Sleepy Portfolio - March Edition

Hi everyone,

I'm skipping the pleasantries this month as there’s lots of (unfortunately) talk about. While the Canadian portfolio had a nice bounce back in February, the Global portfolio continues to struggle.

I’ve spent a lot of time thinking about what to do and there are no good options. There’s an irony that value investors (me included) have complained that once it becomes a “stockpickers market”, it’ll be their time to shine. Unfortunately, the last 12 months have been a “stockpickers market”, it’s just that the bull market has been in stocks that no value investor (or quality/low volatility) would ever own.

Like starting a value fund at the end of 1998; starting the Global portfolio (that tilts toward dividends, quality, value, and low volatility factors) couldn’t have had a worse start.

While preparing this month’s write-up and thinking about what to do. I came across some charts that hopefully help explain what’s going on in the markets.

From Deutsche Bank, positioning in mega-cap growth is getting extreme and the knock-on effect is that it’s pulling capital away from other companies and sectors.

Meanwhile, JPM shows that the momentum facotr (i.e. stocks that are going up) continues to accelerate. In short, winners are winning by the largest margin since the dot-com bubble. The flipside of course is that if your stock isn’t going up, then it’s probably going down.

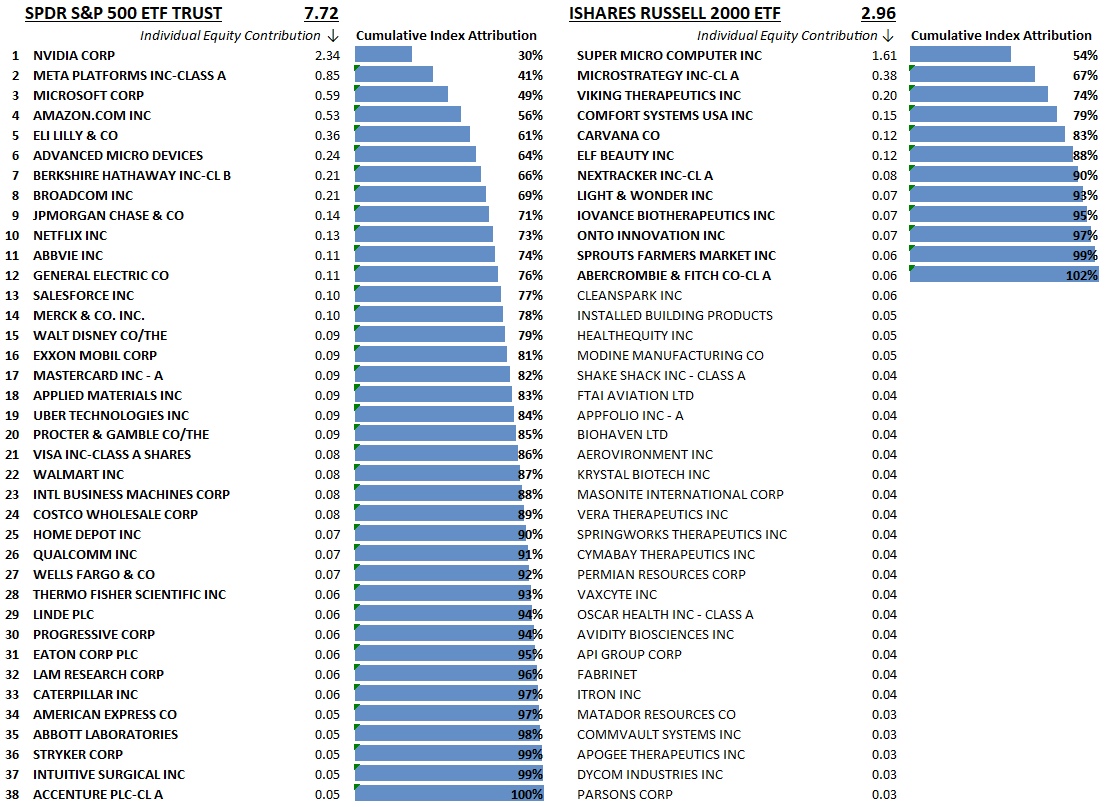

I struggle to find good data on global markets, but the US capital markets now make up over 60% of global market capitalization so it’s still reasonably representative.

Year-to-date attribution analysis shows that 3 (out of 500) stocks have contributed to half of the S&P 500 returns (US large caps). In small cap world (using the Russell 2000), 3 companies have contributed a staggering 75% of returns.

In short, if you haven’t owned the winners year to date (or last year), it’s been a very rough time.

And finally, here’s a nice factor US chart by Koyfin for the last year.

Dividends, low volatility, value, and small-cap factors are all down 10% or more. The buyback factor is doing slightly better being down only 7%. Quality has held up ok, generating a

The global portfolio focuses on the quality, dividend, and low volatility factors with a small weighting to value. The weighted average of these factors is down about 7%.

But that doesn’t explain all of the underperformance itself. Part of the problem is that the portfolio has been weighed down by materials (mining), energy, and healthcare (which make up ~40% of the portfolio).

Out of this group, there have been two winners in this group (Abbvie and Tenaris), 2 big losers (Pfizer and Humana), and 4 that have been flat for the last year (BHP, Rio Tinto, Equinor and Woodside).

When markets are up over 20% (like they have for the last year), it’s just not good enough. So I’ve decided to change the model and focus on shareholder yield (dividends plus share buybacks) as well as make some other minor tweaks.

The rankings don’t change all that much but hopefully it leads to better performance. In the process, I’ll be selling Woodside Energy whose ranking has tumbled due to low LNG prices while investing the cash from the Petrobras sale into US shale driller Diamondback Energy (FANG) and French energy super major Total Energy (TTE).

For Humana, under the revised ranking rules it’s still in the top quartile so I’ll keep it for now. But Pfizer is near the bottom. For better or worse, I’m going to override the model and hang on to it. It’s very cheap and hated and I think they spent way too much time (and money) focused on Covid. The business is slowly turning around so I’ll give it another 6 months.

As for the Canadian portfolio, things aren’t so bad. February was good and March so far is looking decent as well. I’ve decided to sell the Tourmaline position (which is a 10% weight) and replace it with energy royalty company Freehold (FRU) and Imperial Oil (IMO).

Tourmaline Oil is a fantastic company that still scores very highly and its President and CEO just won the “Canadian CEO of the Year” award. But the company doesn’t produce that much oil anymore. It mainly produces natural gas and some liquids.

The whole team there has done a masterful job navigating the markets over the last couple of years. Just because natural gas prices are low, it doesn’t mean they can’t go lower. Natural gas inventories are very high and if we have a mild or even normal summer, natural gas prices could go a lot lower (maybe even zero). So I’ve decided to not take the risk and sell the name. I’m still very bullish on oil, especially Canadian oil with the completion of the TMX expansion soon, so I’ve added the two highest-ranking energy companies on the list which are FRU and IMO.

So have a great March everyone and hopefully come April I’ll have more positive news to share!

Trades:

Sleepy Global Portfolio:

Sales:

Woodside Energy (WDS)

Purchases (5% target):

Diamondback Energy (FANG)

Total Energy (TTE)

Sleepy Canadian Portfolio:

Sales:

Tourmaline Oil (TOU)

Purchases (5% target):

Freehold Royalties (FRU)

Imperial Oil (IMO)

Performance Update

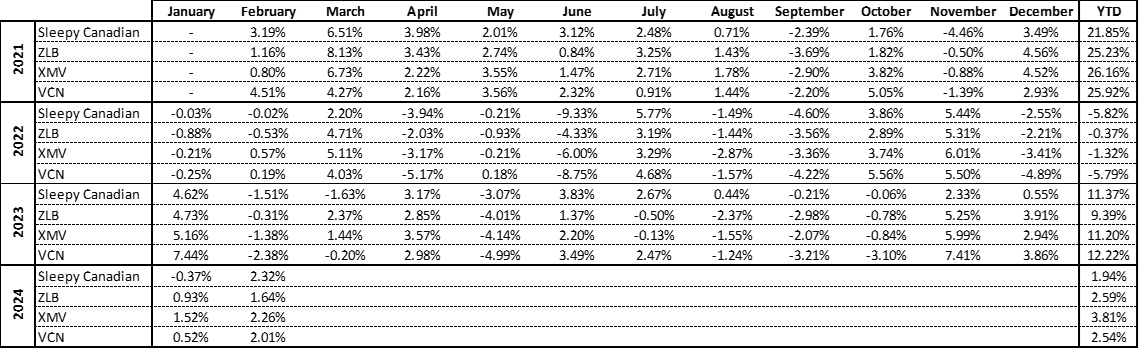

Canadian Portfolio:

Global Portfolio:

Portfolio Holdings

Canadian Portfolio:

Global Portfolio:

Disclosure: I am long and have a beneficial interest in all of the above-mentioned securities. I may change my holdings at any time post-publication.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.