Macro Thoughts - The Great Mining Scramble

Macro Thoughts - The Great Mining Scramble

Hi everyone

This is an idea that I’ve been meaning to write about for a while. The theme has received some press coverage but what’s been going on in the mining industry has largely gone under the radar.

So what’s the theme? There’s been a huge wave of consolidation in the mining sector this year and I think it’s just the beginning.

Just in the last month or so, we’ve seen the following big M&A announcements:

American mining company Newmont is acquiring Australian gold miner Newcrest.

Anglo-Australia’s Rio Tinto and Canada’s First Quantum are forming a joint partnership for a large mine under development in Peru.

Canadian-based Hudbay Minerals is acquiring Canadian miner Copper Mountain Mining.

Swiss-based Glencore is trying to acquire Canada’s Teck Ressources (still ongoing).

UAE’s Fujairah Holdings offered to acquire all of Canada’s Asante Gold.

It’s almost as if someone fired the starting gun and we’re watching the beginnings of a mad scramble.

So what’s going on? And why has there been so much M&A recently?

I think it’s because there are a couple of big trends that are colliding at the same time:

The last decade has been a brutal period for cyclicals and especially so for mining companies. Commodity prices dropped a lot and many new mines ended up way over budget and delayed.

This caused the mining industry to incur hundreds of billions of dollars in losses.

Large-cap mining companies drastically cut costs across the board to survive. Many small-cap mining companies simply went broke.

Over time, profitability returned and balance sheets were slowly repaired as debt was paid down.

In spite of recession fears, commodity prices are still relatively high. Copper prices in particular remain close to all-time highs largely thanks to demand from the Green Transition (something that I wrote about last December (can be found here). Meanwhile gold is doing gold things (i.e. going up when everyone stopped caring about it).

And now we’re here we are.

The large & mega-cap mining companies are now flush with cash but suffering from declining production and reserves.

I’ll use Canada’s Barrick Gold as an (extreme) example of the 2010s.

For those who aren’t familiar with the company, it was founded by Peter Munk and became the world’s largest gold mining company in the late 2000s and early 2010s.

Peter Munk was an empire-builder with the singular goal of creating the world’s largest gold mining company (which he accomplished).

The downside of this strategy is that the company took a lot of risks and never paid much attention to operations or profitability (sounds familiar to many tech companies).

When commodity prices dropped (gold declined from ~USD1760/oz to under USD1100/oz), the company crashed and burned. In 2012 Barrick added ex-Goldman Sachs banker John Thornton to the board of directors. Then in 2014, there was a palace coup that saw John Thornton replace Peter Munk as executive chairman.

After that, Thornton started to slash costs and cut back on exploration and development to right the ship. Along the way, Barrick acquired South African gold miner Rangold Resources. Its President & Founder, Mark Bristow, took over as President and CEO of the combined firms.

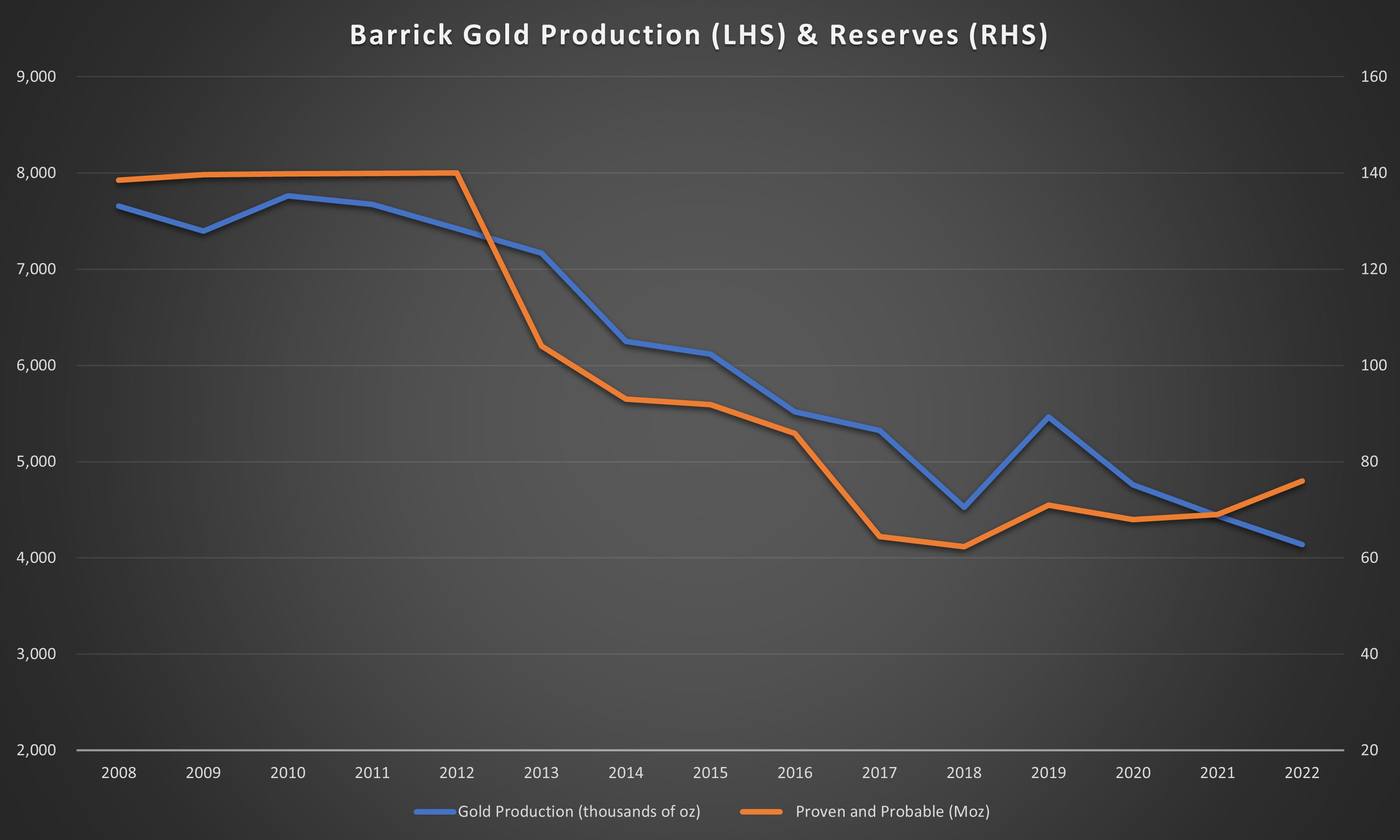

I want to tell the story of Barrick through three charts. First, there’s the company’s gold production and reserves:

Its net income and free cash flow:

And finally the company’s net debt:

From 2008 until 2014 the company cumulatively lost $9.4 billion (they lost another $3.1 billion in 2015 during restructuring) and generated negative free cash flow of $5.8 billion.

To plug the hole, the company’s debt swelled from $3-4 billion to a peak of almost $12 billion. This was unsustainable. Either the company had to get its costs under control or it would very soon be headed to bankruptcy.

And that’s exactly what John Thornton did. He cut costs ruthlessly. Eventually, profitability and positive free cash returned. And the giant pile of debt was slowly paid down.

But it came at a tremendous cost in terms of production and reserves.

It’s worth pointing out that Barrick is an extreme example, but it’s a problem across the industry.

Adding to the dilemma is that it now takes 13 to 17 years to develop a new mine. So anything that is started today likely won’t come online until the end of the next decade (2035 - 2040).

So what’s a mega-cap mining company to do? Well, we’ve already seen it start. And that’s to go out and buy their (smaller) peers. Even better (for them), the small and mid-cap mining companies’ valuations are even lower, so acquiring them becomes very accretive and very quickly.

And what are investors to do? I think it’s time to roll up our sleeves and start going through all the mining companies that are left (something few investors have done in over a decade).

Fortunately, the entire listed mining industry is now tiny. Using Koyfin, I pulled up a list of every mining company with a market cap in excess of USD $250mm (excluding China & Russia).

The result is that there are only 340 companies that meet this criteria. They have a combined market cap of approximately USD ~$1.35 trillion. For comparison's sake, Apple has a market cap of roughly USD $2.65 trillion.

Over the summer, my goal is to go through all these companies and at least get a high-level understanding of each and from there drill down and put together a basket of 5 to 15 names to own long-term.

My current personal picks were Copper Mountain (CMMC.TO) and Centerra Gold (CG.TO). Unfortunately, because I procrastinated in writing this article Copper Mountain was already acquired.

As for Centerra Gold, I’m planning on writing a short article summarizing the company next week so stay tuned.

Disclosure: I am long and have a beneficial interest in all of the above-mentioned securities. I may change my holdings at any time post-publication.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.