Macro Thoughts: Spy The Lie

Macro Thoughts: Spy The Lie

Hi everyone,

Well, the markets makes fools of us all. Just two weeks ago I published a pretty bearish article on US markets. Since then, they’ve gone straight up!

But this week I’m going talk about something near (but not dear) to my heart. It’s Elon Musk and Tesla (full disclosure I am short Tesla so take everything that I say with a pinch of table salt).

Last week (January 25th to be precise), Tesla reported results after the market closed. The results were pretty bad, but that was expected and the stock was up a little. Until 5:30 pm when the share price started to soar.

So what happened at 5:30 for the share price to go vertical? Well, the company conference call started and a couple of things Elon said caught the market’s attention:

Elon Musk: Demand far exceeds production, and we actually are making some small price increases as a result.

Anyone that has (cynically) followed Elon & Tesla would notice that this is a classic Elon statement. Take a small kernel of truth and spin it into an outrageous lie.

So let’s dissect this statement.

First, earlier in the month Tesla had cut prices across all of its models by ~15%-20% globally (the range of the cuts seems to depend on the source).

The reason for the drastic price cuts is that inventory was piling up.

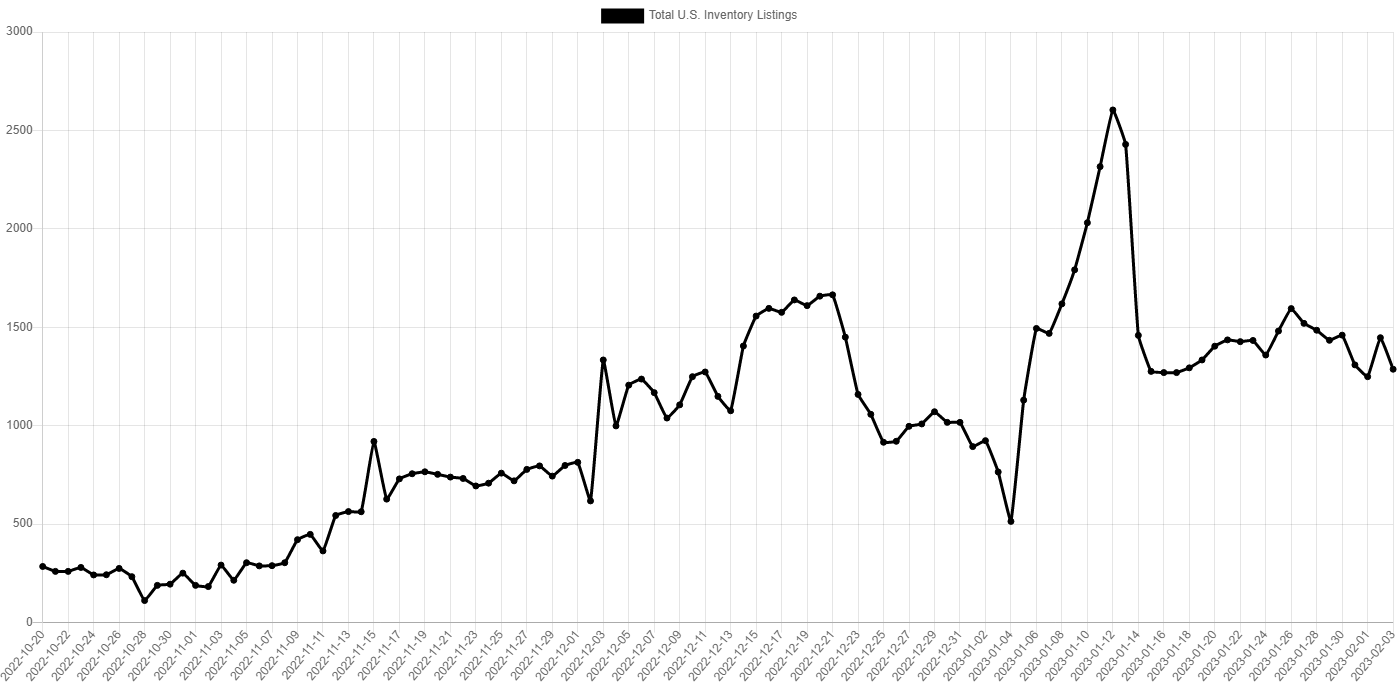

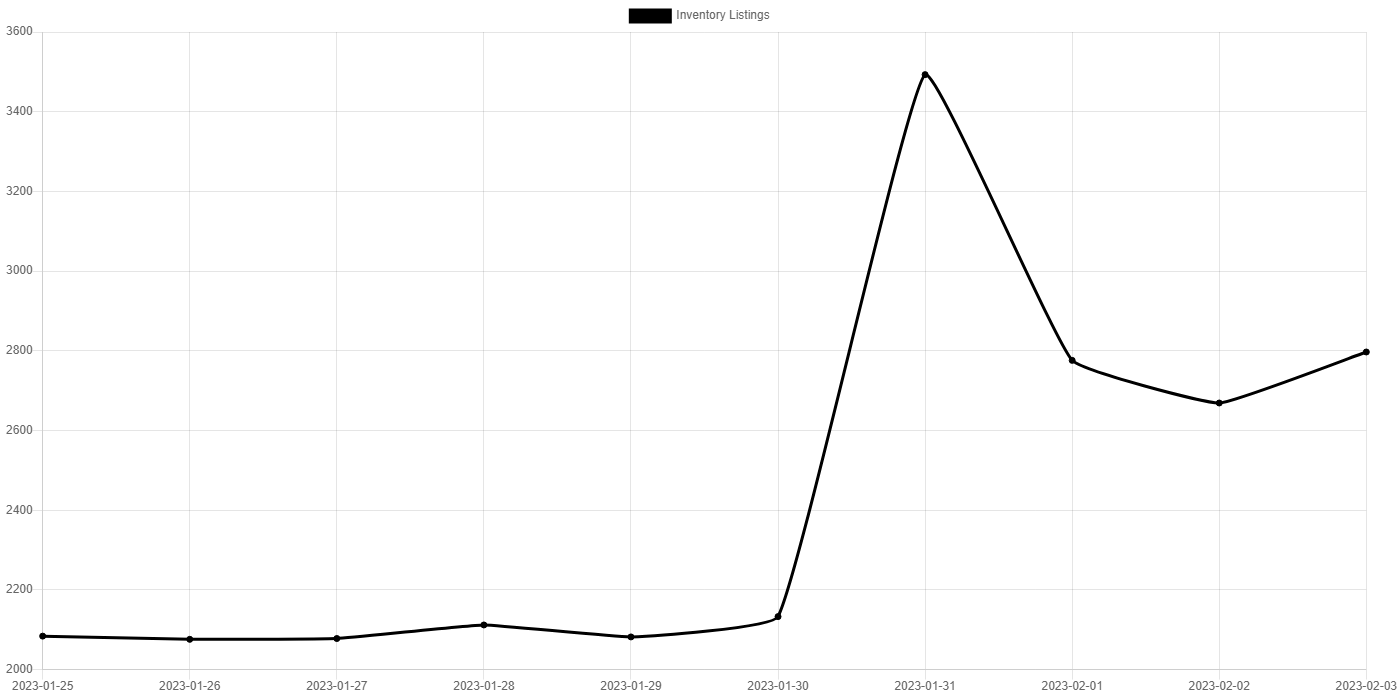

People have built web scrapers to track Tesla inventory and by the end of Q4 it was looking bad:

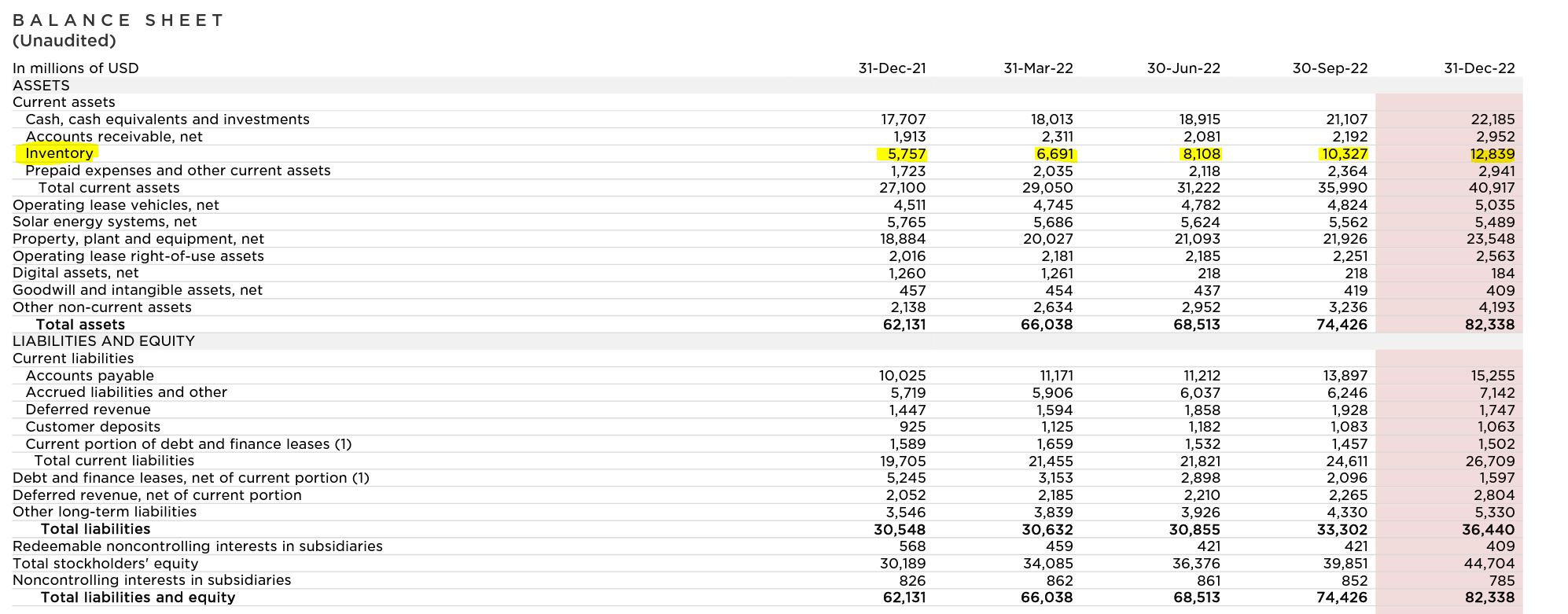

These data trackers were proven correct when Tesla released their unaudited earnings:

Tesla’s inventory was up 123% YoY and 24% QoQ. So Tesla had no choice but to cut prices to move inventory as it was taking up more and more working capital. The price cuts worked as they led to a surge in demand and inventory has somewhat normalized.

But wait, there’s more.

Tesla also halted all production from its Shanghai factory over the holidays (from December 25th to January 2nd).

The Shanghai factory represents at least 40% of Tesla’s global manufacturing output (it could be more depending on how much Austin & Berlin are actually producing).

And it doesn’t stop there either. After the earnings call, Tesla cut the lease rate on the base-level Model 3 so that it could get the monthly payments down to $399/month. Tesla is also offering $3,000 worth of free supercharging with the purchase of a Model S or X.

So how can Elon say that “demand exceeds production”?

Because it’s classic Elon, where he’s intentionally vague. He doesn’t define the timeframe nor elaborate on the statement. So he can always claim the statement was accurate (even though the substance was not).

Demand was (temporarily) supercharged thanks to the many price cuts and incentives. While production was less than normal as his largest plant was offline.

So in these circumstances, demand should outpace supply!

But as we can see from the inventory charts, demand has leveled off and inventory is no longer falling so the short-term bounce Tesla benefited from was short-lived.

But the statement worked and the rest is history…

10K Time

For those that aren’t familiar, 10K’s are the annual audited financials that companies file with the SEC. Historically, Tesla has taken 2 to 3 weeks after “reporting” their earnings to file their audited financials. This time Tesla filed their audited financials in record time.

It could be that Tesla has gotten better and hence the quicker filing. The cynic in me though thinks that it’s largely due to Elon needing to sell more Tesla shares (and soon) to plug the leaky boat that is Twitter.

Regardless, it’s what was in the audited financials that really mattered. Most of it was what you would expect and lined up with the earnings release. Except for one glaring issue:

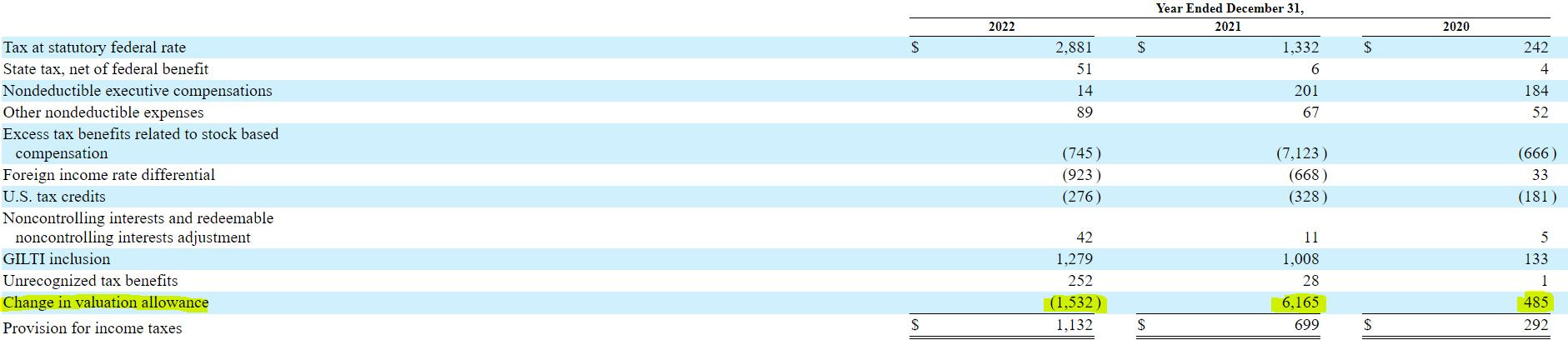

In Q4, Tesla reduced its deferred tax asset by $1.532 billion dollars and recorded a non-cash gain of the equivalent amount.

Now there’s nothing wrong with this on its own. The company had built up a massive deferred tax asset as it was unprofitable for a very long time. The company is now profitable so it is drawing down on its tax loss pools.

The issue is that this very large (and material) non-cash gain was never disclosed in the company’s earnings release or shareholder presentation.

In the earnings release, the company did disclose that the rise in the US dollar last year cost the company “over $300M” in foregone profits. But they never said anything about this non-cash gain.

This DTA gain represented ~40% of Tesla’s Q4 profit and the company would have missed (already significantly lowered) Wall Street estimates by a massive amount.

An honest company would have disclosed this non-cash gain given how material it is. But of course, Tesla (or Elon) is not an honest company (or person).

But just like his statements during the conference call, it succeeded as all of the sell-side and media attention was focused on the earnings release. There’s been virtually no follow-up since the actual audited financials were filed with the SEC.

These kinds of financial games are not new either. GE and IBM (and many others) have used these kinds of accounting gimmicks for years to hide underlying problems. But we know how it ended for both companies. I don’t think it will be any different for Tesla either. I’m probably too early (as I always am). But eventually, the sun will set on Tesla and Elon.

Disclosure: I am short and have a beneficial interest in the above-mentioned security. I may change my position at any time post-publication.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.