Trade Idea - Buying the dip in Canadian Energy

Trade Idea - Buying the dip in Canadian Energy

Hi everyone,

I was planning to write something every week and publish it on Fridays (albeit not as long as the first one), but this one is a little bit more time sensitive so I figured I would publish this now.

What I am proposing is highly risky with a possibility that it could lose 100% of its value. This trade idea should not be considered as investment advice or a recommendation to trade. Please consider the risks carefully and consult with a registered investment advisor first before taking any actions.

The Trade

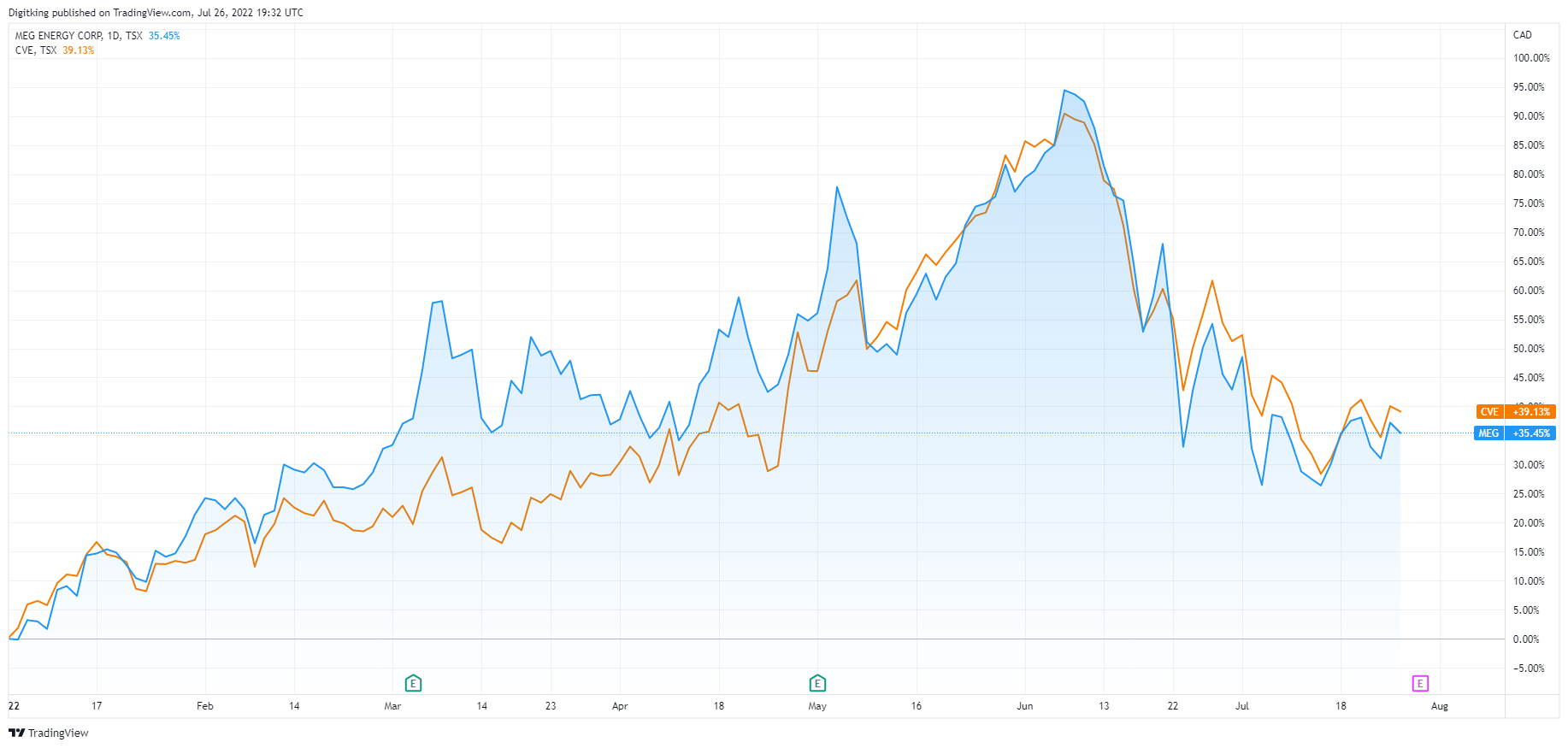

Generally, I’m a long-term investor and can go weeks and sometimes even months without making a trade. But the recent pullback in energy stocks, including high-quality blue chip Canadian names, combined with a number of catalysts in the next couple of months has led to a short/medium-term trading opportunity.

The trade ideas are to buy a bull-call spread on two high quality Canadian oil and gas companies:

Long MEG.TO $19 December call and short the MEG.TO $24 December call for an approximate cost (using the midpoint) of CAD$1.20/share (big:1.03, ask: 1.33)

Long CVE.TO $25 December call and short CVE.TO $30 call December for an approximate cost (using the midpoint) of CAD$1.15/share (bid: 1.06, ask: 1.26).

For these call spreads, the share prices don’t have to make a new high, they simply need to retrace back to their June highs over the next 140 days for a maximum payoff.

Unfortunately, as anyone that’s traded in Canadian markets knows, Canadian options are extremely illiquid and expensive to trade. MEG is only listed on the pink sheets in the US so there are no USD options available. CVE does trade on the NYSE so a comparable USD call spread trade would be the following:

Long CVE.N USD$20 December call and short CVE.N USD$25 December call for an approximate cost of USD$0.95/share (bid: 0.85, ask: 1.05).

By trading in the US, you get much better liquidity and lower trading costs, but you will take FX risk. The $CAD has been pretty volatile with a number of swings between 1.245 on the low-end and 1.315 on the high end so it’s something to keep in mind.

In all three cases, you’re risking ~CAD$1.15-1.20 (which could turn into $0) with the upside of making as much as $5 if everything turns out. This is obviously a very high-risk strategy and Interactive Brokers gives the probability of payoff at 33%.

Thesis

Canadian oil and gas stocks are extremely cheap and are producing the most profits and cash flows in a decade (even with the recent pullback in oil prices). Since peaking in early June, they’re down close to 30% on recession fears and central bank tightening.

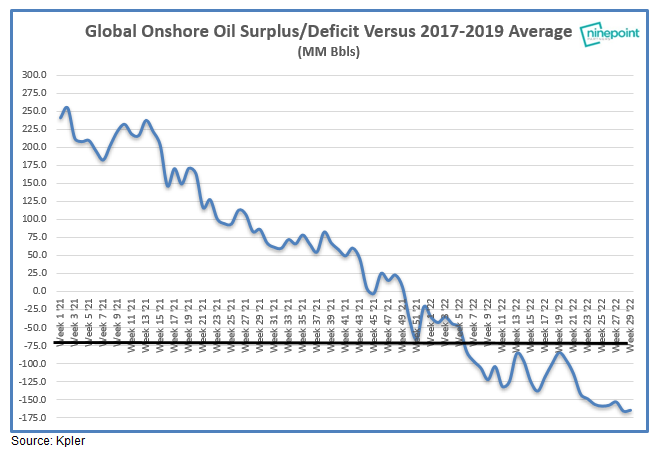

However, global oil inventories continue to decline and the physical oil market remains extremely tight.

Meanwhile, governments all across the world are handing out energy subsidies to offset the rise in energy prices which is preventing significant demand destruction like what we’ve seen in past recessions.

I for one hate paying for theta (i.e. time value of options), but there are a number of catalysts over the next couple of months:

Earnings: Both CVE & MEG report Q2 earnings on Thursday (July 28th). This might get overshadowed by the Fed meeting tomorrow, but it’s still a chance to remind investors and the rest of the market both how cheap they are and how much money they’ll be able to make (even at $95 oil). They’ll also be reporting Q3 results sometime in October which will be covered by the options period.

Most generalists have largely remained on the sideline and significantly underweight energy companies. A change though might already be underway. Capital Group, one of the world’s largest asset managers with USD$2.6 trillion in assets, initiated and acquired ~15% of Tourmaline’s shares outstanding, initiated and acquired 5% of MEG’s shares outstanding, all the while significantly adding to their holdings in CVE and CNQ in just Q2.

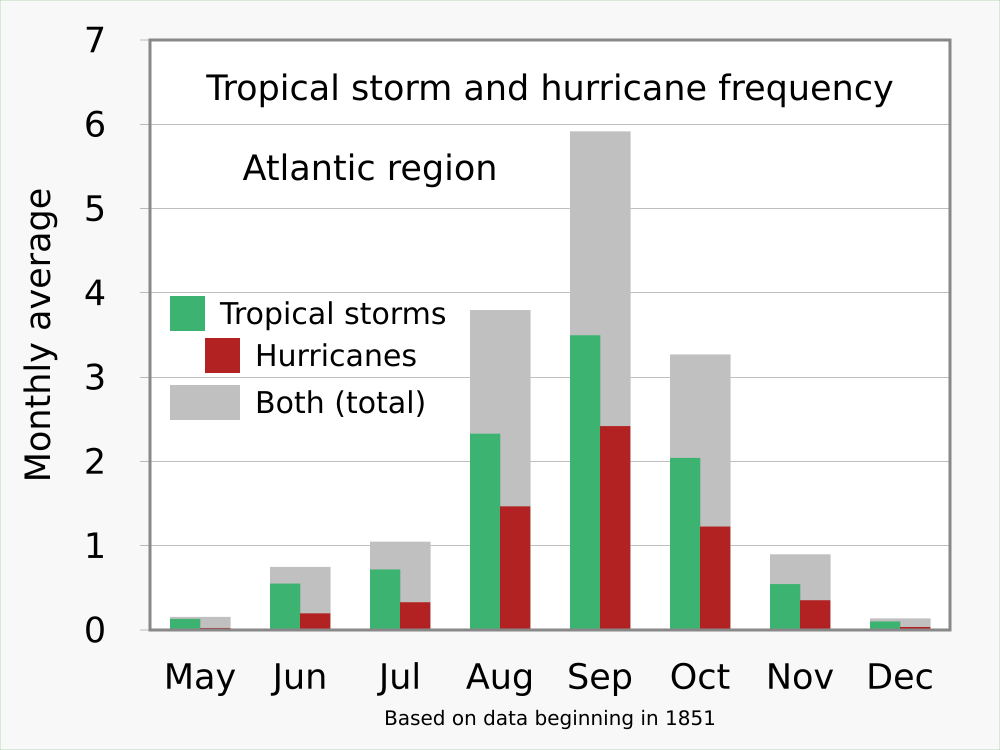

Hurricane season: The Atlantic/Gulf of Mexico hurricane season officially runs from June through November. However, the vast majority of hurricanes occur in August, September, and October.

Last year (2021), Hurricane Ida knocked out almost 80% of Gulf of Mexico oil production for an extended period of time. In 2019, Hurricane Barry temporarily knocked out 70% of Gulf of Mexico oil production.

This year, the National Oceanic and Atmospheric Administration (NOAA) is warning that the hurricane season will likely be above average due to the La Nina effect (so far it’s been very quiet though).

The Gulf of Mexico, which produces approximately 1.7mm b/d, is now crucial to the global energy balance. In the past, large disruptions due to Hurricanes would mean little because there was sufficient supply capacity globally to offset it. But given how tight the oil markets currently are, a major storm that shutdowns a significant portion of GoM production for an extended period of time could cause oil prices to spike just as much (or more) than the initial Russian invasion of Ukraine.

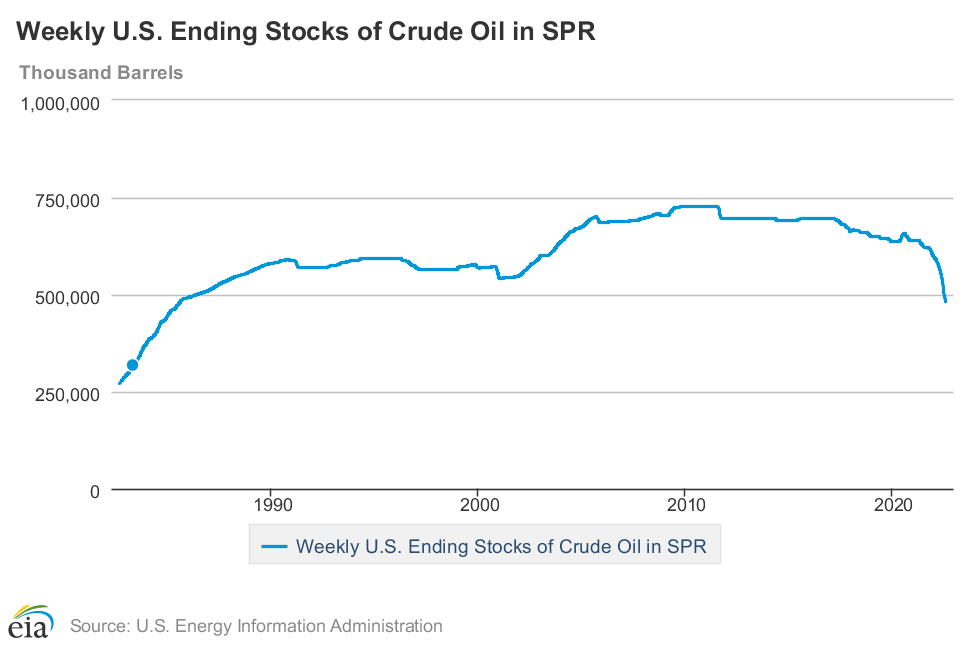

SPR relief. In response to the high oil prices, the Biden administration has been releasing 180mm barrels at a rate of 1mm bb/d of oil from its strategic petroleum reserve (SPR). This is clearly a political move to try and curb surging gasoline prices and rescue the administration from the public’s wrath.

The SPR releases have definitely played a role in bringing down oil prices, much to the chagrin of energy investors. The upside is that the SPR releases will likely end around the US mid-term elections on November 8th (if not before). In addition, SPR inventory levels are at their lowest level in ~30 years, and much of it will need to be repurchased and refilled later down the line which would boost oil strip pricing.

JCPOA is DOA. The Joint Comprehensive Plan of Action (JCPOA) aka the Iran nuclear deal seems to be dead now. I’m not an Iranian or geopolitical expert by any means, but it seems unlikely that a new deal that has been promised since Biden was elected just doesn’t look like it’s going to happen.

Recently, Iran removed numerous surveillance cameras from its nuclear sites (making it impossible to track Iranian nuclear activity) and arrested numerous foreign diplomats involved in the nuclear negotiations. Meanwhile, Biden’s administration has unveiled new sanctions targetting Iran’s oil exports.

While there’s desperation in Europe to salvage the deal, it seems like it’s only a matter of time before the negotiations end completely. This is likely bad for Middle Eastern stability and geopolitics, but bullish for energy prices.

M&A Pop (for MEG). Canadian oil and gas companies are flush with cash and running out of debt to repay. And the oil patch has seen an incredible amount of consolidation over the last 12 to 18 months.

MEG has been discussed as a takeover target for as long as I’ve worked in the industry (it’s almost a running joke at this point). But if there was ever a time for a large E&P to acquire MEG (such as Canadian Natural Resources), now would likely be the time.

There are fewer companies or assets to choose from and MEG’s assets remain very high quality and come with a large tax loss pool. Overall I’d put the chance that this happens as very low(<10% probability), but if there was ever a time for a large E&P (such as Canadian Natural Resources) to take a swing at acquiring MEG, it would be now.

Cenovus is too large at this point to be considered a takeover target though.

Risks (aka what could go wrong)

As I mentioned at the beginning, this strategy is very high risk with a distinct possibility that the calls end up being worthless. I think there are three big risks that could cause MEG & CVE’s share price to stagnate or go down from here.

Nothing Happens. For the options to be “in the money” and have any intrinsic value, the shares would need to rally by ~10% from here. Currently, the options will lose a little less than 1c/day assuming nothing changes. But that’s life when buying out-of-the-money options and always something that you have to keep in mind.

Recession. A recession is on everyone’s mind and how deep the recession ends up being could play a big role. A mild recession with governments handing out energy subsidies likely means little reduction in overall energy demand or energy prices.

But a deep recession that sees material demand loss could have a big impact. A deep recession could easily take oil prices down to or below $70/bbl and there’s zero chance that E&P prices go up in this kind of environment.

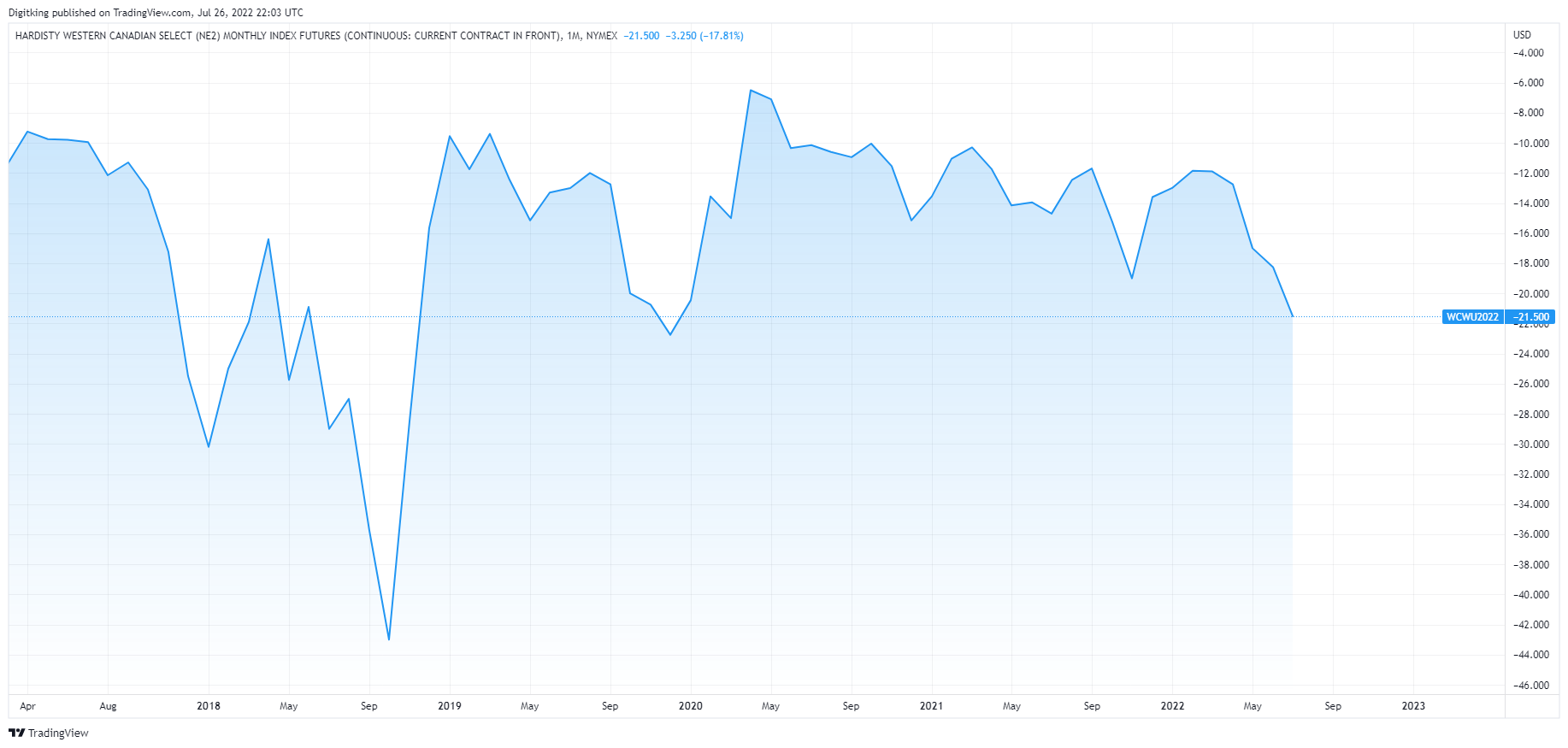

WCS Discount. Canadian oil trades at a discount to WTI because of a lack of takeaway capacity. The gap widens when takeaway capacity is limited and shrinks when capacity is ample.

Historically, the WCS discount has widened over the winter and shrunk during the summer. Unfortunately this year, the discount has already started to widen due to the oil patch increasing production in response to higher oil prices while the Trans Mountain expansion completion was pushed back from Q3 of this year to the middle of next year.

I worry that we might see a replay of 2018 where the WCS discount approaches $40 (i.e. if WTI is at $90, WCS is at $50) and this would be just as crushing to Canadian E&Ps as a deep global recession.

Conclusion

For me, the risk/reward of these call spreads are enticing. I’m going to try and put on one of these positions tomorrow assuming I can get a reasonable price ahead of earnings. I’ll hold off on the other until next week or the week after (hoping for a pullback). Given the downside risks, these are going to be tiny positions (likely 1% positions) with an asymmetric payoff profile.

Hopefully, everyone found this interesting, and if not just let me know so I can make changes for future articles.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.