Macro Thoughts - The Coming Boom for American Workers?

Hi everyone,

As promised in the Sleepy Portfolio Update, here is an article that I’ve been kicking around for some time. Recession is on everyone’s mind right now given:

Monetary tightening by the Fed and other Central Banks along with rising interest rates.

Declining fiscal stimulus as the Covid response slowly rolls off.

High inflation dampening business and consumer sentiment.

Rising commodity and energy costs.

The fallout from the war in Ukraine and China’s zero covid policy (more on that later).

Many are now predicting that the upcoming recession will be as bad or worse than the Global Financial Crisis or the recessions during the early 1980s. And yet, I’m going to take a very contrarian view that the US may enter a recession, but it’s going to be fairly mild (especially compared to 2008 & 1980) and largely a white-collar recession (similar to the dotcom bust).

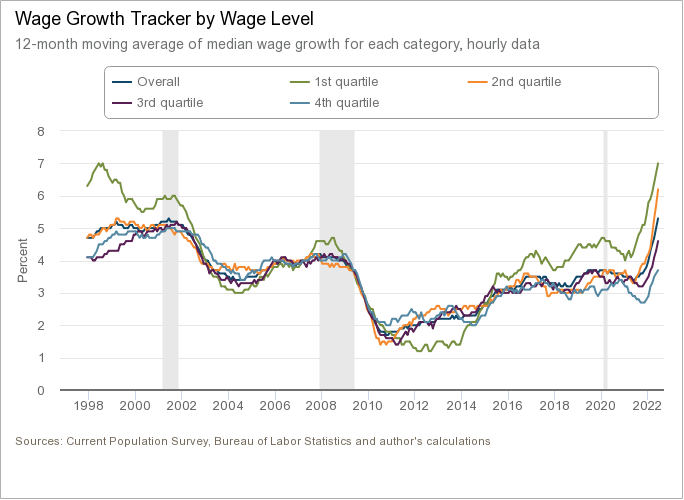

The reason why I believe that the upcoming recession won’t be that severe is that I think the US/North American labor market is going to hold up a lot better than most expect. Currently, wages have risen strongly but overall still declining in real terms due to inflation.

However, when you break it down by income group, you’ll see a big divergence between the richest 25% (4th quartile) and the rest. Those with the lowest income (i.e. the bottom 25% or 1st quartile) are currently seeing the strongest wage gains.

In this piece, I’m going to argue why I think this trend, that the average American worker will see outsized (real) income gains, will continue to play out over the next 3 to 5 (even as inflation moderates). It won’t be smooth sailing, as yesterday’s (Thursday - July 20th) initial unemployment claims showed. But I do think we’ll see many workers that were “left behind” over the last decade (or three) have a chance to play catch up.

United States’ biggest (economic) competitors have crippled themselves

“Never interfere with an enemy while he’s in the process of destroying himself” - Napoleon

While the world has slowly transitioned towards a more service-oriented economy, we still require a lot of “physical” stuff and the United States is still a powerhouse when it comes to manufacturing (albeit a reduced one).

Right now, we have lots of talk of “reshoring” where manufacturing jobs are returning to the United States (well really all of North America) after the last 3 decades of “hollowing out”. This is being driven by the (unintentional) helping hand from other countries whose policies and decisions over the last decade are coming home to roost.

Germany as we all know is one of the world’s largest manufacturers and they’ve also adopted an energy policy entirely dependent on cheap Russian gas and oil. The war in Ukraine has caused their entire economic and energy policy to blow up in their faces.

And yet in the face of complete economic ruin, Germany and the rest of Europe shows little interest in changing course. Germany still refuses to even consider extending the operating life of its existing nuclear power plants or re-open nuclear plants that were decommissioned.

It’s not just the Germans either. The Dutch have shown little interest in changing their policy of steadily shutting down the Groningen gas field (which once provided almost 25% of all of Europe’s natural gas needs). Meanwhile, shale oil fracking is a complete non-starter across all of Europe (even though there are large basins that could be tapped).

It will only get worse as this winter approaches barring some kind of last-minute peace treaty between Russia and Ukraine (which looks unlikely). Europe is already bleeding energy-intensive heavy industry which is unlikely to ever return:

Businesses are not waiting around and already shifting investment and production to North America which has the world’s cheapest and most secure/stable energy and electricity. For example, German petrochemical giant BASF is busy expanding a large chemical plant in Louisiana.

But it’s not just Germany that is struggling. China, which has been long regarded as “the world’s factory”, has had its own struggles (to put it mildly). Their “Zero Covid” policy has been a complete economic and social disaster. The reason for the draconian lockdowns is that the Chinese vaccine (Sinovac) isn’t effective (<10% effectiveness vs. 90%-95% for Western mRNA vaccines). Add in the country’s high rate of smoking, a weak healthcare system, and awful pollution levels that combined makes Covid acutely dangerous to residents in China.

It has already been floated (and then quickly walked back) that China could be stuck in “Zero Covid” for the next five years when they are able to develop their own mRNA vaccine. This would be devasting for Chinese long-term competitiveness, and China was already losing manufacturing jobs to South East Asia (such as Vietnam) and Mexico before this. This shift is still in its infancy so hard data is scarce but there are many anecdotes already. For instance, Chinese battery-making giant CATL is looking to expand into Mexico and or the US (rather than expand in say Western China).

Finally, South Korea and Japan round out the world’s manufacturing heavy weights. They followed similar energy policies as Europe and are suffering just as badly. With Japan having just purchased the most expensive LNG cargo in history.

The one upside for South Korea and Japan is that they’ve had their “come to Jesus moment” and have now started to change course regarding their energy policies. Japan is looking to restart a number of nuclear reactors as early as this winter, while South Korea looks to extend the life of their existing nuclear reactors and build out more nuclear power. The only downside is that it will take time. Meanwhile, Korea’s LG conglomerate is investing USD4.1 billion in a new battery plant here in Canada.

The net result is that net new manufacturing jobs, in both reshoring old jobs and new FDI (foreign direct investment) into the US/North America is booming. In 2021, the US saw ~260k manufacturing job gains via reshoring and FDI and is forecasted to add another ~400k in 2022.

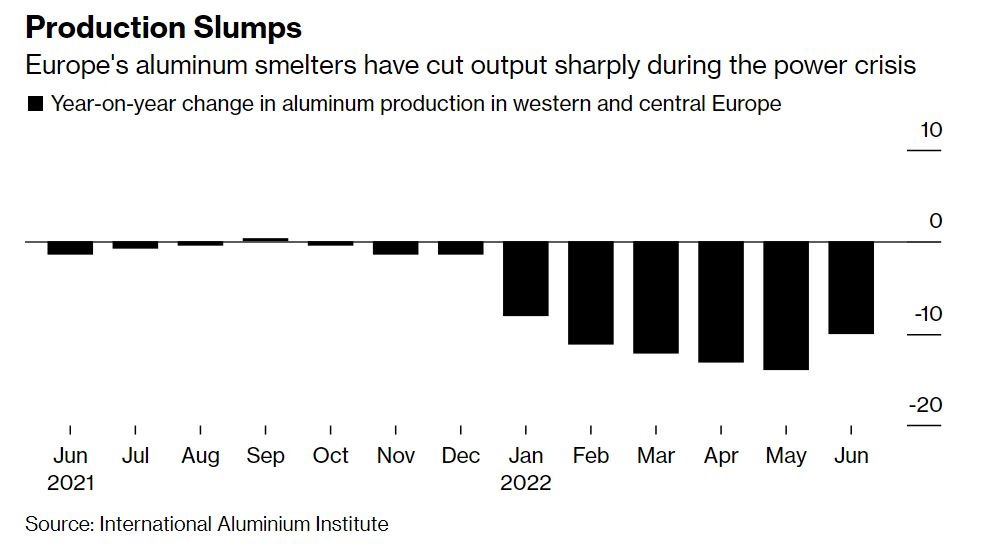

Here is a nice summary from a Bloomberg article detailing how CEOs are moving production out of China:

The construction of new manufacturing facilities in the US has soared 116% over the past year, dwarfing the 10% gain on all building projects combined, according to Dodge Construction Network. There are massive chip factories going up in Phoenix: Intel is building two just outside the city; Taiwan Semiconductor Manufacturing is constructing one in it. And aluminum and steel plants that are being erected all across the south: in Bay Minette, Alabama (Novelis); in Osceola, Arkansas (US Steel); and in Brandenburg, Kentucky (Nucor). Up near Buffalo, all this new semiconductor and steel output is fueling orders for air compressors that will be cranked out at an Ingersoll Rand plant that had been shuttered for years.

And here’s a great chart from the above-mentioned Bloomberg article:

Finally, keep in mind that while the manufacturing jobs added are relatively small. They are generally much higher paying than many services jobs and have a huge multiplier effect on the local economy and jobs (including services). If a new plant is opened that employs thousands of workers, you also see a large number of suppliers and services open up in the surrounding area to service both the factory/plant and its employees.

The Reinforcements Aren’t Coming

With the markets down, crypto down, home prices cooling and the cost of living rising; I’ve heard a lot of pundits proclaim some variation of “many who left/retired will have to re-enter the workforce”. In theory, this will help alleviate the worker shortage. The only problem is that this isn’t going to happen (at least not on a scale to move the needle)!

The current US unemployment rate is now at 3.6% and the most recent JOLTS (Job Openings and Labor Turnover Survey) shows about 2 job openings for every unemployed worker (11.3mm vs 5.95mm).

The Labor Force Participation Rate survey gets trotted out all the time to show that many workers have left the economy and will have to (eventually) return. This implicitly means that there’s a large reserve of workers just waiting on the sidelines to jump back into the labor market.

The only problem with all of this is that it’s wrong! The classic labor force participation rate survey is now deeply flawed because it was devised during an era far different than today. This survey counts anyone over the age of 16 as part of the labor force as it was created before things like post-secondary education (college/university) and retirement were commonplace.

If we look at the much more relevant “core” 25 - 54 Labor Force Participation Rate, we can see that the participation rate hasn’t really changed that much since the early 1990s. The last reading was at 82.3% versus 83.1% just prior to Covid a high of 84.6% in the late 1990s.

So that leads to the question, who is retiring/leaving the workforce? And the answer should be pretty obvious. It’s baby boomers! And no, most of them aren’t going to be coming back to the labor force regardless of how tight the labor market becomes and how fast wages grow.

Bloomberg just published an article on how people that are 75+ are coming back into the labor market. But this flies in the face of conventional wisdom and common sense. The median baby boomer is now ~68 years old, they are the wealthiest generation in history (with the vast majority owning their own home outright and much more), and they’ve already delayed their retirements for many years due to the fallout of the GFC.

There will be certainly some baby boomers who unfortunately will have to work until they die. But by and large, the vast majority of baby boomers that haven’t already retired are going to be heading for the exits within the next couple of years. And there aren’t nearly enough young people coming up behind them to replace all of them.

Immigration could help alleviate this problem. But there’s little political will to dramatically increase immigration at this time as polling shows that a majority of Americans do not want more immigration. Down the road, and as the labor crunch worsens, this could change but right now it seems unlikely.

Where Could It Go Wrong?

Obviously, no forecast is ever perfect and there are definitely a lot of possible outcomes that could make me look very wrong. I think the following could be real problems and worth watching out for:

Fed hikes far too much. The Fed is clearly behind the curve and now trying to play catch up. In one scenario, the Fed over-tightens by pushing the overnight rate to say 4%+ which plunges the US into a deep recession. This wouldn’t be the first time this happened either. The 1937-1938 recession was caused by the Fed over-tightening as the US economy started to recover from the Great Depression and policymakers panicked over rising credit growth. The result was that the US economy collapsed (again) and Great Depression continued until WW2.

Something like this could happen, although the interest rate futures markets are already starting to price in rate cuts by the Fed next year. And I think it would take a pretty big tightening cycle to impact actual consumer spending (and not just consumer sentiment). US consumers’ balance sheets are pretty healthy and most homeowners locked in 30-year mortgages over the last couple of years at very low rates and therefore aren’t impacted by rate hikes. Higher rates are clearly slowing down the housing market which has a big multiplier effect on the economy though.

Trouble Overseas. If Europe and/or China enter a deep recession due to the policy choices they’ve made, does that drag down the United States and the rest of the world into a recession with them? Or does the United States and commodity-producing emerging markets (Brazil, Indonesia, Middle East, etc.) flush with cash drag Europe and China up? I honestly don’t know at this point.

I think it will depend largely on how much fiscal stimulus the EU & China rolls out to stabilize their economies. Already, Spain, Portgular, and Greece are balking at cutting the natural gas consumption to “bail out” Germany as lingering resentment over how the EU debt crisis a decade ago was handled. The EU could fall apart into infighting, or they could be angling for some kind of continent-wide fiscal deal.

As for China, who knows? They are opaque at the best of times. There is news of possibly a new big fiscal stimulus package being unleashed. But the CCP “election” that will see President Xi return for a third term at the 20th National Congress of the CCP isn’t until the fall and by then it might be too late. President Xi could fall on his sword (i.e. lose face) and adopt a Western vaccine to end the “Covid Zero” policy, but that seems unlikely.

The continued tensions over Taiwan aren’t helping with sentiment either. Should China go ahead with its long-rumored invasion, then all bets for the global economy are off.

Autonomation and AI. Both of these topics get a lot of mileage in the news, promising that any minute now they will “revolutionize the world and make workers redundant”. The unfortunate problem is that it’s less an overnight transformation but a slow and gradual adjustment.

Will the world and work be dramatically different 10, 15, or 20 years from now? Absolutely.

But will companies, especially in fields like manufacturing and heavy industry, be able to completely redesign entire processes and procedures to incorporate robots, automation, and AI (that might not even exist) overnight (or the next year)? Not a chance. And that’s assuming you could even find the workers to make it happen in the first place.

So now, over the timeline that I’m looking at (i.e. the next three to five years), I think it will have a fairly slow and steady, but ultimately minimal impact.

Energy. As everyone knows, I’m a huge energy bull. And if we get a pronounced spike in energy prices (earlier this year with Russia’s invasion of Ukraine being a test run), it could send the whole world into a 1970s-esque recession.

The IEA says we are now in the world’s first global energy crisis (this was the same IEA that recommended everyone stop investing in fossil fuels a year ago). However, in a somewhat contrarian way, a global energy crisis would likely benefit North America.

North America is now self-sufficient when it comes to its energy needs. This is why European nat gas (using TTF) trades at almost 10x premium to US nat gas (HH). As recently as the mid-2000s, the US imported over 10mm bb/d of oil. It is now largely self-sufficient while importing heavy oil from Canada and exporting light oil globally. This gives the continent a massive advantage over Europe, China, Japan and South Korea which are all resource-poor.

But it would largely depend on the magnitude of the energy price spike. Oil spiking to $180/bbl (which inflation-adjusted would be equivalent to its 2008 high) would slow the global economy and may tip it into a recession. Oil spiking to $250/bbl or $300/bbl would probably crash the global economy.

Conclusion and early investment implications

This article went on much longer than I was anticipating so I’m going to delve into the investment implications at a later date. A strong labor market is net-net a good thing for the economy. However, what’s good for the economy might not be good for the markets (and vice-versa).

We saw during the 2010s that a weak labor market led to strong corporate margins (as they held all of the bargaining power). Meanwhile, a weak economy led to very accommodative central banks which boosted financial asset valuations.

As the chart from Darius Dale at 42 Macro shows, employee compensation including government transfers (blue line) spiked in 2020 due to the fiscal stimulus but returned to the bottom end of this 60-year range.

The beneficiary of this weak labor market was corporate profitability (red line) which is still close to its highest over the period. With a continued tight labor market, the only release valve will be employee wages.

While everyone laughed at the lengths technology companies went to attract and retain staff during the 2010s, we could see a more broad replay of this across all industries as reality dawns on companies that their employees aren’t just disposable expenses (although maybe not as extreme).

This will mean that just as liquidity is being withdrawn from the markets by central banks, corporate profit margins will be under considerable pressure. This is bad for “rentiers” (i.e. asset owners) and corporate executives, but good for workers (and hopefully social/political stability).

I hope you found this informative and interesting and if you have any thoughts or pushback just let me know.