here. But short, Tourmaline obtains JKM (Japan Korea market) nat gas pricing less the cost of pipeline transport and LNG liquefaction & shipping costs. The result is that Tourmaline is receiving a substantial premium over North American gas prices.

Whitecap now has enough natural gas production, long-life assets, and a negative emissions profile for it to be a prime candidate to partner with an LNG export company.

I wouldn’t count on it, but if it did happen it would definitely be a unexpected upside that nobody has priced into the company.

Risks & Drawbacks of Whitecap

So what are the drawbacks of Whitecap? I think they can be summarized as followed:

Recession: Needless to say, but if you do think we’ll be faced with a recession, and in particular a deep recession. Then anything energy related is going to get crushed. I’m still in the camp that the recession will likely be very mild and mostly a white-collar recession (much like the Dotcom bust).

Torque: If you want the most bang for your buck exposure to rising oil and gas prices, Whitecap won’t do it. Whitecap is much more of a compounder/GARP (growth at a reasonable price) kind of company. It’s worked over the long term, but if oil prices rise to $100 or $120 a barrel by the summer, I don’t see Whitecap leading the pack (in terms of share performance). For a lot of current energy investors, they seem to want the most possible upside and Whitecap just doesn’t tick that box.

Capital Returns / Investor Base: As I mentioned above, most investors currently focused on energy equities want capital returns first and foremost. Whitecap is starting to play catch up but keeping the door open for more long-term accretive deals. If the company finds an acquisition that they feel is compelling enough, it will likely go and make the deal regardless of the short-term share price performance and complaints of shareholders.

Lack of US listing: Many US investors can’t invest in OTC securities and this hurts Whitecap as most of their peers (VET, BTE, CPG, etc.) have listings on the NYSE. I’ve asked management about this in the past but it’s never been a priority for them.

Wrapping it up

In conclusion, Whitecap is a very high-quality oil and gas company that is led by a top-tier management team. The company’s shares, like its peers, are very cheap (even in a world of $80 oil) and the company has a long runway of accretive growth ahead of them.

Recession fears are currently putting a lid on oil prices and energy shares, but I believe that if you can look past the next 12 to 18 months than Whitecap has a very bright future.

Disclosure: I am long and have a beneficial interest in all of the above-mentioned securities. I may change my holdings at any time post-publication.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.