Sleepy Portfolio - January Update

Sleepy Portfolio - January Update

Hi everyone,

Welcome to 2024! There are no changes to the Canadian or Global portfolios for January as companies are just starting to report Q4 results. I probably won’t be making any changes until March when almost all of the companies have reported.

But there’s lots to discuss, both looking back at 2023 and forward to 2024.

2023 was one for the record books. The NASDAQ put in its best year since 1999 (up 55%). The S&P 500 was up 26%, MSCI EAFE (international stocks) was up 18% (in USD) while the TSX lagged being up “only” 12%.

The Canadian portfolio was doing okay until the last two months of the year. It put in an overall good year but on a relative basis gave back a lot of performance in November and December (energy stocks were a big drag). On the plus side, adding momentum while also screening out illiquid stocks was a big positive.

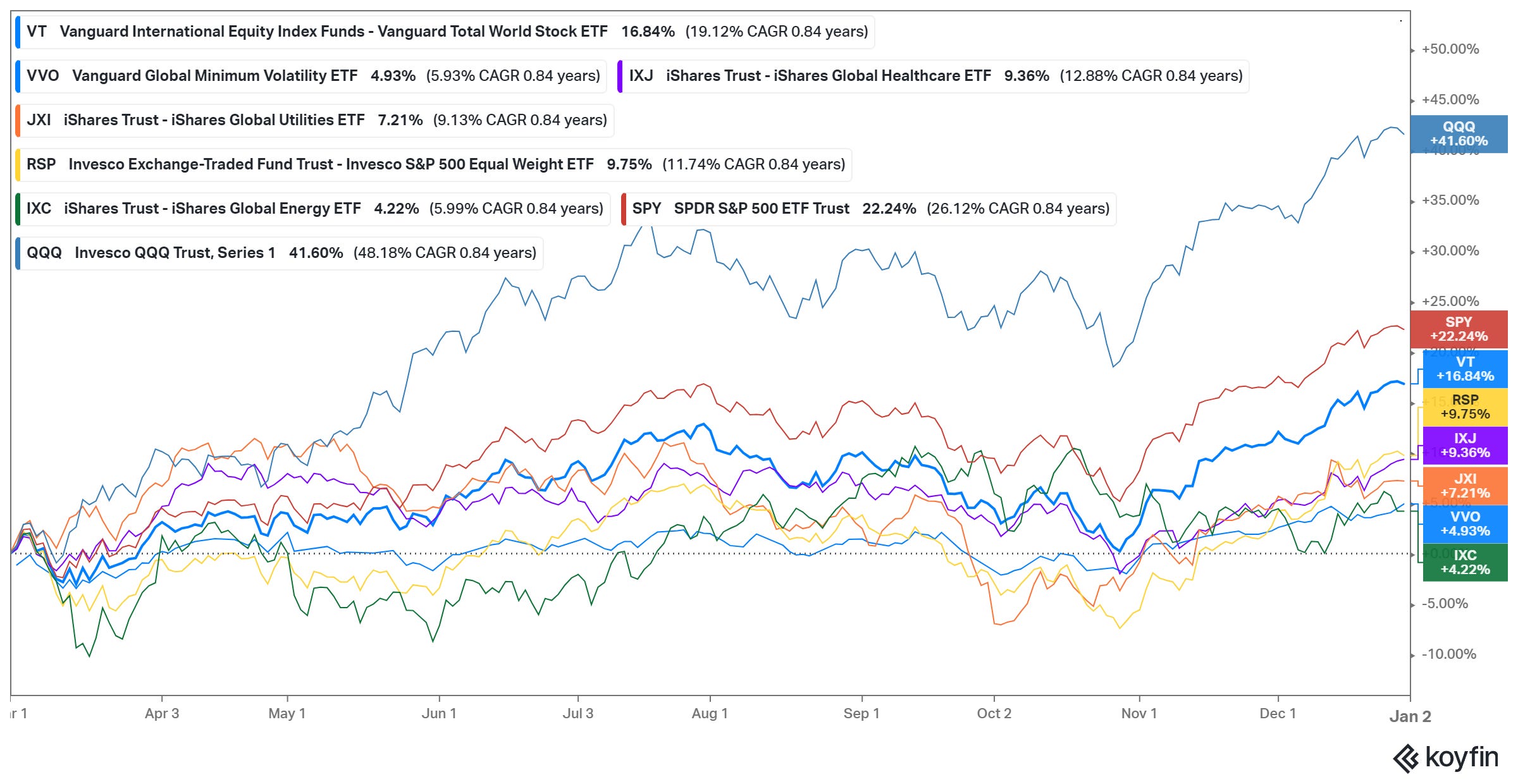

Moving over the Global side, the Sleepy Portfolio (up 6.85%) badly lagged VT (Vanguard Global Equity Index ETF - up 17%)) from its inception in March.

2023 was a year where the hare beat the tortoise by a mile (and some). It was dominated by the “Magnificient 7” (Microsoft, Apple, Amazon, Google, Facebook, Nvidia, and Tesla) and high beta junk (unprofitable growth, high short interest, etc.).

The Global portfolio has neither. As currently constructed, it will always be underweight technology companies due to its focus on dividends (most technology companies pay little to no dividends).

I could alter the strategy to shareholder yield (dividends plus share buybacks and net debt repayment). But that seems to be the very definition of chasing returns (again after the best year for tech stocks in over 2 decades).

There’s also the practical problem that I get my data from Koyfin and they only just recently added shareholder yield data. And I’m not sure how accurate it is (especially for international stocks). So I’ll be doing some investigating over the next couple of months and keep it in my back pocket for now.

At least I can console myself that I wasn’t the only tortoise that missed the rally. Most global low-vol and overall defensive strategies performed poorly (at least relative to market cap-weighted indexes). Energy and miners had another “blah” year too:

Oil prices tanked after surging to $90/bbl (using WTI) at the start of the Israel/Hamas war. Tax loss selling was particularly brutal for Canadian small and mid-caps. Meanwhile, anything with natural gas exposure has been crushed due to the mild winter (largely thanks to El Nino).

Here’s how some of the Canadian O&G stocks did over the last two months:

Canadian Natural Resources (CNQ), Pembina Pipelines (PPL), Tourmaline (TOU), and Whitecap Resources (WCP) are all part of the Canadian portfolio. Baytex (BTE), Crescent Point (CPG), and Tamarack Valley (TVE) were the “FinTwit” favorites of the year and just shows how brutal the last two months were.

In December I added to the energy in both portfolios. Headwater Exploration (HWX) in Canada and Petrobras (PBR) in the Global portfolio and it hasn’t paid off yet (HWX is down slightly while PBR is up slightly).

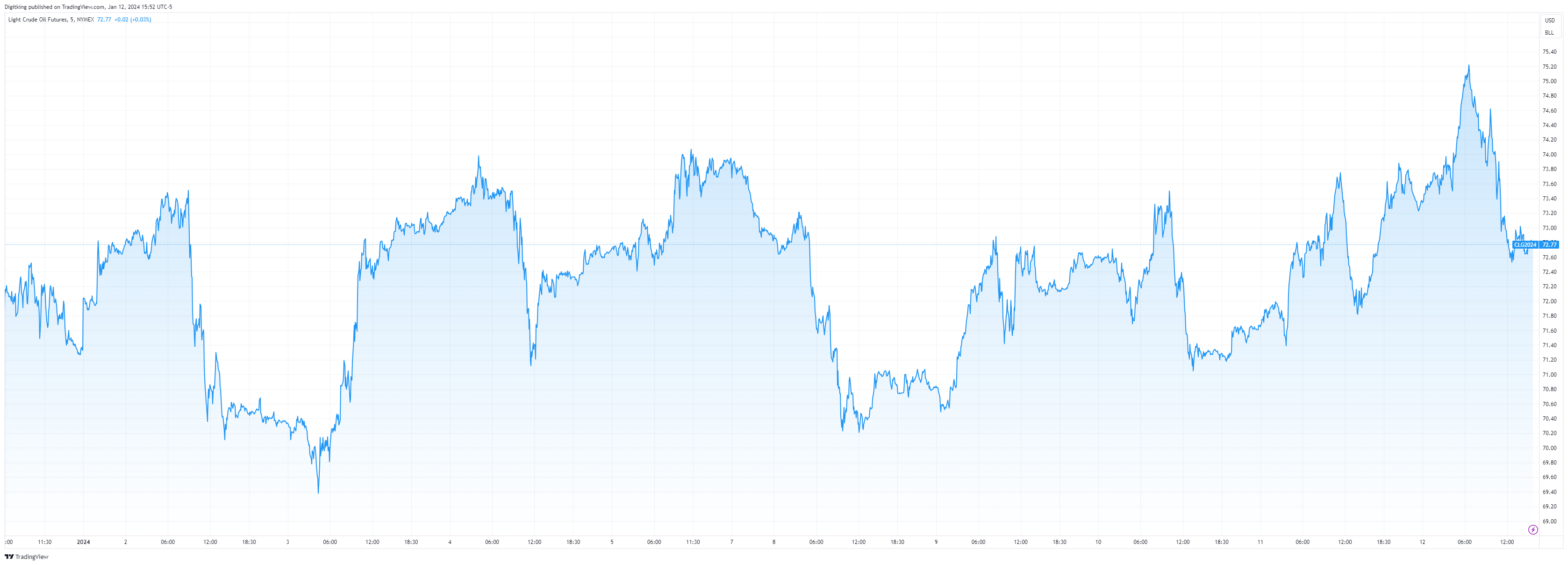

Speaking of oil, geopolitics continues to rear its ugly head. The headlines have been getting more and more alarming, but oil has so far remained in a very tight range of $70-$75/bbl (using WTI):

Last week, there was a big article in Politico that the Biden administration and the US intelligence/defense community worry that time is running out to prevent the war from spreading.

Since then, Israel has started evacuating civilians from northern Israel, arming its territorial defense groups, and prepping its hospitals for the possibility of thousands of casualties. A war between Israel and Lebanon’s Hezbollah seems increasingly inevitable.

On Thursday morning (January 11th), US Secretary of State Anthony Blinken in Bahrain stated that Iran was directing Yemen’s Houthi rebels attacks on international shipping in the Read Sea. You couldn’t get closer to a declaration of war without crossing the line.

And then that evening, a US-led coalition bombed over 60 targets in Houthi-controlled areas of Yemen. The bombings have continued through the weekend as it looks like the US is fed up with the Houthis.

Is it the beginning of the end? Or the end of the beginning?

I’m leaning towards the latter as Saudi Arabia has been bombing the Houthis for years with little to show for it. But this continues the escalation of tensions in the region and brings the US and Iran ever closer to direct conflict.

Yet the consensus right now is that oil will remain largely rangebound due to the amount of spare capacity from OPEC. In my surprise predictions, #9 was that oil (again using WTI) would remain range bound between $75 and $90. But as I said then and I’ll repeat now, if there’s a direct war with Iran all bets are off.

In the markets, we’re only two weeks into 2024 but we’re already seeing some massive rotations. Fundamentals are re-asserting themselves and some sanity is returning.

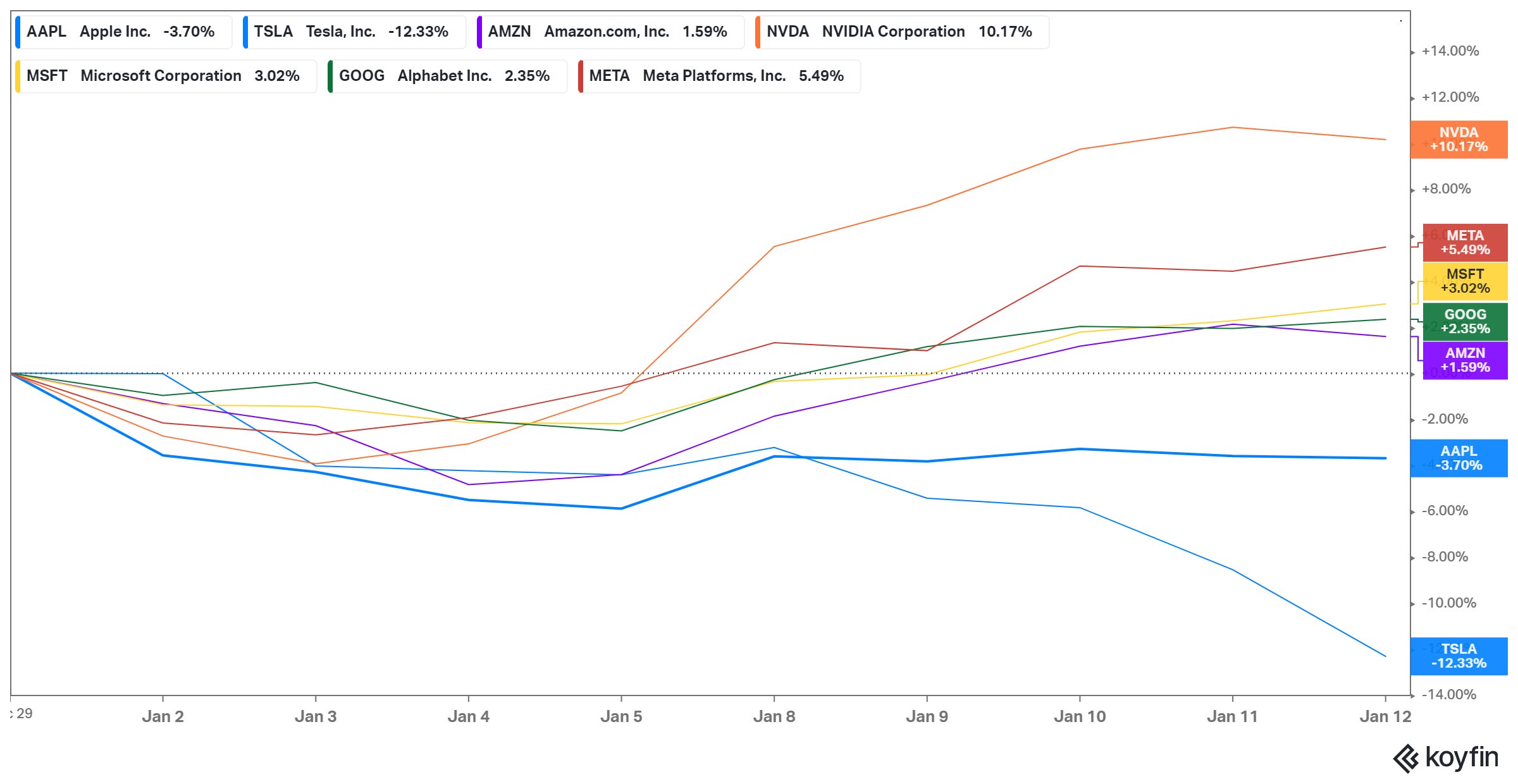

The Mag7 is turning into the Mag5 as both Tesla and Apple fall to the wayside:

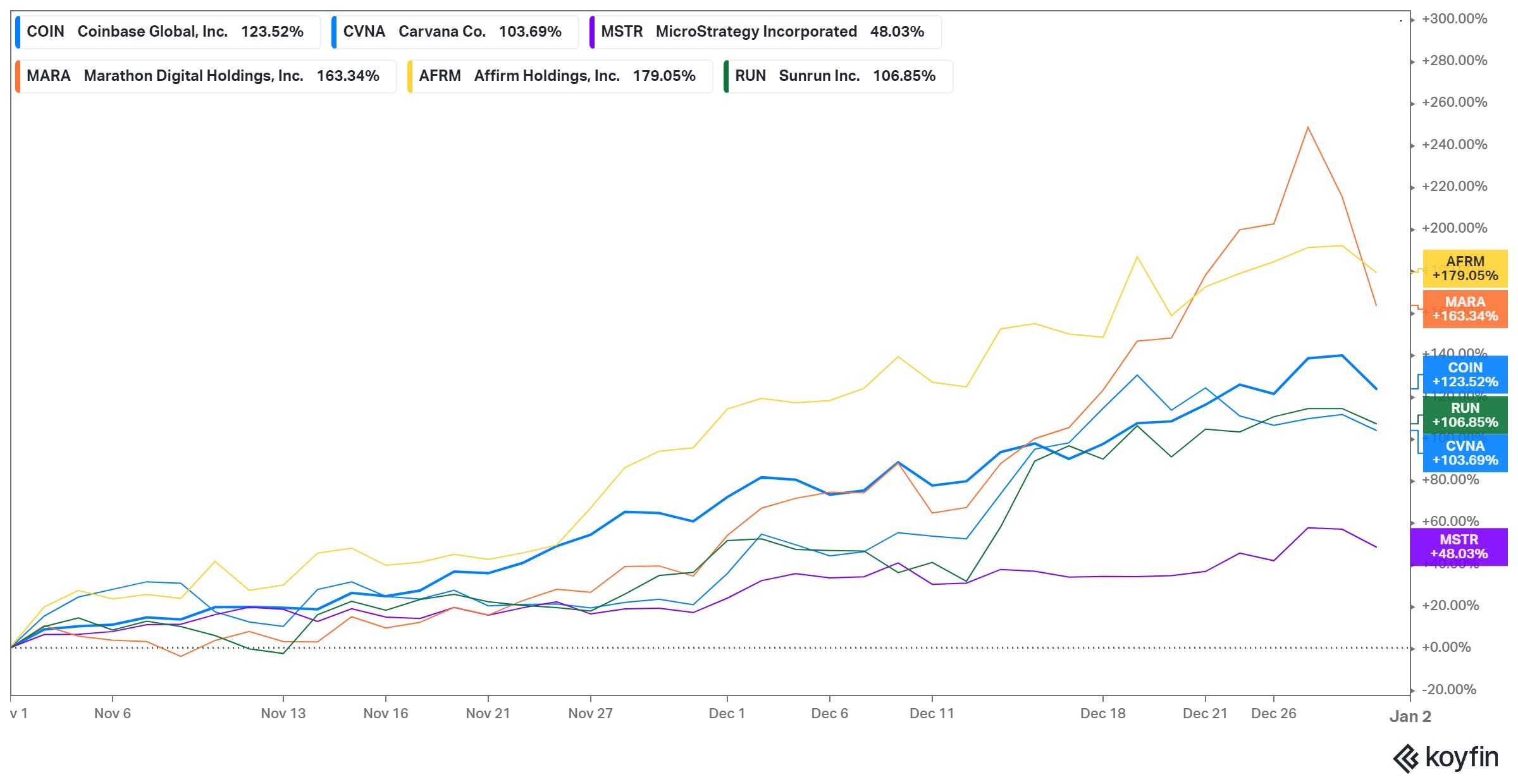

Unprofitable tech and crypto-related stocks soared in 2023 with many up over 100% just in the last two months of the year (here’s just a handful of examples):

They are now crashing back to Earth:

This is despite bond yields continuing to drop with the US 10-year bond now below 4%. Futures markets are now pricing in 7 rate cuts for this year. I still think the likelihood that the US will experience a recession in 2024 is unlikely.

It would be unprecedented given the amount of fiscal spending that is still ongoing. Here’s a chart from a fantastic Bloomberg article on the fiscal deficits:

And the United States, unlike much of the rest of the world, has become highly insulated from interest rates. ~40% of US homeowners don’t have a mortgage on their home. For those that do, the median mortgage interest rate is 3.5% (locked-in for 30 years) and over 95% of mortgages are below 5%. So without major layoffs, I don’t see consumer spending dropping at all.

US corporates also termed out much of their debt. US megacaps like Microsoft and Apple have weighted average debt of around 3% while collecting 5% on their cash. The only borrowers that are now feeling the pain of higher interest rates are the US Federal Government, real estate, and private equity.

On the other hand, inflation continues to decline. The December inflation reports had inflation still over 3%. But stripping out OER (owner’s equivalent rent which has lags), US inflation has been running around 2% for six months now. That would mean that the Fed has accomplished its mission and should start cutting rates.

But the labor market is still tight and wages are rising by roughly 5% YoY. How do you get 2% inflation with 5% wage growth? Right now it’s thanks to falling commodity prices and the end of the Covid-related supply shocks.

So there’s a possibility that we see inflation re-accelerate from here if oil prices rise dramatically or the shipping disruptions in the Red Sea continue to worsen. And that’s not something the markets are prepared for.

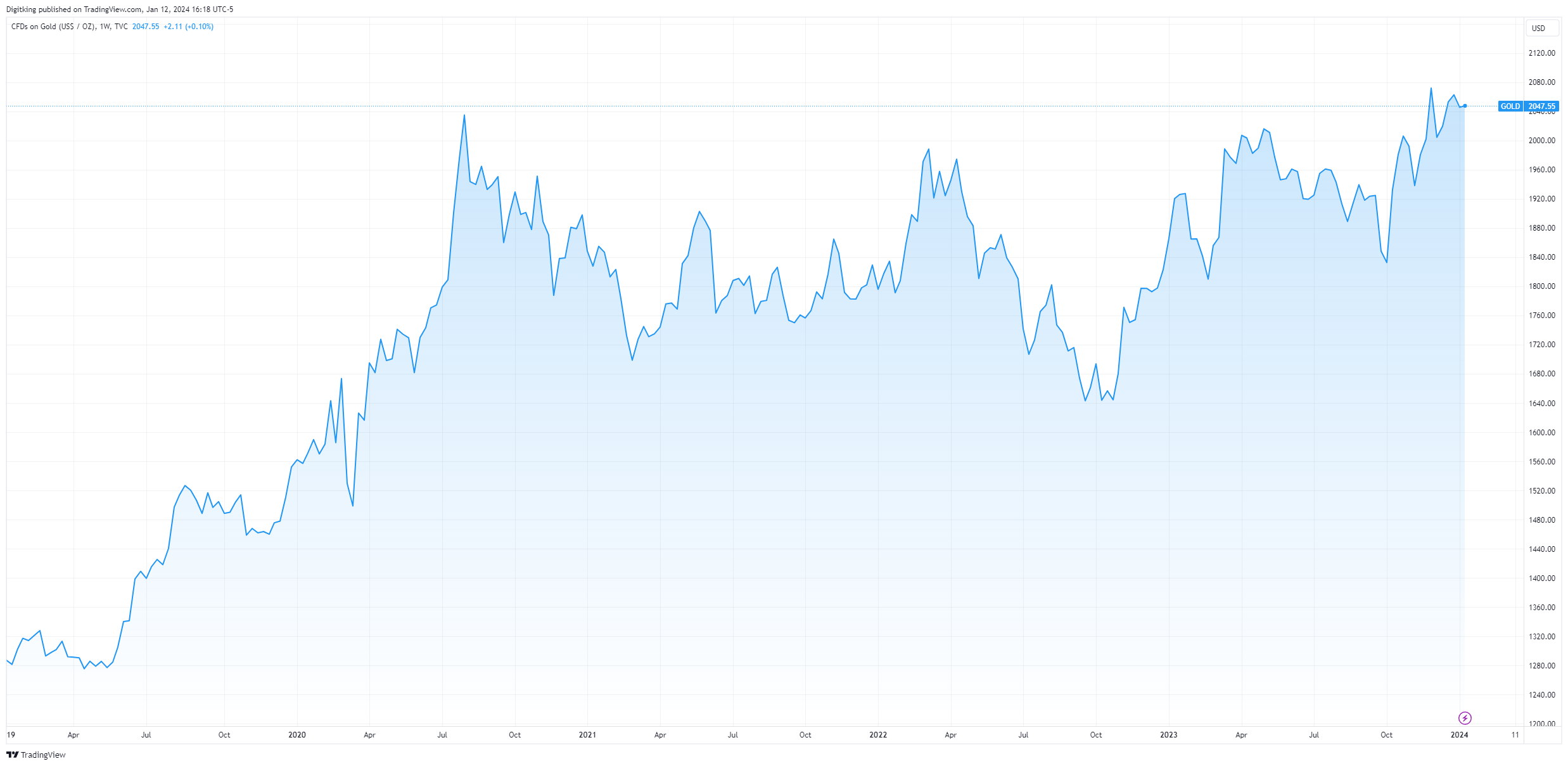

One asset class that has been quietly booming over the last couple of years has been gold. Since Russia’s invasion of Ukraine and the Western world’s response by seizing their foreign reserves. Gold has steadily grinded higher from ~$1800/oz to now almost $2050/oz. Going even further back; it has almost doubled from the end of 2019 and yet almost no one is talking about it:

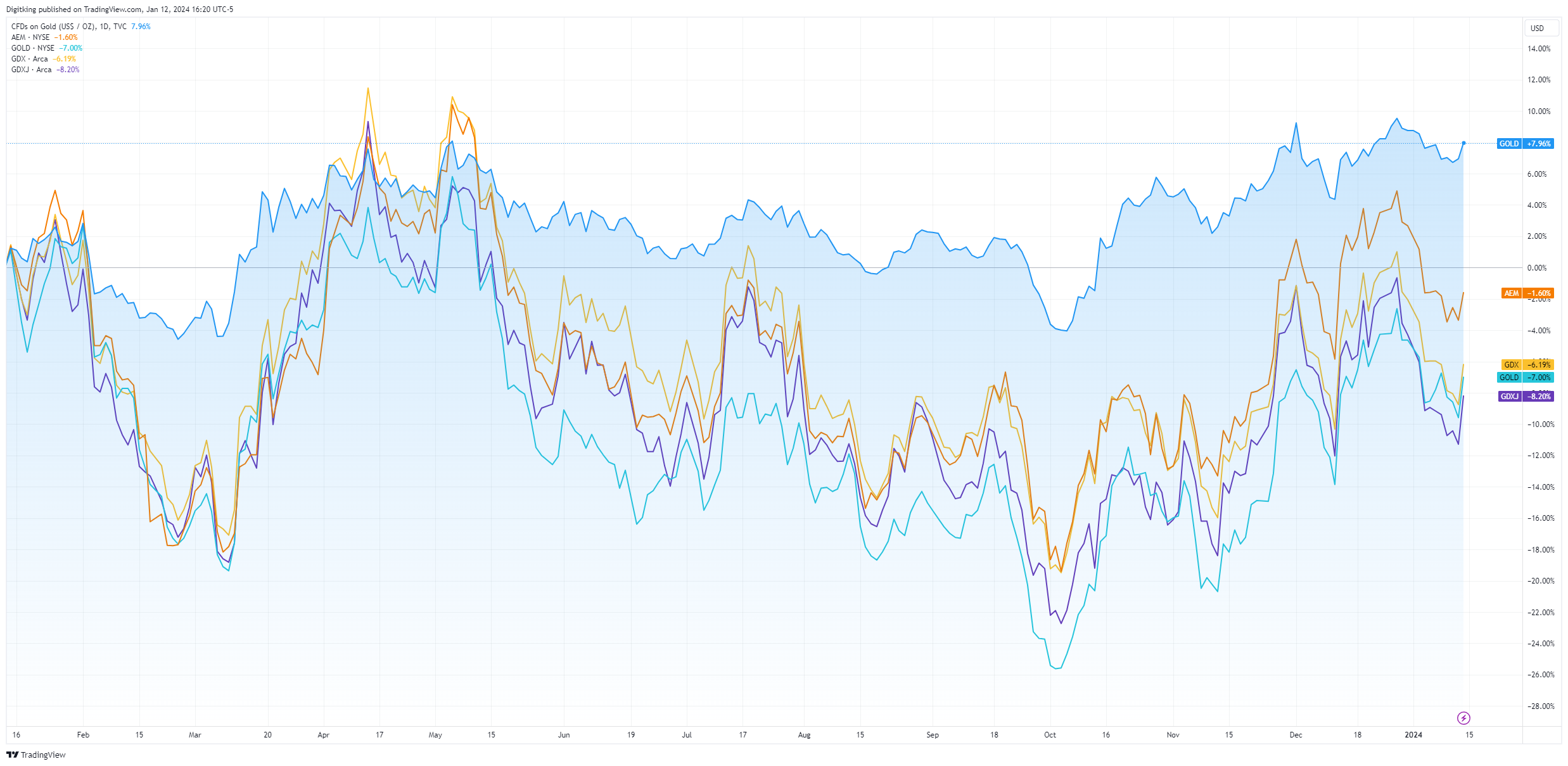

The bull market in gold has not spread to the gold miners as they’ve lagged the rally (especially over the last year). Here are just the one-year returns of gold versus Agnico Eagle (in the Canadian Portfolio, orange line), Barrick (another large gold miner, teal line) as well as the VanEck Gold Miners ETF (GDX, yellow line), and VanEck Junior Gold Miners ETF (GDXJ, purple line):

On top of rising gold prices, diesel prices have fallen dramatically so gold miner profits are going to be through the roof. And again yet few investors care.

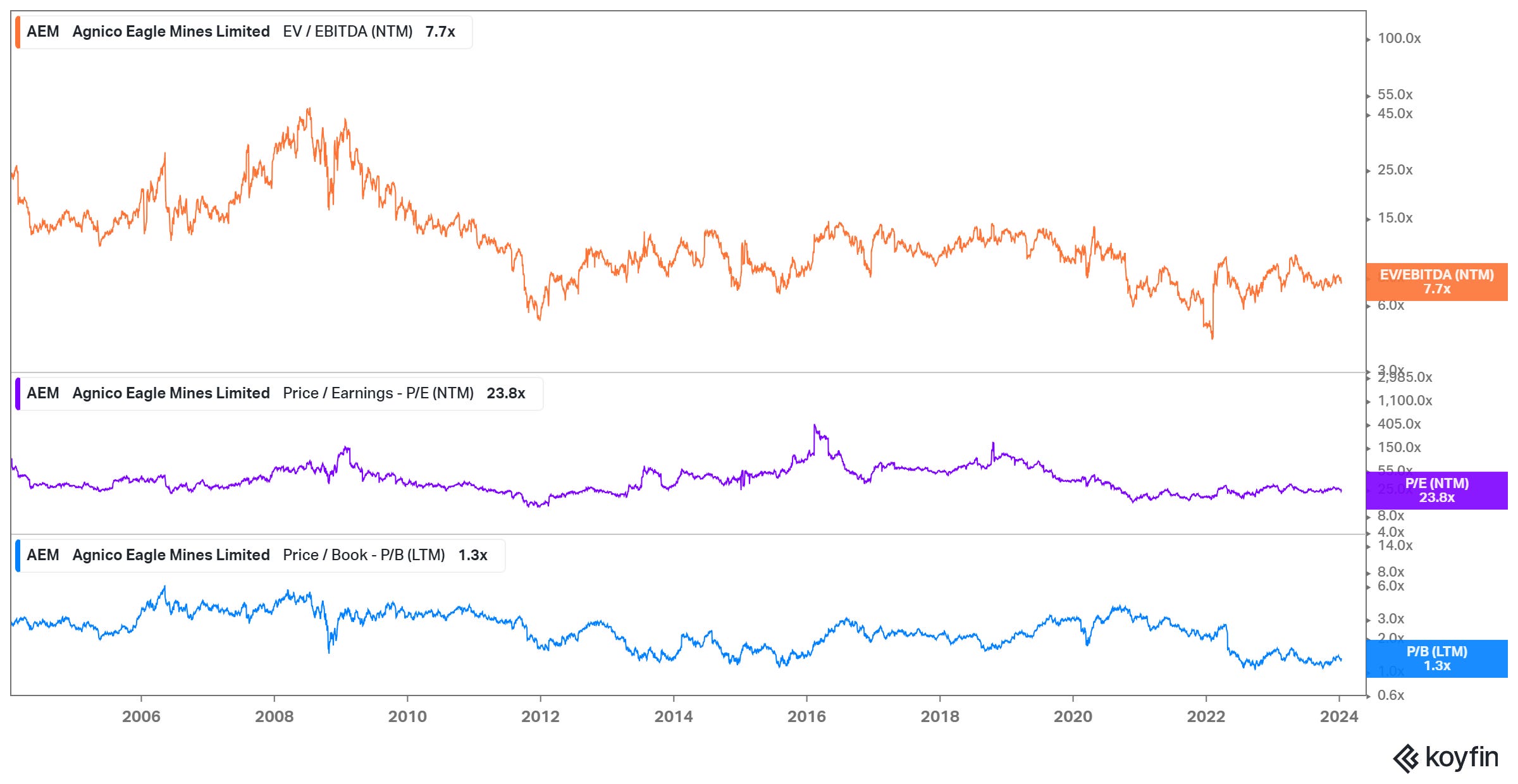

Agnico Eagle (AEM) has been a long-time holding in the Canadian portfolio. It’s one of the best-managed miners in the world with (almost) zero geopolitical risk and a very long track record of shrewd acquisitions and prudent capital allocation.

Since the gold bubble popped in 2011, there have been few times that Agnico shares have ever been cheaper. On most metrics, Agnico’s valuation has fallen by 66% to 75% from its bubble high:

I didn’t include it in my 2024 Surprises (which can be found here), but as things currently stand I think that gold miners could be the best-performing sector this year.

Before I end, I have to point out something extraordinary. In my 2024 Surprises, I predicted that Microsoft would overtake Apple (there was a ~200 billion gap between the two at the end of December). I was very certain of this (I ascribed a 75% probability) but even I was stunned when it happened last Thursday (January 11th). The markets move so fast these days!

The weighted average sum of my predictions had a 39% probability. So if I get 4 or more right I would consider that a success. I’m now already 25% of the way there.

Trades

None for January

Performance Update

Canadian Portfolio:

Global Portfolio:

Portfolio Holdings

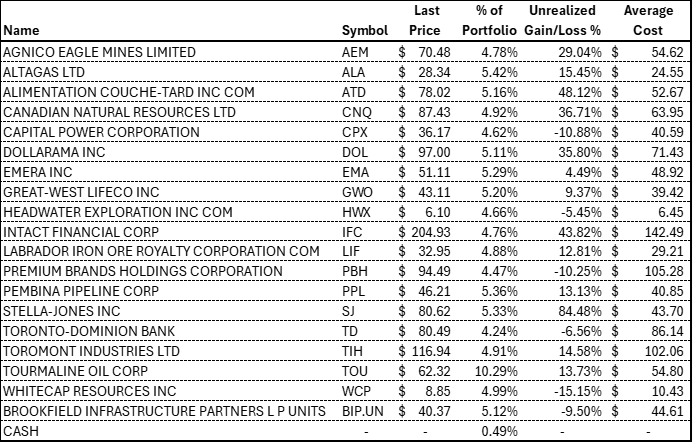

Canadian Portfolio:

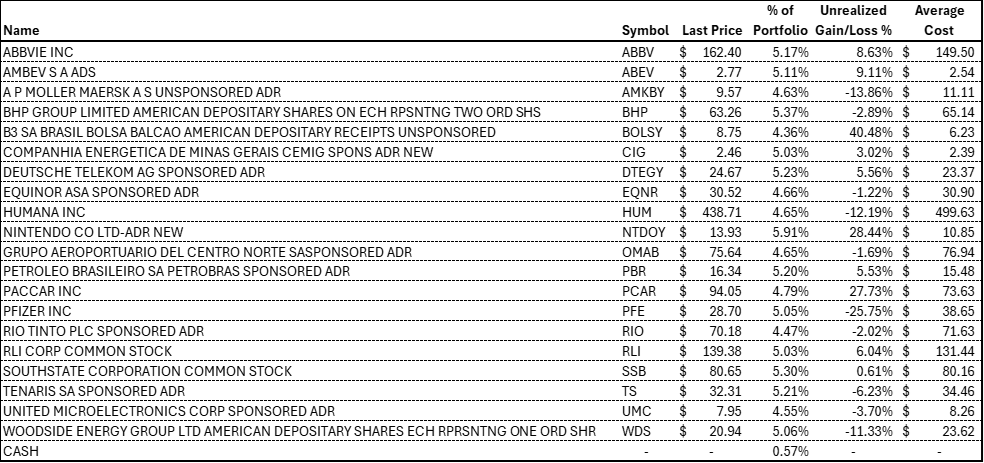

Global Portfolio:

Recommended Readings:

The war in Gaza may widen. The Biden admin is getting ready for it. That could put President Joe Biden in the center of a messy Middle East conflict in the midst of a bruising re-election campaign.

The Bond Market Rally Is Overlooking a Soaring $2 Trillion Debt Problem. Investors are ignoring the cloud of rising deficits around the world.

A Dozen Reasons To Remain Bullish In 2024. An excerpt from the Yardeni Research Morning Briefing, December 18, 2023.

Disclosure: I am long and have a beneficial interest in all of the above-mentioned securities. I may change my holdings at any time post-publication.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.