Digging through the debris of Canadian REITs

Digging through the debris of Canadian REITs

NOTE: This article discusses Canada Real Estate Investment Trusts (REITs). They are structured as either open-ended or closed real estate mutual fund trust. Therefore if you are not a Canadian investor, please carefully consider the tax implications and/or consult with a tax lawyer or accountant before investing.

Hi everyone,

I haven’t written much lately as I’ve been busy digging through all of the Canadian REITs. The sector caught my attention because there’s been a lot of doom and gloom for real estate (and a lot of bellyaching about returns). This made me reminiscent of the energy sector back at the COVID-19 lows back in 2020.

But the more and more that I dug, the less it resembled the energy crash of 2020 and the more it reminded me of the energy crash in 2014 (the first of many).

There’s value to be had investing in REITs right now, but I think you need to be very selective.

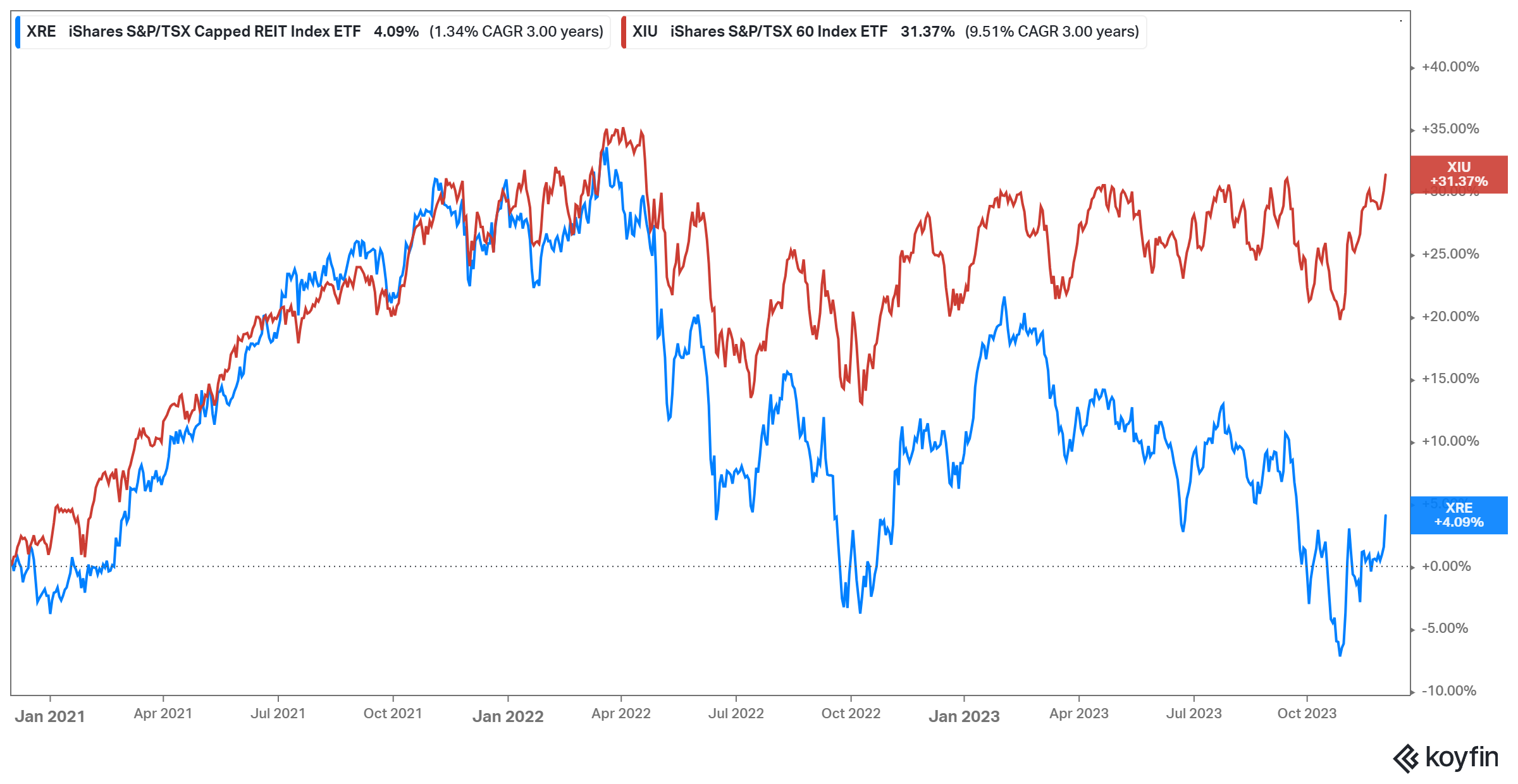

The sector’s returns have frustrated investors. But to me, it doesn’t seem that bad all things considered. Over the last 3 years the REIT sector, using the iShares REIT Index ETF (XRE), has managed to squeak out a positive nominal return. Admittedly it’s underperformed XIU (our version of SPY).

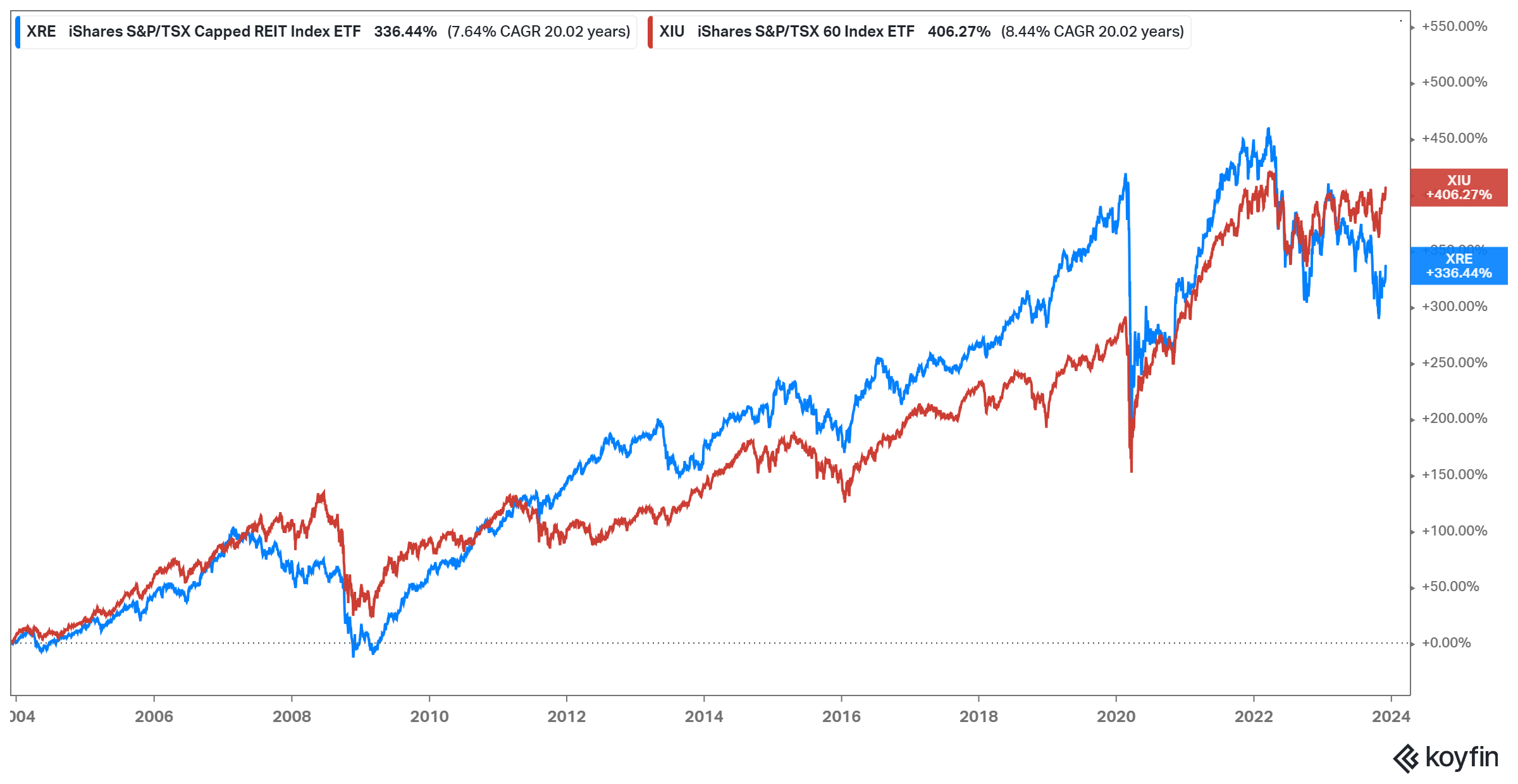

Not great, but if you zoom out you can see why it’s felt so bleak for public real estate investors. Up until Covid, the REIT sector handily outperformed the broader Canadian markets. I guess a couple of years of underperformance feels like a lifetime?

Rising property values and declining interest rates were rocket fuel to the sector. But all of that has changed post-Covid. To make matters worse, it doesn’t seem like most REIT management teams have gotten the memo.

I think over the medium term (3 to 5 years), I think there’s going to be a lot more pain to come for REITs. But I think this is also a great opportunity for smart REIT management teams that can use the “chaos” to their advantage to make accretive acquisitions and set themselves up nicely for the next decade. And by extension, I think that’s good news for active stockpickers.

Valuations are depressed

There’s already been a lot of pain and that can be seen in the big drop in valuations.

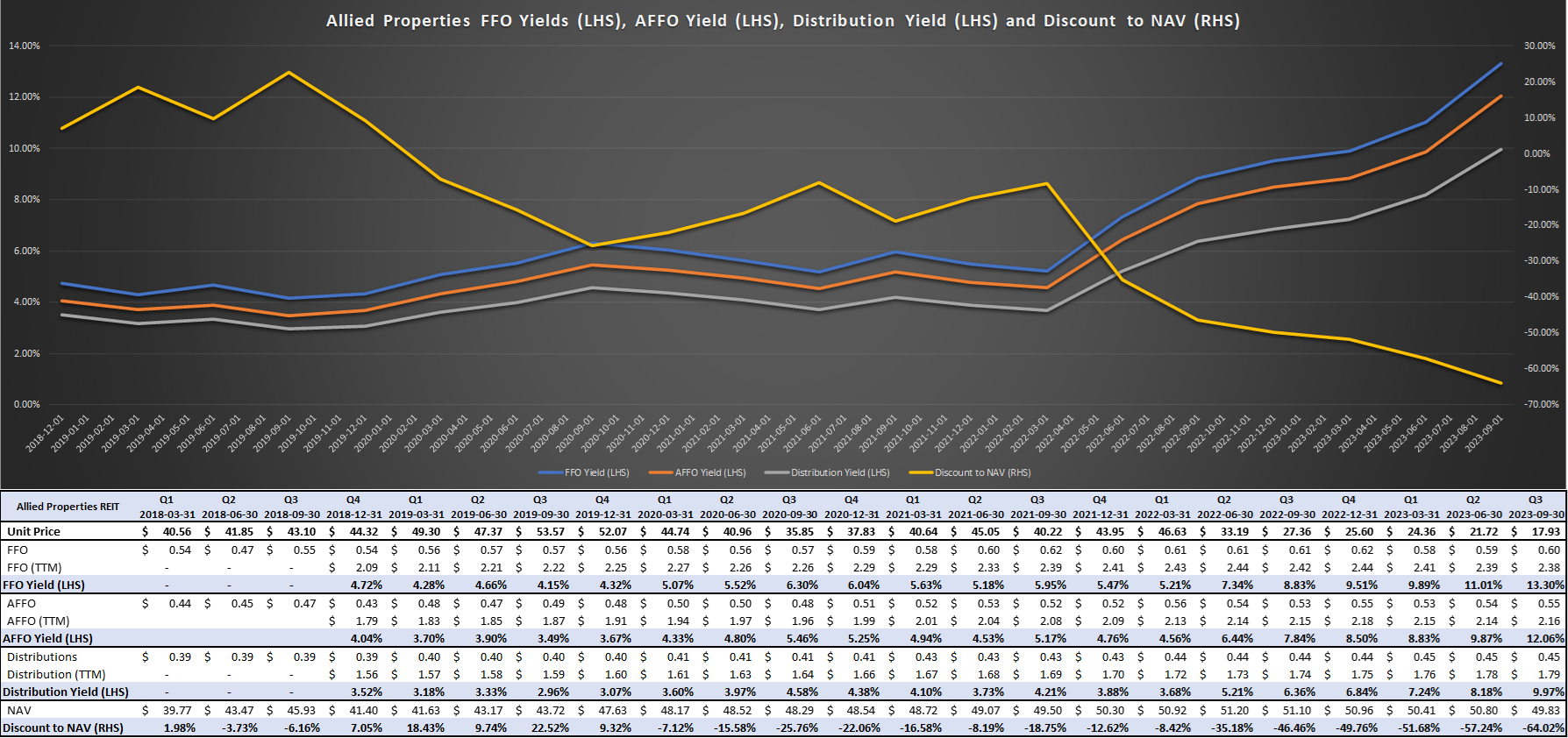

Many REITs used to trade at a premium NAV (net asset value) and 3% to 4% cash flow yield (using FFO & AFFO).

The extent of the collapse in valuations has ranged. At one end are REITs like Allied Properties which once traded as high as a 20% premium to NAV and now trades at a ~65% discount to NAV (I’ll have more to say about them later on).

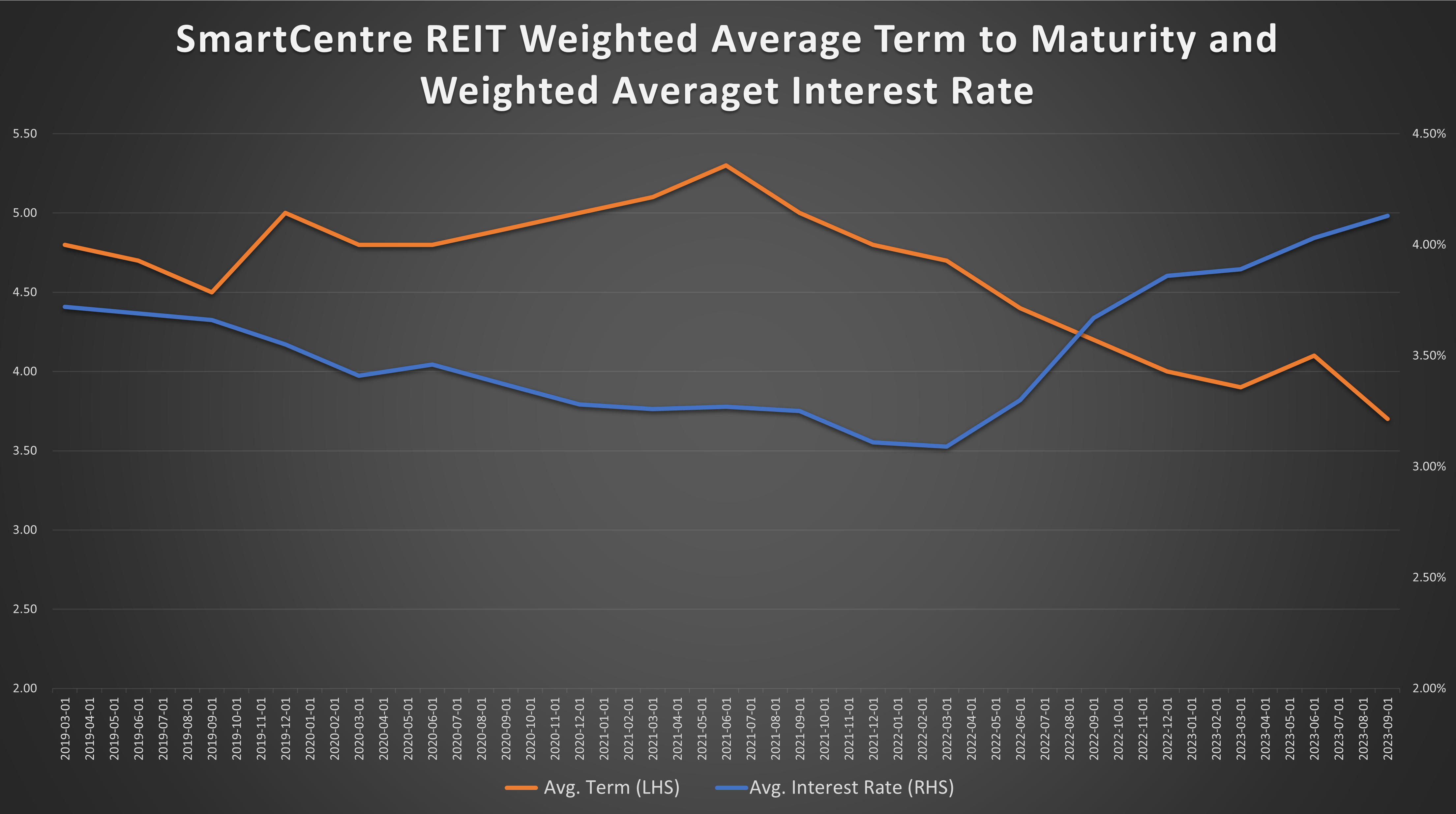

Even well-run REITs with prudent capital allocation and rock-solid balance sheets have seen their valuations get squeezed too. One of the best REIT operators is SmartCentre REITs and they too have been affected (although not nearly as badly):

Why have valuations crashed over the last couple of years? There are two reasons often cited, although after reviewing the data only one of them matters (at least to me).

Occupancy fears are overblown

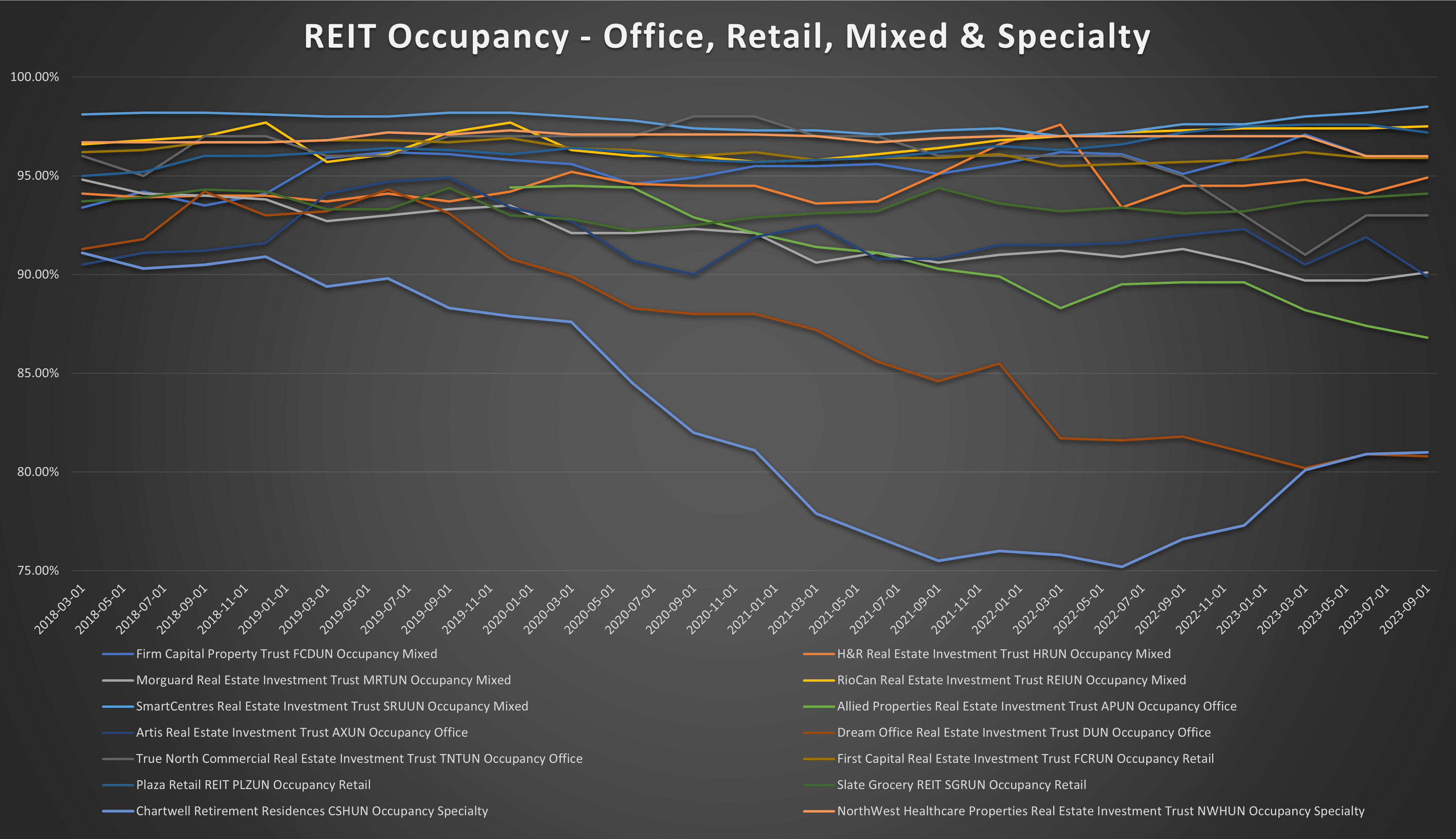

The headlines are full of doomsday stories about empty offices and buildings but I’m not seeing it in the REIT regulatory fillings. Some REITs have been harder hit than others. And those with large exposure to the Toronto office market are especially pronounced. But other than that, occupancy rates have been stable.

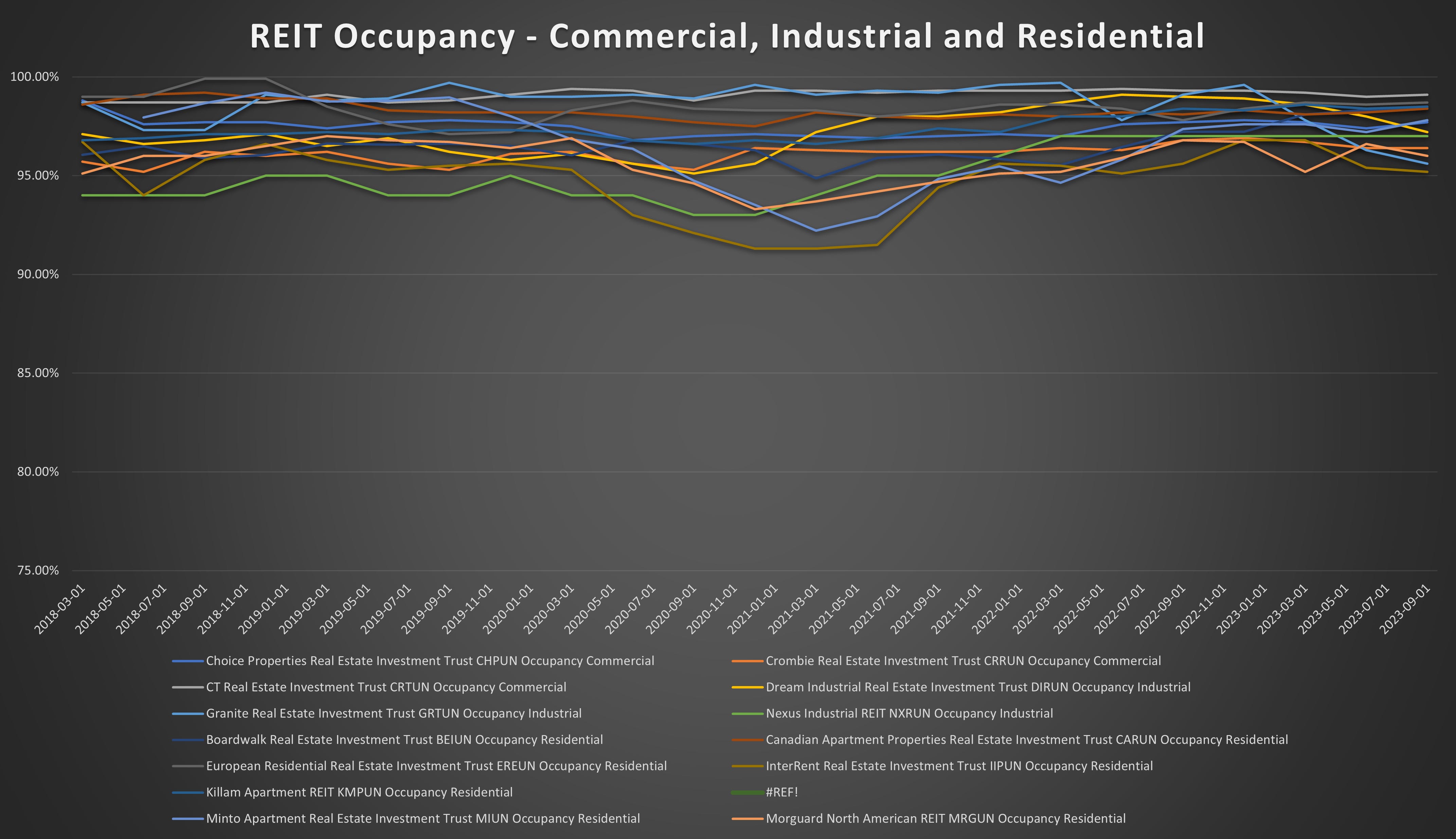

I broke the occupancy into two groups. The first group is office, retail, mixed (what I call REITs with exposure to everything), and two specialty REITs.

Chartwell, which provides retirement homes and long-term care facilities was the hardest hit by Covid-19 out of any REIT and they are slowly bouncing back.

Meanwhile, Dream Office REIT is in serious trouble while Allied Properties and Artis continue to struggle due to their exposure to Toronto office space. But for the rest of the group, occupancy has been pretty stable.

With employers now requiring employees to return to the office for at least 3 days a week, I think this will become a big boost for occupancy rates. But at the same time, there’s a “white-collar recession” going on with lots of layoffs in tech and finance that will be a drag (particularly in Toronto).

But even with all that doom and gloom, almost all of the REITs that I’ve reviewed have been able to increase rents by 5% (or more) annually over the last couple of years. Even in the struggling office sector.

In the other group, I have commercial, industrial, and residential. And there’s no signs of trouble anywhere to be seen.

So while there are challenges in some markets for some REITs, I think overall the doom and gloom about occupancy is way overblown.

Now a recession (particularly a deep recession) may hit the industrial space hard and cause occupancy rates to drop. But with the current focus on “reshoring” and governments at all levels continuing with very large amounts of fiscal spending, I just don’t see it.

As for residential, it’s been by far the biggest beneficiary of the current government’s emphasis on immigration. There’s downside risk should we see a big shift in immigration policy (which seems to be building).

But at the same time, there’s such a scarcity of residential units that even if we (Canada) halted all immigration for a couple of years, there would still be a shortage.

It’s the Interest Rates

What isn’t overblown is what has happened to interest rates and how it’s affected REITs.

When interest rates were at generational lows, none of them termed out their debts. Now that interest rates have risen, it’s playing havoc on their financials.

To give you a sense of how dramatic the change is, here is SmartCentre REITs’ weighted average term to maturity and weighted average interest rate.

Over the last 2 years, SmartCentre’s weighted average interest rate has gone from 3% to 4% while their average term to maturity has gone from ~5 years to 3.5. This has increased their interest expense by 20%. And they’re one of the best-run REITs.

Many other REITs have seen their interest expense grow by much more (some by 50%). The rise isn’t just because of rising interest rates either. The REIT sector has continued to operate as if it’s “business as usual”. That has meant continued development of new properties (or acquiring new properties), and that’s meant taking on even more debt.

It wouldn’t be much of a problem except that most were already distributing 80% (or more) of their cash flows to investors. Now, many have payout ratios at 100% (or more) and it’s not sustainable. It also means that if they’re distributing out all of their cashflows, they’ll never be able to de-lever their balance sheets organically.

On top of that, the entire industry seems to have decided to wait/hope that interest rates will go down before refinancing their debt again. Many REITs’ average term to maturity is under 3.5 years now (versus 5+ years in the past) and some are approaching 2 while they sit and wait. This seems very dangerous to me as the old saying goes “A good treasurer raises capital when they can, not when they need it”.

I’m firmly in the camp that the world has fundamentally changed and it’s unlikely that the central banks take rates back to zero (ZIRP). And that means that REITs’ interest rates probably aren’t going to go down a lot.

Here is my back-of-the-napkin math.

Currently, the Bank of Canada's overnight rate is 5%. Assuming we have a recession and they cut the overnight rate by half to 2.5%. Then you add on 1.5% to 2% for credit spreads and most REITs’ interest expenses will remain unchanged or may even rise more. That’s because it’s important to remember that all of the debt REITs issued 3 to 5 years ago (and that’s now coming due) when interest rates were at zero.

But it gets worse. If a REIT is issuing a 5-year bond or mortgage, it would be priced off the 5-year reference bond yield and not the overnight rate. Over the last 10-years, the Canada 5-year treasury bond has averaged 30bps more than the overnight rate (and 45bps more if you exclude the last year because the curve has been deeply inverted).

So if get go back to the previous example add the 2.5% plus 0.3% for the curve and 1.5% to 2% for the credit spread. All of a sudden we’re looking at 4.3% to 4.8% which is higher than most REIT’s current weighted average interest rates.

Finally, there’s the question of whether there will be sufficient appetite from investors to refinance for all of the secured debt, mortgages, and credit facilities. As some REITs now have over $500mm in revolving credit facilities alone. So it leads to the question, if all of the REITs tried to refinance their debts at the same time, would some be left out in the cold?

So my advice is that if you are interested in investing in REITs, make sure you have a look at the balance sheet and are comfortable with both their interest rate risk and refunding risk.

Conclusion

Just wrapping up part 1, I want to emphasize that valuations have come down a lot and there is value to be had.

BUT, I think you have to be selective and willing to go through each REIT’s financials. Because the Bank of Canada cutting rates isn’t the panacea that most investors seem to think it is.

In my next article, I’ve divided up all of the REITs into six broad categories. They are “circling the drain”, “too much debt”, “meh - valuation isn’t compelling”, “just avoid”, “too early” and “recommended buys”.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.