Macro Thoughts - Will LATAM turn the corner?

Macro Thoughts - Will LATAM turn the corner?

Hi everyone,

Last week, I wrote a pretty negative article about the state of the world. Just to wrap it up, I thought it would be interesting to look at LATAM (Central & South America).

I’m sure older readers are going to roll their eyes when I talk about LATAM, the “perpetual land of opportunity”. But things couldn’t really have gone worse there over the last decade.

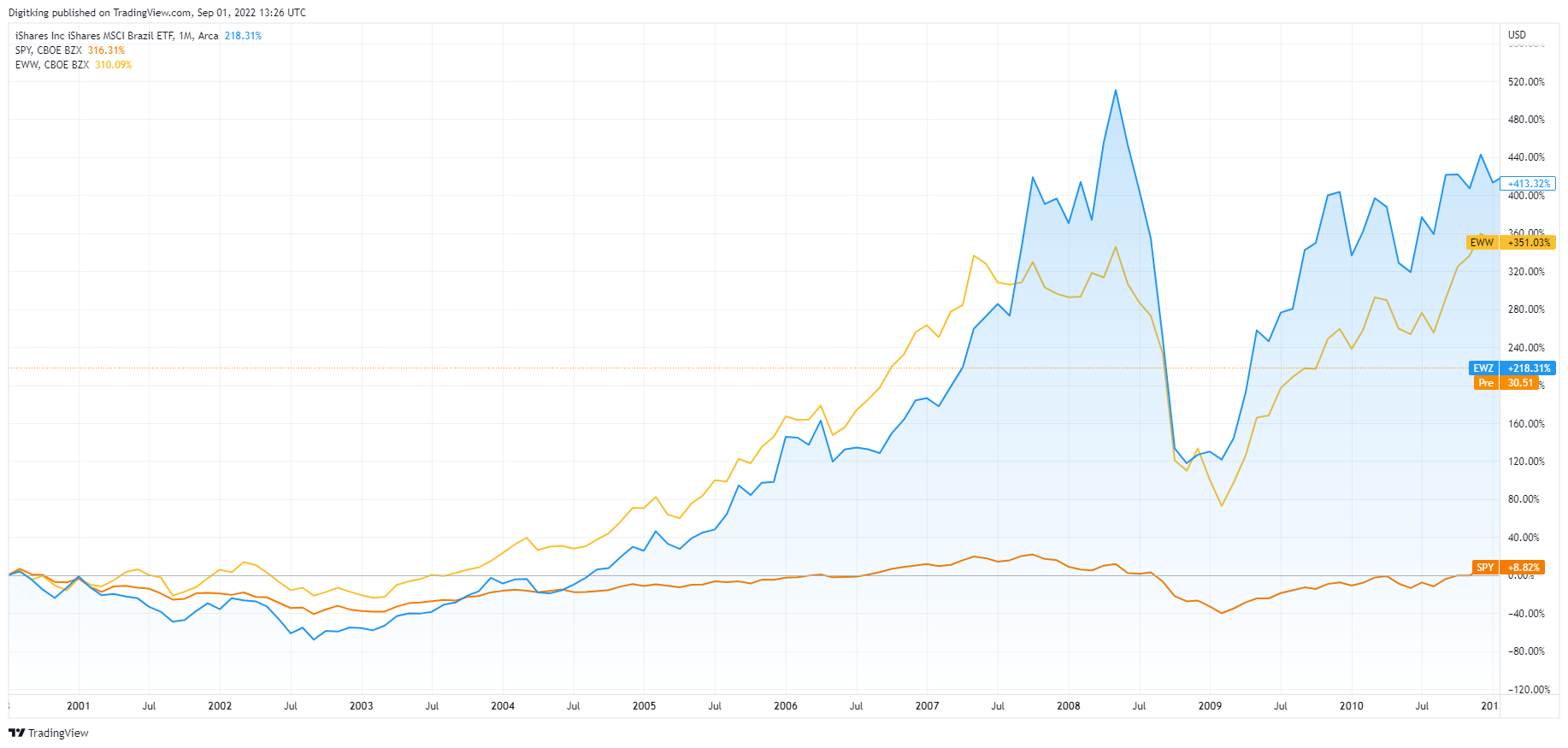

The commodity supercycle during the 2000s caused LATAM economies and their markets to soar. Here are Brasil (EWZ - blue line), Mexico (EWW - yellow line), and the US’s S&P 500 (SPY) from the start of the commodity bull market in the early 2000s to its peak in late 2011:

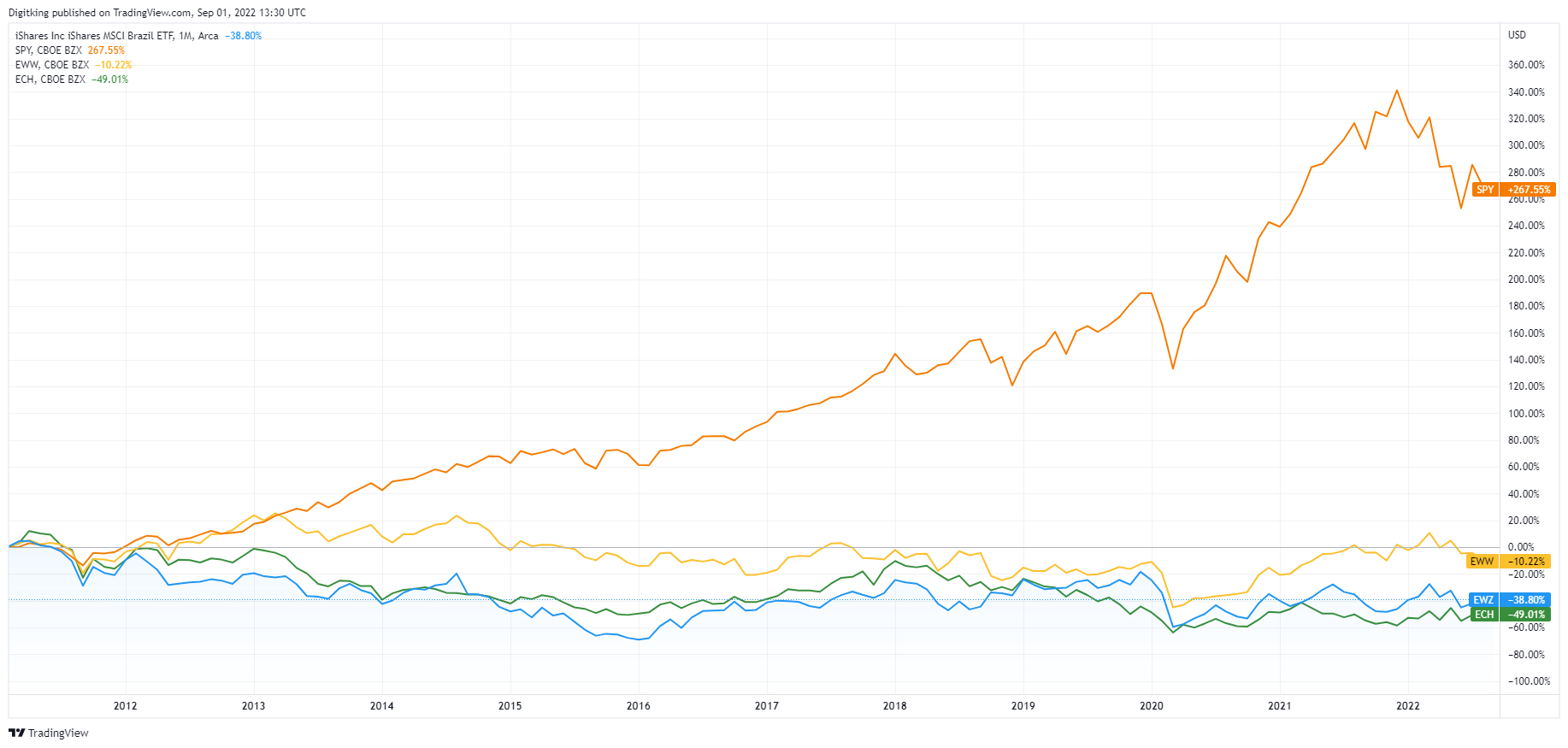

Of course, the boom turned to bust during the 2010s and I’ve added Chile’s market as well (ECH - green line):

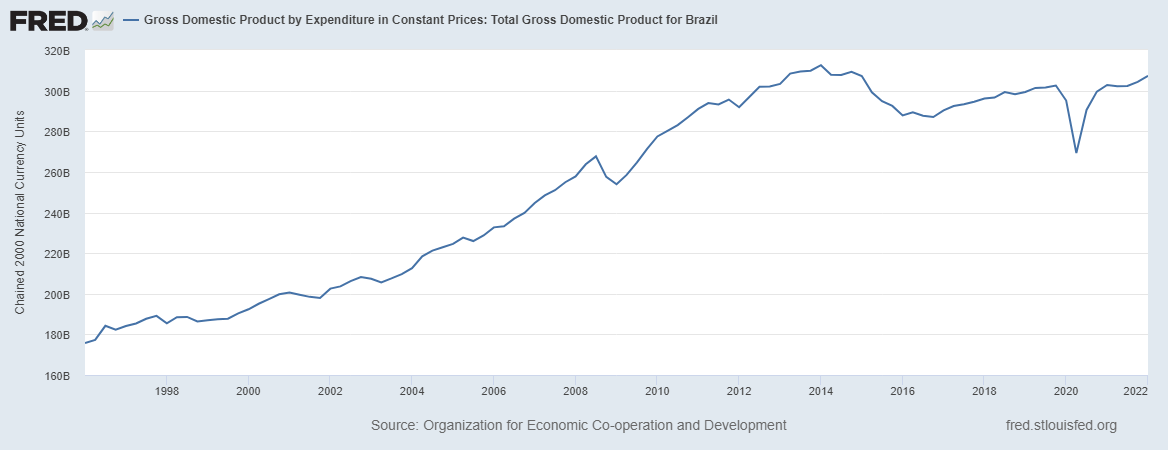

Some will argue that markets aren’t a good proxy for economic development which is fine. But this chart, Brazil’s GDP adjusted for inflation, largely tells the same story:

The same story can be said for much of Central & South America. A lost decade of poor economic growth, poor policies, widening inequality, rising cost of living, and rampant corruption. Sounds familiar no?

What has been the repercussion of all of this? The rise of extremist populist politicians on both the left and right.

5-year summary of political upheval

In 2018, Andrés Manuel López Obrador (often referred to as AMLO) was elected president of Mexico running on a left-wing platform. In fairness to AMLO, since being elected he has pivoted to a centrist and bucks the trends of many other politicians in the region.

In late 2018, the Brazilian people had grown fed up with the political class and were incensed by the bombshell revelations of Operation Car Wash. Their response was to elect far-right wing populist politician Jair Bolsonaro as president.

Since 2017, Peru has been in a series of political crises. There have been so many changes in the Presidency that it’s hard to summarize, but there have been at least 3 Presidential impeachments by my count. In 2021, Pedro Castillo, a far-left populist was elected President of Peru and has already faced (i.e. survived) another 2 impeachment votes. He hasn’t helped his cause either by being extremely erratic and appointing 4 different governments in one 6 month stretch.

Meanwhile in Chile, the country was rocked by violent protests in 2019 over the rising cost of living and widening wealth/income inequality. This gave rise to Gabriel Boric, a young left-wing politician, being elected President of Chile in December 2021. As part of his platform, he promised a new very left-leaning constitution that would radically remake Chile.

Then there’s Colombia. In June (2022) a former Marxist rebel and mayor of Bogota, Gustavo Petro, became Colombia’s first left-wing President. His election platform included:

Reducing inequality with higher taxes and more state intervention in the economy (standard fare).

Slowly shutting down the entire Colombian oil and gas industry (the country’s largest legal export industry) and replacing it with a “green economy”.

Radically rethinking the war on drugs (including decriminalization of cocaine).

The whole situation though is very unstable because centrist and right-wing parties still control both houses of congress so it could go the way of Peru (though that looks unlikely right now).

And I won’t even touch on the basket cases that are Argentina, Nicaragua, or El Salvador.

You might push back and say “look it’s Central and South America, populist left/right-wing politicians are the norm”. While that is true and I’m no expert, it seems like the last 5 years have been especially tumultuous.

Colombia, Peru, and Chile have historically been right-wing-leaning (often fighting left-wing insurgencies) and have all elected left-wing politicians. Meanwhile, Brazil has often been centrist or center-left leaning but voters last time round elected a far-right wing President. The dissatisfaction with the status quo has meant that voters have sought out “outsiders” who come from the far ends of the political spectrum.

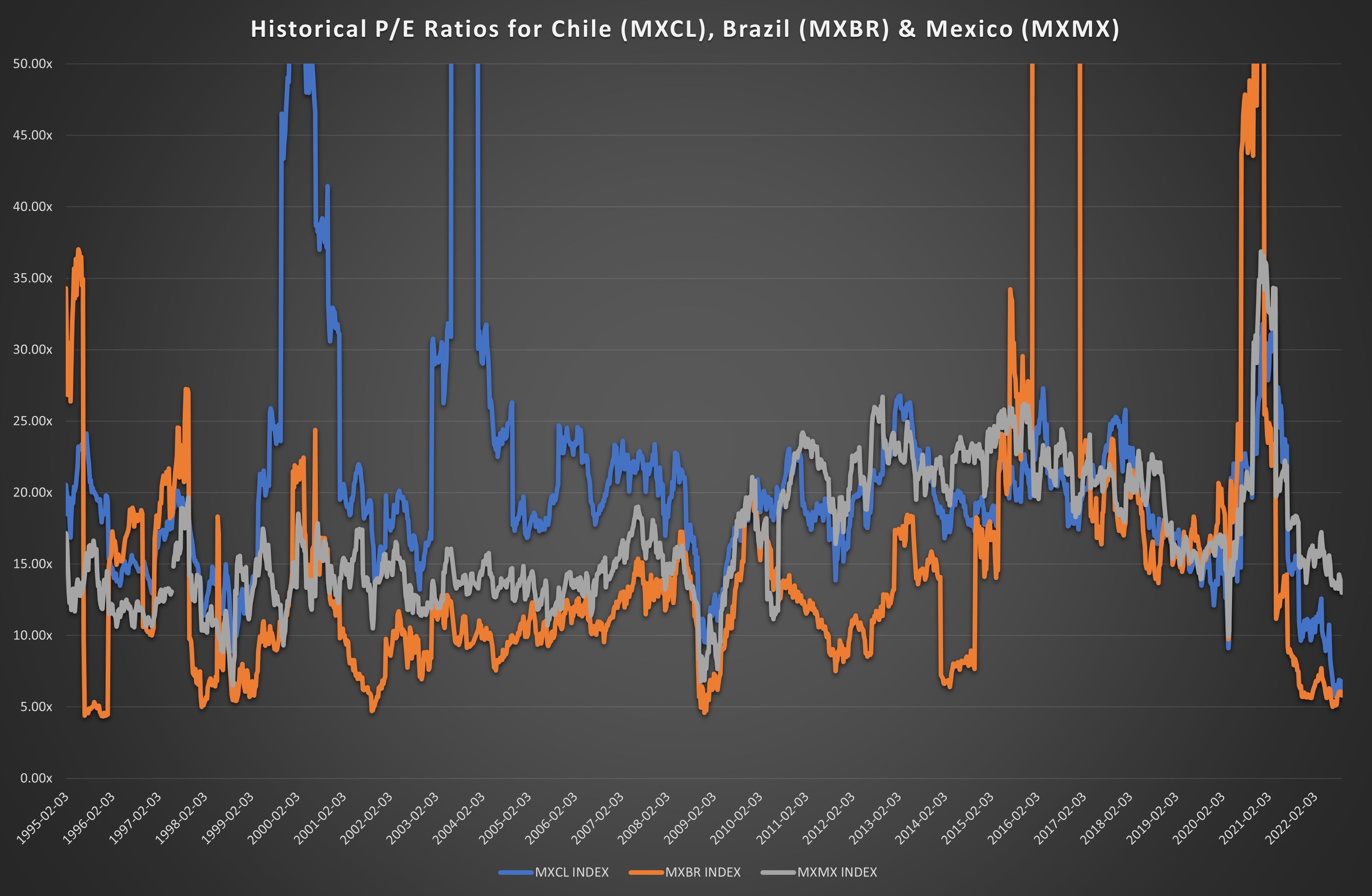

And this has very real implications for markets and asset valuations. Here is the historical P/E ratios for Chile (blue line), Brazil (orange line), and Mexico (grey line):

Chile and Brazil indices are at ~6x earnings and are close to 30-year lows. Meanwhile, Mexico which has been more stable both economically and politically in spite of the horrific cartel war (that is still ongoing) trades at a very modest 3-turn discount (currently 13x vs historical 16x P/E).

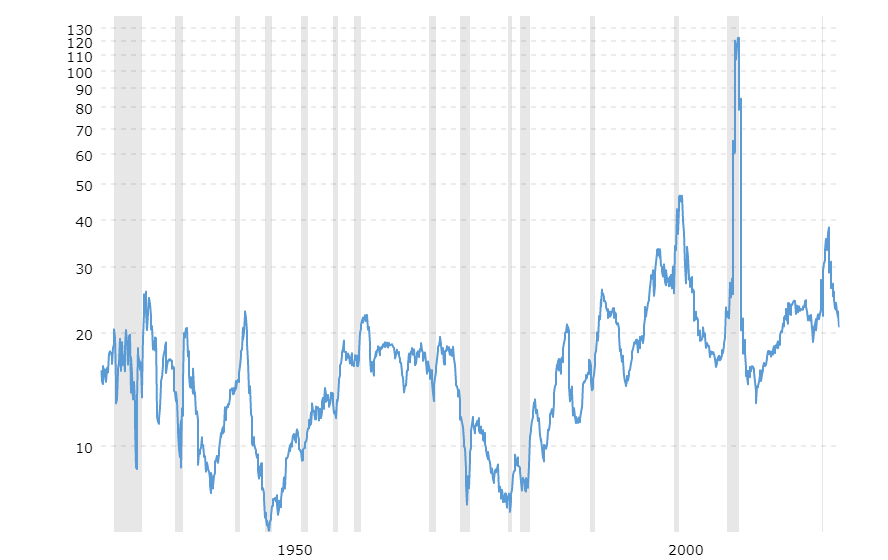

And this isn’t just an “emerging markets” phenomenon either. The late 60s and 70s were a particularly tumultuous time of rising cost of living along with social and political upheaval. US markets bottomed in the early 80s at around ~7x earnings:

So here are my big takeaways.

First, just because something’s “cheap” doesn’t mean it’s going to mean-revert higher on its own. I know this is heresy to most value investors. But history and personal experience would say that just because something is “cheap” doesn’t mean it can’t get “cheaper”. You need some kind of positive catalyst(s) to cause investors to rerate markets (or companies) higher.

I bring this up because I’m seeing a lot of recommendations to buy European equities simply because they’re “cheap”. Right now Europe is suffering from a severe energy crisis, but it is already morphing into a political and social crisis that will likely worsen over the winter.

Germany’s DAX is trading at ~10x earnings, but what’s stopping it from trading at 6x or 7x (plus a massive drop in earnings due to the energy crisis)? If DAXX rerates to 7x earnings and earnings fall 50% due to exorbitant energy prices, you're looking at a ~60% decline from here, regardless of how “cheap” it is.

Most European politicians and bureaucrats are busying themselves with this “Russian oil price cap” scheme that will never work and doubling down on failed energy policies. On top of that, Europe still suffers from terrible demographics and is resource-poor just as we enter the 2nd part of the commodity supercycle (i.e. when commodity prices go up).

There have been some catalysts such as the UK and France promising to expand nuclear power, but this will take a decade to bear fruit. Most of Europe seems to be in the “hope and pray” camp.

The only near-term catalyst that I’ve come across is in the UK. It appears that likely next Prime Minister will expedite onshore and offshore drilling permits to try and ramp up production by winter’s time. Environmentalists are already bemoaning the “backsliding”, but these people are out of touch and completely naive. Large-scale blackouts and the inability for people to stay warm will be far worse for the environment long-term than any of them will ever appreciate or acknowledge.

The political and social upheaval that is coming if this winter bad couple be really, really ugly. Oh and by the way, the massive volcano eruption in Tonga this January may very well mean a very cold winter across the winter hemisphere (even as an energy investor, I really hope this isn’t the outcome for all of our sakes).

On the flip side, LATAM has been through this over the last five years. I haven’t seen any significant catalysts to get excited about but there are a couple of big upcoming and promising events to watch.

First, there’s Chiles's constitutional referendum vote which will happen this weekend (September 4th). While the majority of Chileans (78%) want a new constitution to replace the one written during Pinochet’s dictatorship.

However, the leftist went too far when drafting their proposed constitution as the constitution they’ve created is simply too extreme for most Chileans. The ask was too big. Current polling has the “reject” vote leading by about 10% but there’s a huge group of undecided (around 15%).

Chilean markets have already rallied off the lows and are about to make new highs for the year. If the new constitution is voted down, markets probably keep ripping higher. Even though we’d have missed the initial part of the rally, there’s still plenty of “meat left on the bone”.

Meanwhile in Brazil, there’s the Presidential election which so far has surprised everyone. It’s current President Bolsanora against the previous President Lula (who had been in jail for corruption until the Brazil Supreme Court nullified his conviction and freed him).

Most watchers were very nervous going into this election but then things took a weird turn. Lula, a lifelong left-wing politician was reported to have met with Brazil’s business elite multiple times and while he’s promised labor market reforms and higher minimum, he’s also promised greater financial discipline and transparency while seeking guidance from Brazil’s business elite.

Then an even bigger shock landed. President Bolsonaro, who fashioned himself to that of Donald Trump, did an extreme about-face and promised to honor the results of the election should he lose. This abrupt pivot to the center for a politician that caught everyone off guard.

Of course, both politicians are just saying things that will make people happy (aka lying) and that’s entirely possible. But an alternative (and my belief) is that successful politicians often know which way the winds of popularity are blowing and pivot there (or at least attempt).

The election will be held on October 2nd so we have some time to wait and see how things play out from here. But a calm and no-drama election would be a real positive catalyst for the entire region.

Investment / Trade Idea

Things seem to be turning around in at least some parts of LATAM and perhaps brighter times lay ahead. Bullish LATAM, a true widowmaker trade I know. We’re also entering the part of the commodity supercycle where commodity prices are going to go up. The last decade saw a massive commodity bust and under-investment meaning supply likely won’t be able to keep up with demand globally.

This is more bad news for Europe which is resource-poor but good news for LATAM as a rising tide often lifts all boats. Finally, Europe’s demographics are dreadful and while LATAM’s demographics aren’t great, they’re definitely a lot better.

Next week I’ll cover a couple of companies that I’ve put tiny starter positions on (I couldn’t help myself and jumped the gun) but wanted to put together at least one actionable trade/investment idea so here it is:

Long a basket of LATAM - iShares Brazil (EWZ), iShares Mexico (EWW), and iShares Chile ETF (ECH).

Short a basket of European indices - DAX German ETF (DAX), iShares MSCI Italy (EWI), and iShares MSCI Austria ETF (EWO)

The reason I choose these European indices is because I wanted to avoid broad Eurozone ETFs which are largely dominated by UK, Dutch & Swiss multinationals that operate in the energy, mining, consumer staples, and pharmaceuticals industries and therefore less likely to be impacted.

As for the time frame, I’m not sure. These kinds of big moves often seem to take 5 to 7 years year to play out so it’s definitely not a short-term trade.

I don’t have the trade on yet and may not put it on so I’m thinking about how to keep track of this recommendation. Right now I’m leaning towards going the “academic” route and just keeping track of the NAVs and tallying the performance periodically.

Currently, the NAVs are the following:

iShares Brazil (EWZ): $30.46

iShares Mexico (EWW): $44.59

iShares Chile (ECH): $27.37

DAX Germany ETF (DAX): $21.79

iShares Italy (EWI): $22.95

iSHares Austria (EWO): $16.84