Company Highlight - Compania Cervecerias Unidas S.A.

Company Highlight - Compania Cervecerias Unidas S.A.

Hi everyone,

Last week I wrote about a possible rebound in LATAM after a very difficult decade. One of the possible positive catalysts that I referenced was the Chilean constitutional referendum this past weekend.

The polling indicated that the proposed constitution would be rejected by voters. When the ballots were down and counted, the defeat was much larger than expected. 62% of the voters rejected the constitution versus just 38% that voted for it.

The Chilean constitution still needs to be rewritten (almost 80% of Chileans agree on that) and how things go from here are still undetermined. President Boric has promised to return to Congress and find a pathway forward to a more moderate constitution but this is overall a positive step.

Chile, like much of South America, still needs to grapple with extreme levels of wealth and income inequality as well as high levels of crime and corruption. But the wacky constitution that was proposed wasn’t a viable solution.

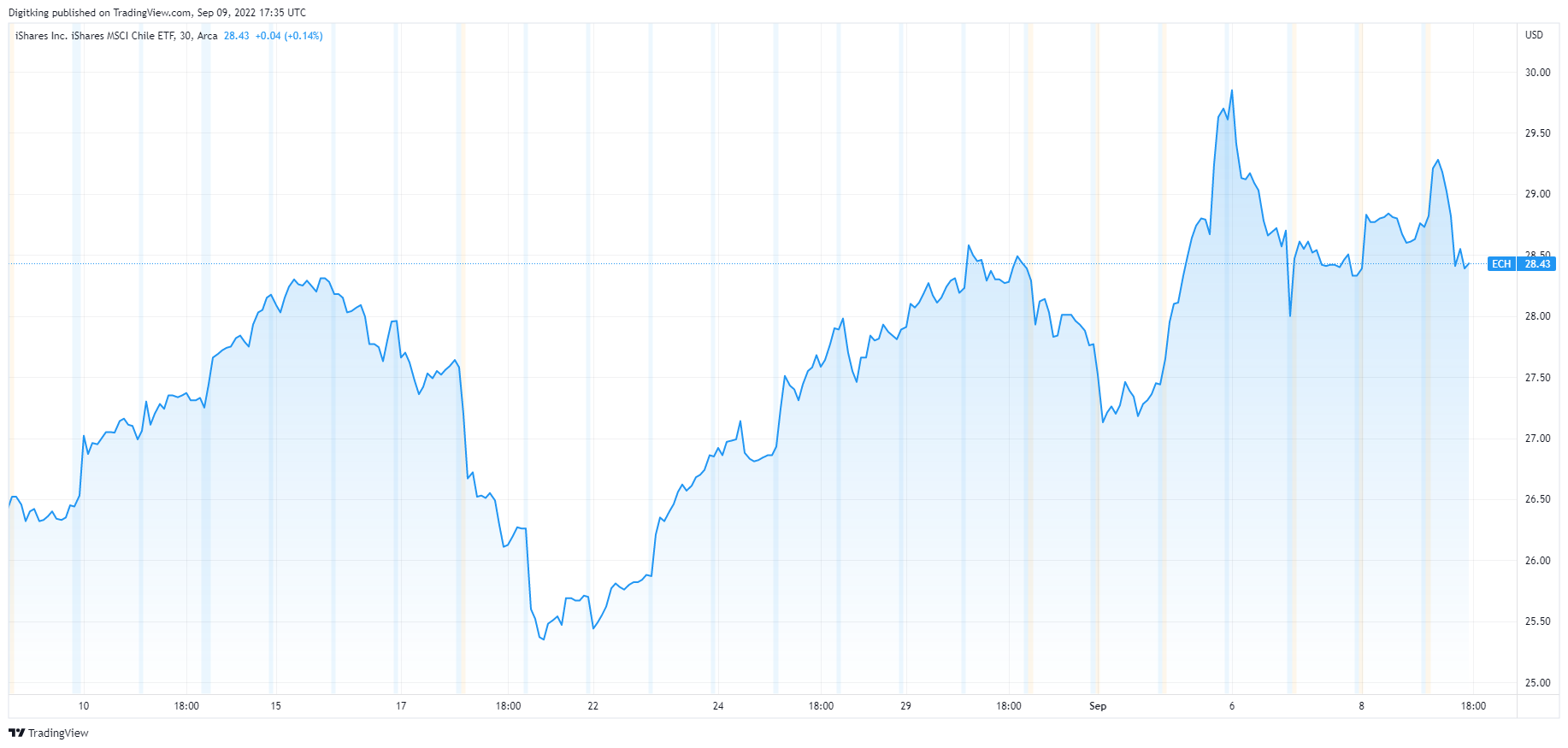

As is often the case with markets, the age-old adage of “buy the rumor, sell the news” was true for the Chilean markets as they peaked yesterday morning and given back almost all of its gains:

That being said, there’s still lots of value to be had in LATAM and I’m highlighting one company where I have a very small position. Again, this isn’t meant to be an in-depth research report but more a high-level summary that might pique your interest.

What Is Compania Cervecerias Unidas S.A.?

Compania Cervecerias Unidas S.A., translated into English as “United Brewery” is Chile’s largest brewer and either the 1st or 2nd largest brewer across much of South America. But they are much more than just a brewer too, they also import and distribute Pepsi and Heineken products for much of South America.

The ownership structure is split into three vehicles. IRSA owns ~2/3 of the company, the US-listed ADR represents ~20% of the ownership and the remainder (~13%) is owned publicly via the Santiago stock exchange.

IRSA is a 50-50 joint venture between Heineken and Quinenco, which is Chile’s largest conglomerate. So in summary, Quinenco owns ~33% of the company, Quinenco owns 33% of the company and public investors own the other 1/3 of the company (including Calgary-based Mawer which owns about ~2.5% of the company).

What Makes It Interesting?

United Brewery is a classic “compounder” stock. It’s not a sexy business or industry (despite what the marketing would lead you to believe), but it’s one of steady growth and consistent returns.

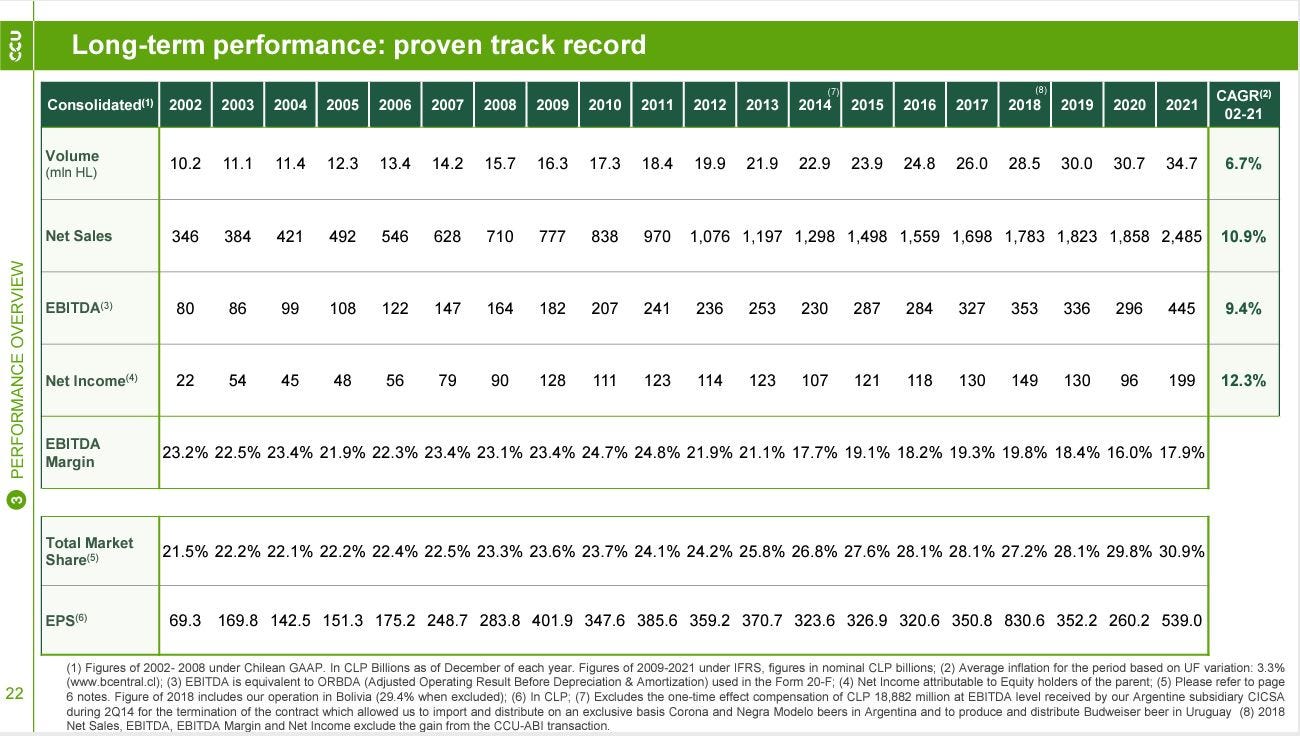

As we can see in the following slide, CCU has steadily grown over the years during the good times and bad.

Future growth looks solid too as LATAM consumers only consume ~1/2 to ~2/3 of what North American and European consumers consume. However, achieving those levels of consumption will require continued economic growth and greater disposable income for the average person.

Their margins took a big hit after losing the right to distribute Budweiser’s products so it’s unlikely that they’ll get back to 23-24% EBITDA margins. But overall the company continues to grow organically and increase its market share.

In spite of the steady and solid growth, the company’s valuation has rarely been cheaper. Here is the company’s historical EV/EBITDA:

Of course, no one valuation metric is perfect so here’s the company’s TTM P/E and P/B:

Not only is the company cheap on a historical basis. It’s also cheap on a relative basis:

Admittedly, the companies I’ve chosen to compare CCU with are much bigger and more diversified. They have less risk and deserve a valuation premium, but a 60% - 75% discount for CCU seems a bit extreme; especially considering that CCU has better long-term growth prospects.

The comps table does show one big problem, and that’s that the company’s net income margin, ROE & ROA have all been pretty weak over the last year. This is due to the double whammy of rising commodity prices and weakening of the Chilean Peso (well really the strength of the USD against all currencies).

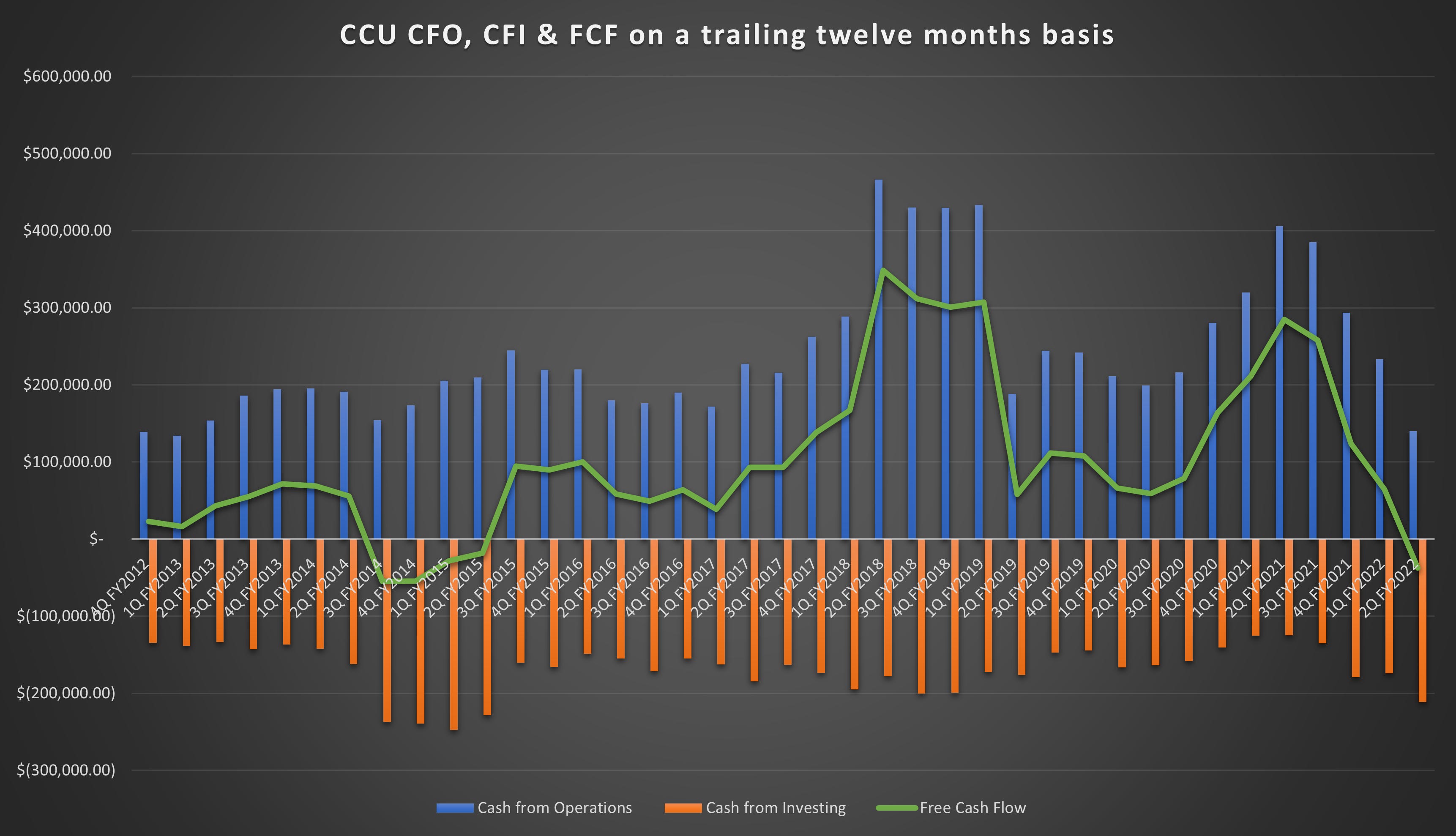

It also shows up in the company’s cash flow from operations and flows down to its free cash flow. Here’s a quick chart showing CCU’s CFO, CFI & FCF. Although I’ve smoothed it by using TTM (trailing twelve months):

Over the last 10 years, CCU has been able to convert on average about 6% of its total net revenues into free cash flow. If we assume that the current pricing pressures ease (which is already happening to some degree). And the South American currencies, particularly the Chilean Peso stabilize, the company should be able to generate about 162 billion in free cash flow (in Chilean pesos) based on the current revenue run-rate.

Based on current exchange rates (0.0011 Peso to USD), this works out to ~180mm in free cash flow or USD$0.483 in FCF/share. But each ADR is worth 2 shares so it’s actually USD$0.966 in FCF/share for US investors.

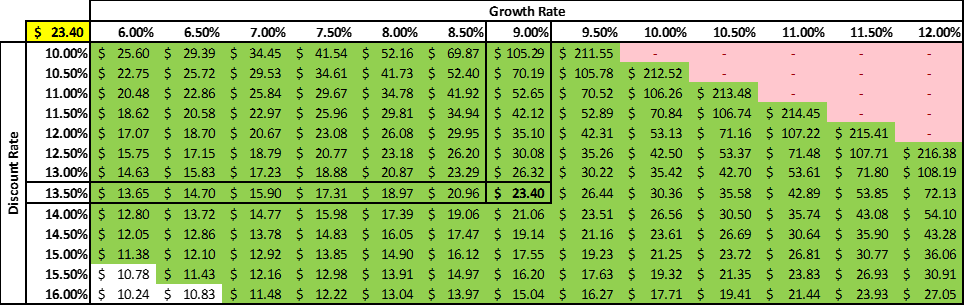

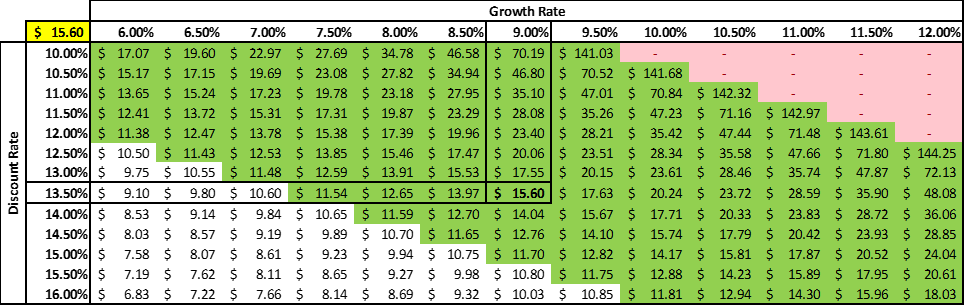

The reason I bring this up is for a fairly steady business such as CCU, I like to use a modified version of the basic dividend discount model (where I substitute the dividend for free cash flow). Assuming a 9% growth rate and a 13.5% discount rate, I get to an approximate value of USD$23.40/share (which would imply significant undervaluation). But I’ve never found a single point all that useful, so instead I prefer to look at a range and try and understand what the market value is implying.

In the following chart, I highlight in green all of the situations where the implied value of CCU is greater than its current share price (the ADR is approximately USD$11.10/share as I write this). The cases in white represent scenarios whereby the valuation is below the current share price:

There of course two big caveats to this exercise. First, CCU is able to get back to converting 6% of its total revenues to FCF. And second, it can continue growing by 9% (nominal). If I assume that instead of 6% but instead will only be able to generate 4%, it reduces the valuation to USD$15.60/share and we can see a lot more scenarios where the valuation is less than the current share price:

Overall though, I think the odds are in your favor if you’re a long-term investor. The risks are still present but the low valuation more than compensates for this risk.

For every fundamental (i.e. not systematic like the Sleepy Canadian Portfolio), I try to boil down an investment into two or three key factors that matter. For CCU, I think they are:

Can the company continue to grow at 8% to 12% (nominally) a year?

Can this growth translate into consistent profits and free cash flow (i.e. will we see mean-reversion in profitability now that commodities and currencies have stabilized)?

Are the politics (which currencies are a proxy for) improving or getting worse?

Right now, I think all three are clear. We’ll get more information in October when the company reports its Q3 results and hopefully more clarity on the next constitution sometime this fall (although a new constitutional convention will likely take 1-2 years as well).

One last thing to mention, CCU has a variable dividend policy. They aim to distribute 50% of the company’s net income to shareholders via dividends. This means that the dividend can change quite a bit from year to year. But it also means that it can be quite large (depending on the amount of net income generated and the valuation of the company). I’m not bothered by this but I know many investors (particularly American) do not like receiving dividends and would much prefer share buybacks. So it’s just something to keep in mind (although this variable dividend strategy is quite common for many LATAM companies).

Disclosure: I am long and have a beneficial interest in all of the above-mentioned securities. I may change my holdings at any time post-publication.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.