Oil - The Good, The Bad and the Ugly

Oil - The Good, The Bad and the Ugly

Hi everyone,

I’ll be publishing the monthly Sleepy Portfolio next week. But as a heads-up, the performance wasn’t good (especially relative). The trend since November continued with massively outperforming technology (which the Sleepy Portfolio has zero weight to).

At the same time, energy has continued to lag. Oil remains volatile, but within a very tight channel of ~70/bbl to ~78/bbl (using front-month WTI). Adding to energy in both portfolios in December hasn’t paid off.

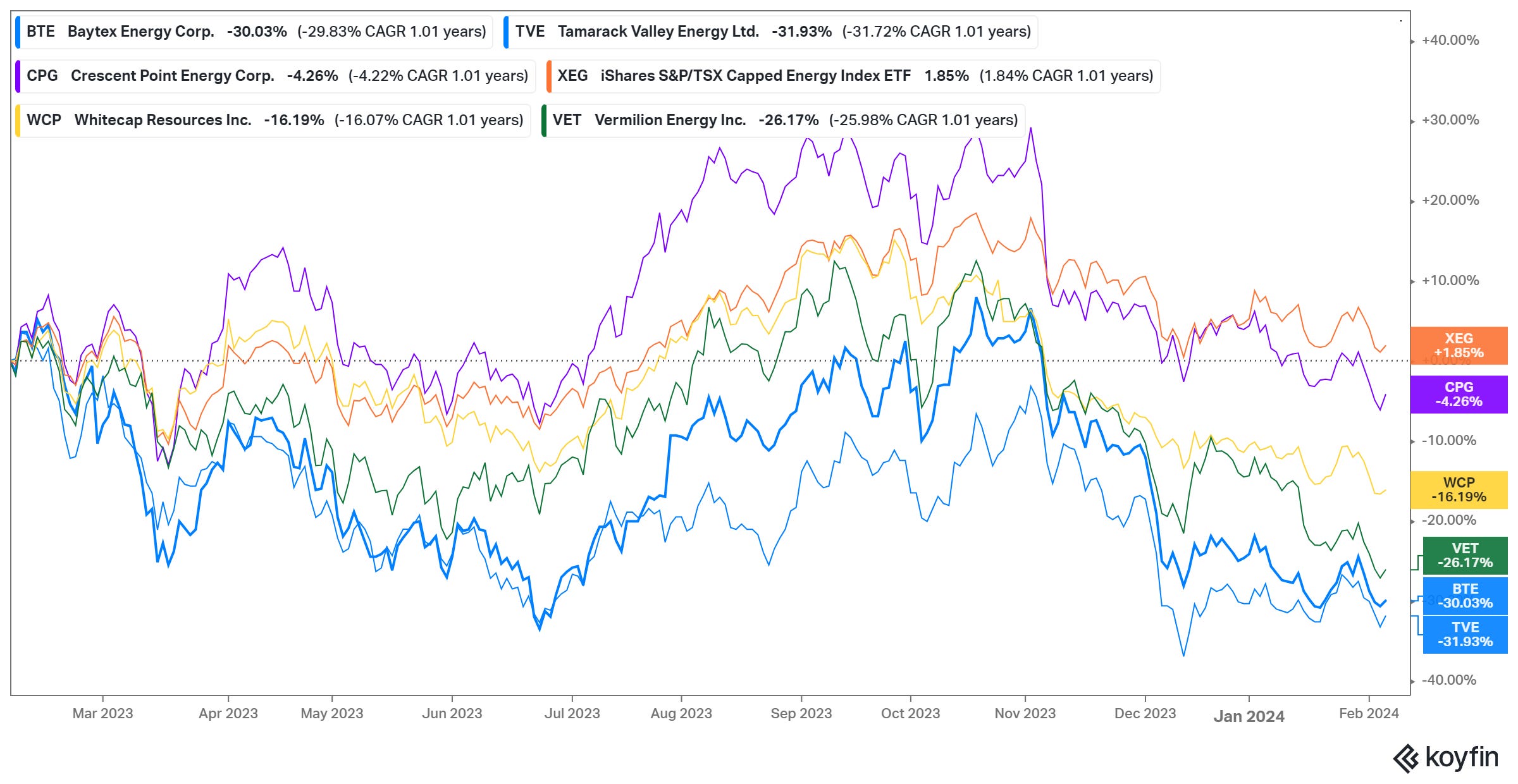

While oil is slightly up on the year, most energy stocks are down and continue to grind lower and lower, with Canadian junior and mid-cap energy particularly hard hit.

I thought oil would be range-bound between $75/bbl and $90/bbl using front-month WTI (see my Surprise Predictions for 2024). But I thought (or perhaps hoped) that it would hang around $80/bbl instead of the low 70s where it currently is.

Being a long-time bull on energy, I thought taking a moment and taking stock of the situation would be worthwhile.

Bad - Technicals and Sentiment are Awful. There’s no way around it. The technicals and sentiment are truly awful in energy right now. Every rally has faded and every headline from possible peace in the Middle East, strong economic reports, weak economic reports, etc. seems to cause oil prices to drop.

Volatility has also been pretty high (at least on the downside). Just last week, Al Jazeera reported that there was a peace deal in place between Israel and Hamas. Even though the story was denied and retracted, oil prices still plunged $6/bbl in 2 days. Stating the obvious but this kind of volatility hurts the industry as most investors would rather stay away.

On top of that, many still predict that the US/Globe will head into a recession; largely due to the yield curve. The go-to recession trade has been too short energy given its economic sensitivity. Of course, they’ve been wrong for a long time (yield curves inverted almost 600 days ago), but the bears are still convinced a recession will happen sometime this year.

Lastly, the rest of the market keeps powering higher. Queue J.P. Morgan’s famous phrase:

“Nothing so undermines your financial judgement as the sight of your neighbor getting rich.”

There’s a lot of bitterness within the energy investment community as they watch NVDA and other technology stocks going up seemingly every day (and if you don’t believe me then just go look on Twitter).

Good - Fundamentals are good. Historically between January and May, oil inventories build ahead of the summer driving season. But this year we haven’t seen the builds (yet). So far this year, US crude inventories (including SPR) have gone down by 10.6mm barrels. Compare that to last year (a much more normal year) where crude inventories increased by 30.2mm barrels.

The same thing is happening globally as oil inventories continue to decline.

Good - Russian energy infrastructure under attack. Since the turn of the calendar, Ukraine’s strategy has dramatically changed. 2 years into the war and they’ve now started to attack Russia’s energy infrastructure (what prompted this is unknown but I could take an educated guess or two). Using swarms of drones, Ukraine has been attacking Russia’s refineries and energy export terminals relentlessly.

These are huge facilities containing lots of volatile compounds which makes them juicy targets. Russia manages to intercept 97 or 98 drones out of 100, it only takes one or two to cause considerable damage.

This chart (which is already out of date due to another two attacks in the last couple of days) shows the extent of the attacks. The effects are already showing as Reuters reported that Russian exports of gasoline and diesel were down 37% and 23% respectively in January.

Bad - China. It’s no secret that China is struggling. The world’s 2nd largest oil consumer and long-time marginal demand growth is in a funk. The reasons are pretty straightforward.

Xi’s “Zero Covid” policy was a complete disaster that crushed consumer confidence (which still hasn’t recovered). Meanwhile, they have dragged their feet on some kind of “TARP” style bailout package to clean up all the toxic real estate debt. Finally, they continue to cling to the hope that export-driven growth will get them out of this crisis while dismissing a greater focus on services and consumer spending. It’s looking increasingly likely that China is going down the same path as Japan circa the late 80s and Europe post-2010 (European debt crisis), which is bleak.

Good - India & USA. China's (and Europe's) loss has been India's and the USA’s gain. Both economies are doing great. Demand for oil in the US probably isn’t going to grow anymore, but a strong economy never hurt either.

As for India, its economy is booming and they’re just getting on the energy “S-curve”. India is the world’s 3rd largest consumer of oil. But on a per capita basis it only consumes about 50 gallons of oil per year. Compared to 140 gallons in China and 920 in the US. So it has a long way to go just to catch up to China.

Bad - Biden Administration. Gasoline prices in the United States play an outsized role in everything from consumer confidence to public approval of the President. It makes no logical sense given that it’s only ~3% of the median person’s budget, but it is what it is.

And nobody knows that better than life-long politician and President Joe Biden. Every step his administration has taken over the last couple of years has been to get oil prices low and keep them there.

For instance, the Biden administration has all but stopped enforcing oil sanctions on Iran, even though both countries are in a defacto war (without admitting it).

When Biden was elected, Iranian production was around 2mm bbl/day. It’s now over 3mm and some projections peg Iran’s production to be more than 3.5mm by the end of this year.

The election is still ~9 months away (or 273 days to be precise) so you have to expect the US administration to pull out all stops to make sure oil stays as low as possible at least until then.

Ugly - Over Promise and Under Deliver. This one is for Canadian juniors and mid-cap energy in particular. After the Covid, they spent years (loudly) saying that once they reached their net debt targets they would start returning “all” of their free cash flow to shareholders.

Last year most hit those net debt targets. Did they follow through on their pledge? Nope. They all went on a massive M&A buying spree and told investors to just sit and wait. Fast forward a year, and oil prices are lower and investor’s patience has run out. The only Sleepy Portfolio that’s impacted here is Whitecap whose XTO Canada purchase just hasn’t worked due to the low natural gas prices.

Big players in the M&A such as Baytex Energy (BTE), Tamarack Valley (TVE), and Vermilion Energy (VET) all performed much worse though.

Management teams can woo investors back. But that will require rebuilding trust and credibility which will take time.

Overall the valuations in the sector look really compelling, with most energy companies trading at a free cash flow (FCF) yield more than 10%. Compared to Mag7 and technology stocks that have an FCF yield of less than 2% (after backing out SBC) they look downright cheap. But as Ben Graham famously said:

“In the short run, the market is a voting machine but in the long run, it is a weighing machine.”

So I have no idea when (if ever) the valuation gap narrows. And it may never. Which is all the more reason that energy companies need to focus on dividends and share buybacks.

Summing it all up. Just wrapping it up, fundamentals are very good (especially for this time of the year). However, the sentiment is awful and that’s likely driving the technicals.

Will it change overnight? No. But if we see continued declines in both oil and product inventories, oil prices will be forced to slowly grind higher. Fears of recession won’t probably go away as bears continue to just change the dates for the “imminent” recession. But it should sentiment and technicals should slowly improve over time.

But make no mistake, the Biden administration will be hell-bent on doing everything in its power to make sure oil prices don’t rise too much.

So I still think energy will probably get back to the high 70s to low 80s, but probably won’t go any higher barring something major. Even at those prices, most oil and gas companies should be very profitable, but whether they’ll allocate the capital wisely remains to be seen.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.