Macro Thoughts - It's Getting Scary Out There

Hi everyone,

I have some macro thoughts that on the surface won’t seem all that connected. But bear with me to the end as I try to put them all together. Right now, they are all on the front page of the news, but there seems to be little discussion of the long-term fallout and repercussions. What we’re seeing in various forms is a massive failure of politicians, bureaucrats, and regulators to craft sensible policies and enforce them. The ramifications of this I’ll dive into below.

Pump’n’dumps go mainstream

In a typical summer, markets go very quiet as liquidity dries up and people take off on holidays. This summer has been anything but quiet. More shocking even is the number of large pump’n’dumps that have occurred in the last couple of weeks. We aren’t talking about small pump’n’dumps of microcrap mining or biotech stocks either.

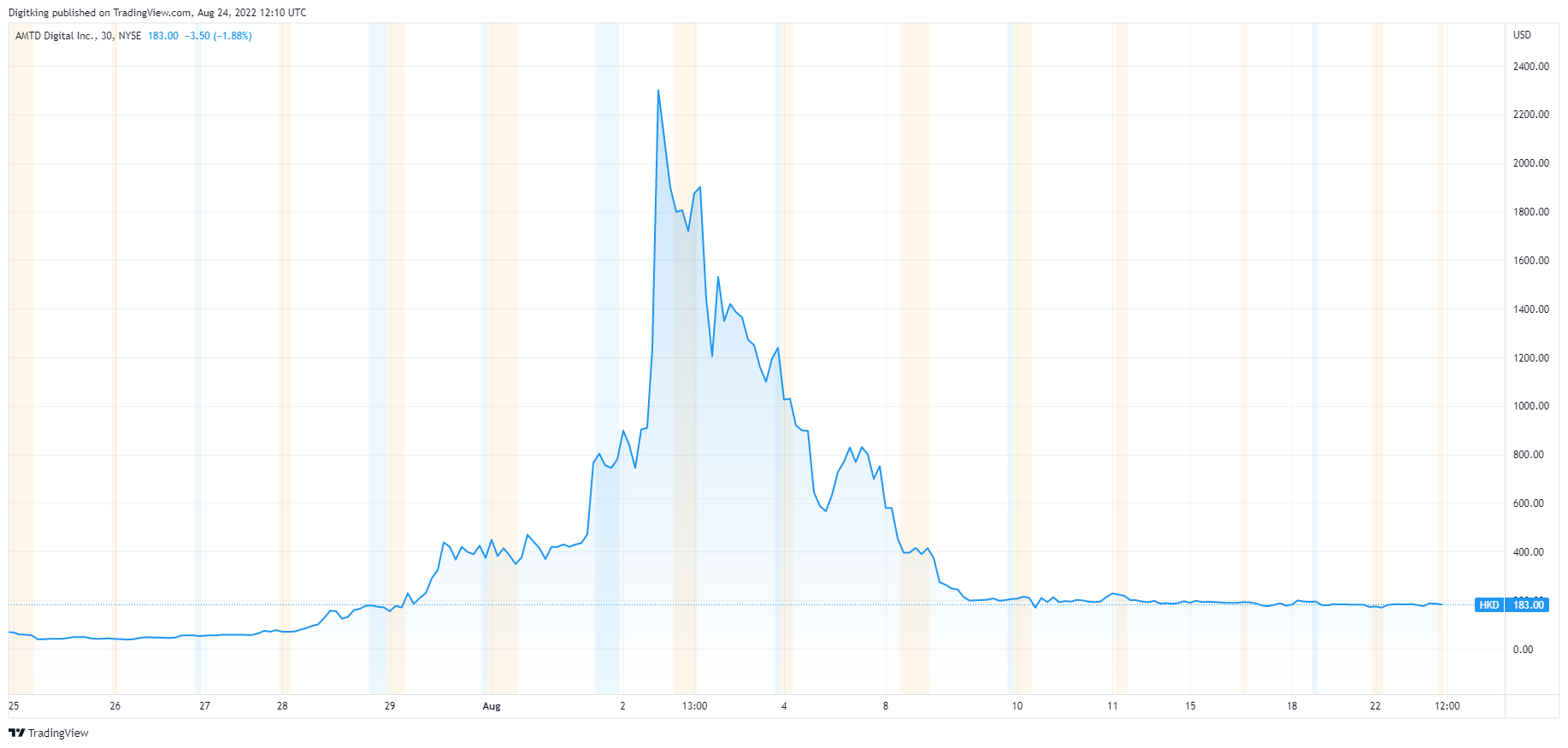

Take for instance HKD or AMTD Digital ADR. A “company” with barely any revenue and issued by an underwriter with a long history of fraud and other financial shenanigans. At its peak, its “market cap” was over $500 billion and would have put it in the top 10 globally. Even now, it still sports a “market cap” of more than $30 billion dollars.

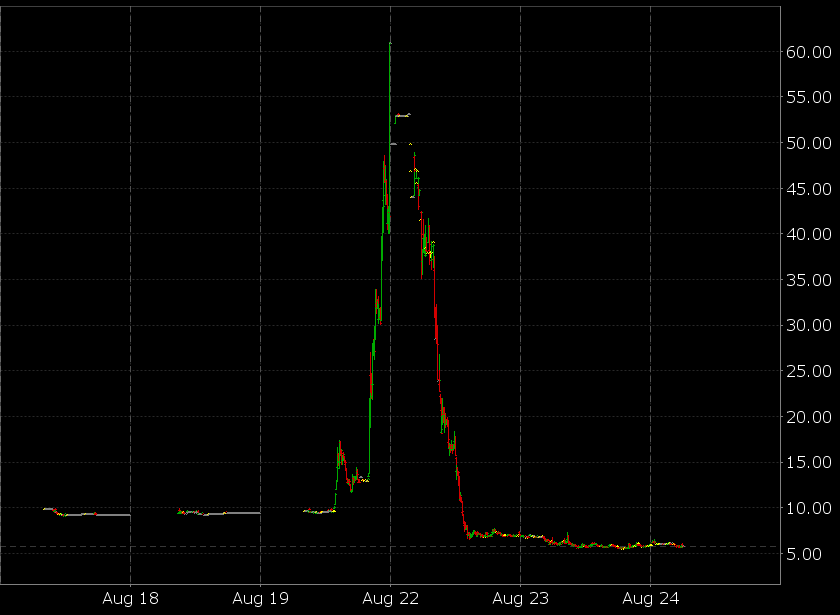

But there have been many more pump’n’dumps just in the last couple of weeks! We also have Chamath’s latest SPAC, which had the trading symbol of DNAA until the deal closed and was changed to AKLI:

The deal was announced on Friday and the stock was up ~50% during the day. It went up another ~220% in Friday AH trading and another ~30% in the premarket on Monday. From its peak on Monday morning in the premarket, the stock has declined by almost 90%!

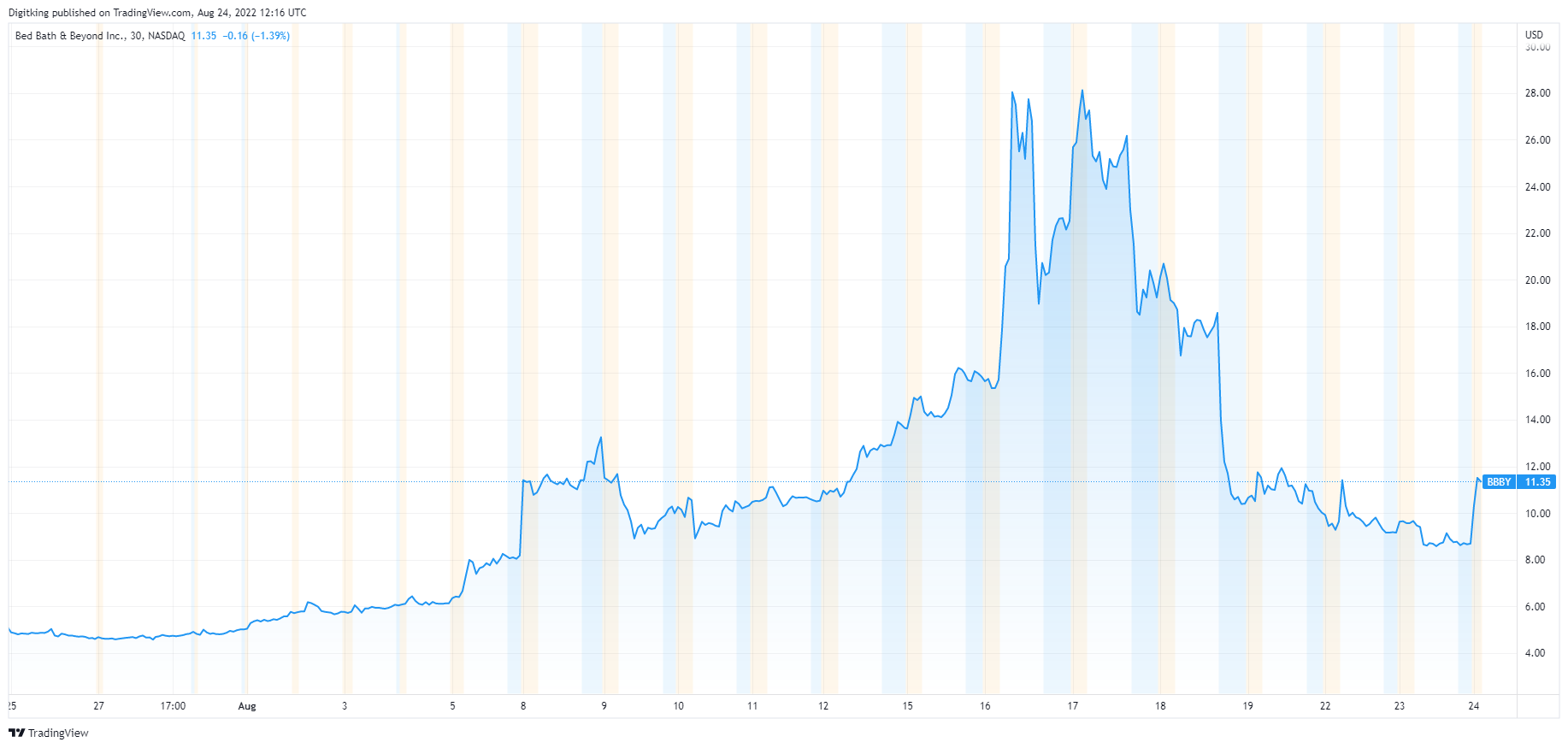

Then there’s of course the entire Bed, Bath & Beyond saga.

Let’s ignore all the legal issues of Ryan Cohen, the Board of Directors, and management who likely sold shares while in possession of material non-public information; and just focus on the trading. The stock, which was one of the meme stocks from last year went up almost 8x in the space of a month even as business fundamentals deteriorated.

The common refrain is that this is mostly just retail or Reddit’s WallStreetsBet crowd pushing a couple of “meme stonks” around but I don’t think so. As Tom Hearden pointed out in the BBBY case:

And this seems to be a fairly consistent issue across all of these pump’n’dumps (and others that I haven’t touched on). An awful lot of trading in premarket and aftermarket hours, which is a time that most retail traders do not have access to.

Who’s doing all these trades in these failing/borderline bankrupt companies? I have no idea but it’s not likely to be retail (at least initially).

Why are they doing this? It seems pretty obvious that someone (or many) is trying to “paint the tape” to bait retail and other momentum traders into these names.

Is it legal? I’m not a legal expert but I was told long ago that market manipulation is illegal. It also crushes the claim that the markets are a “serious place where capital is allocated efficiently”.

Where are the regulators (aka SEC & CFTC)? I have no idea. Even worse, they don’t seem to have learned anything from last year’s “Meme Stonk” frenzy!

Things Not Looking So Hot in Europe

Meanwhile, in Europe, the energy crisis continues to worsen. Bloomberg’s Javier Blas has done a fantastic job warning of this looming disaster and covering it as it unfolds:

The obvious reason is that natural gas prices (using the Dutch TTF) have skyrocketed:

The less obvious reason are numerous though. Europe decided to transition to “green technology” far too soon with completely untested technology that hasn’t even come close to living up to expectations. Simply put, the battery technology that would switch wind & solar from intermittent to baseload is still a decade or more away.

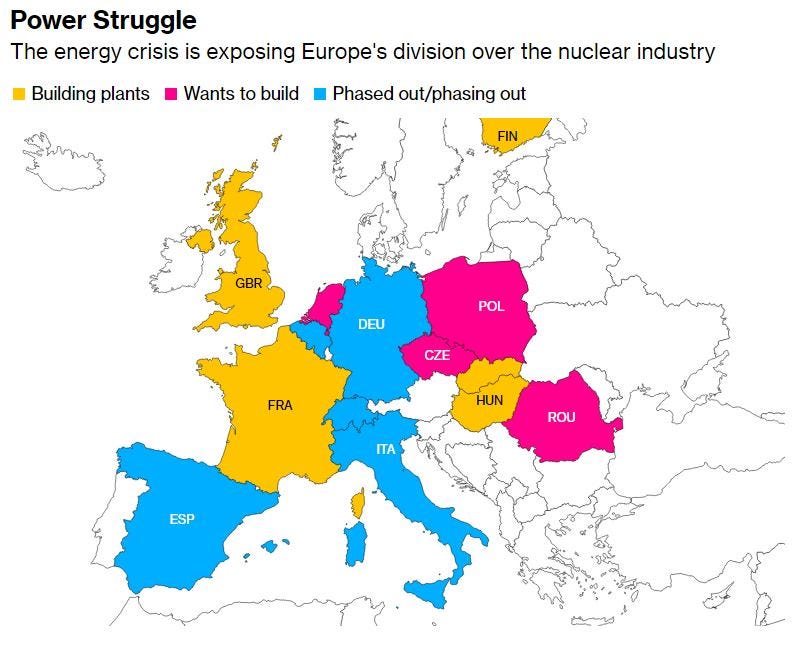

Most of Europe (not just Germany) has also phased out or is in the process of phasing out its existing nuclear power from Bloomberg:

Meanwhile they also dramatically reduced their own natural gas production (mostly from the North Sea) while banning onshore oil and gas shale fracking. You would think an impending economic collapse would motivate some real soul-searching, and yet here we are:

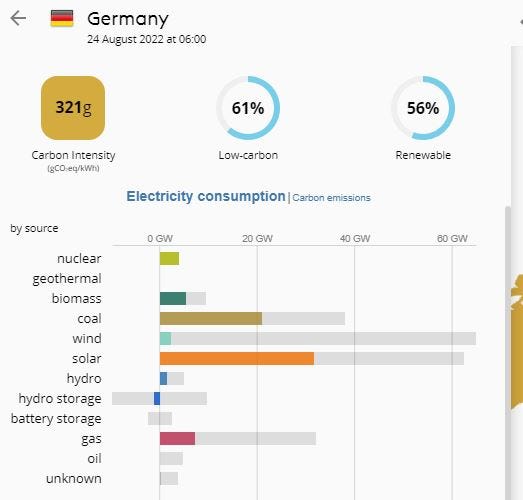

What is the result of all of this? Well take a look at Germany’s live electricity grid:

It’s just another normal day with wind working at ~3.5% of installed capacity while solar is having a relatively good day at ~50% of installed capacity. Meanwhile, the little bit of nuclear power that is left is operating at ~98% installed capacity, and yet per the latest remarks from Germany’s Economic Minister, it will still be shut down at year-end.

Of course, there are many more examples of the silliness and unseriousness of European energy policy. This one, in regards to the EU’s Carbon Pricing Plan (which is still in the draft state), takes the cake though:

China Lurches From One Disaster to Another

Meanwhile, things seem to keep getting worse in China. China’s Zero Covid policy continues to be an epic failure, with China now locking down many of its most popular vacation resorts as well as large chunks of Western China.

Of course, Zero Covid could be relegated to the dustbin and solved by President Xi admitting that the China vaccine (Sinovac) doesn’t work. And then contracting with one (or all) of the Western vaccine producers for supplies of a Western vaccine that does work. But that would mean Xi falling on his sword (and losing face) while also destroying the nationalist fervor that he has created.

I’ve discussed this issue before, but between the “Zero Covid” policy and the constant saber-rattling over Taiwan, manufacturers are leaving outright, diverting new investments elsewhere (US, India, etc.), or making backup plans. For instance, Apple which is probably the most important manufacturer given its visibility (via Foxconn) in China, announced that the iPhone 14 will be manufactured in India two months after its release in China, the smallest gap in its company history. Even a blind squirrel like me can see where this is going, Apple will continue to shift ever more of its production out of China, and it’s likely never to come back.

Meanwhile, Xi’s “Three Red Lines” plan to reign in speculation in the real estate sector has already failed spectacularly. Chinese real estate is on paper, the largest asset class in the world. It represents 70% of household wealth and represents over 20% of the country’s GDP. Any sensible effort to deflate this bubble should have been done with extreme care and done over a five to ten-year period. Instead, it brought the entire real estate industry into a crisis in less than a year.

Allowing large real estate developers to fail also had some interesting knock-on effects. I didn’t know this until the “mortgage boycott” made the news. But in China, you have to pay upfront and in full before the development is even started!

So what happened? Chinese investors and would-be homeowners who gave all of their savings and took out a mortgage to buy a home saw that their home/condo/etc would never be built (or completed). So they did what any rational person would do and stopped paying their mortgage!

At first, the CCP tried to scold and threaten these delinquent borrowers. But once that didn’t work, the realization dawned that this boycott could turn a real estate crisis into a banking crisis very quickly and so they began to pivot.

Now the regulators and bureaucrats are scrambling to force the banks and (insolvent) real estate developers to find a solution to completing the projects that the Chinese people have already paid for. It remains to be determined if this will work.

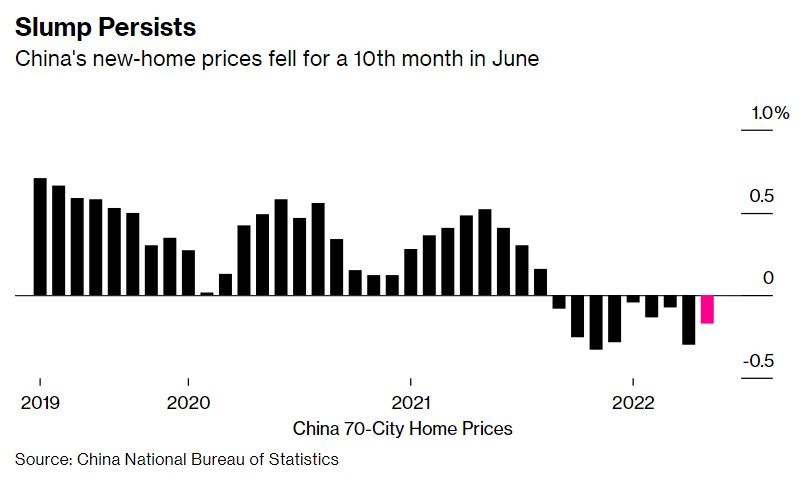

The fallout of all of this is already started to bubble up. Housing is already rolling over:

An entire generation of Chinese homeowners and investors only know one thing, and that’s that real estate prices increase (sounds familiar to Canadians). But there are even bigger problems now than real estate.

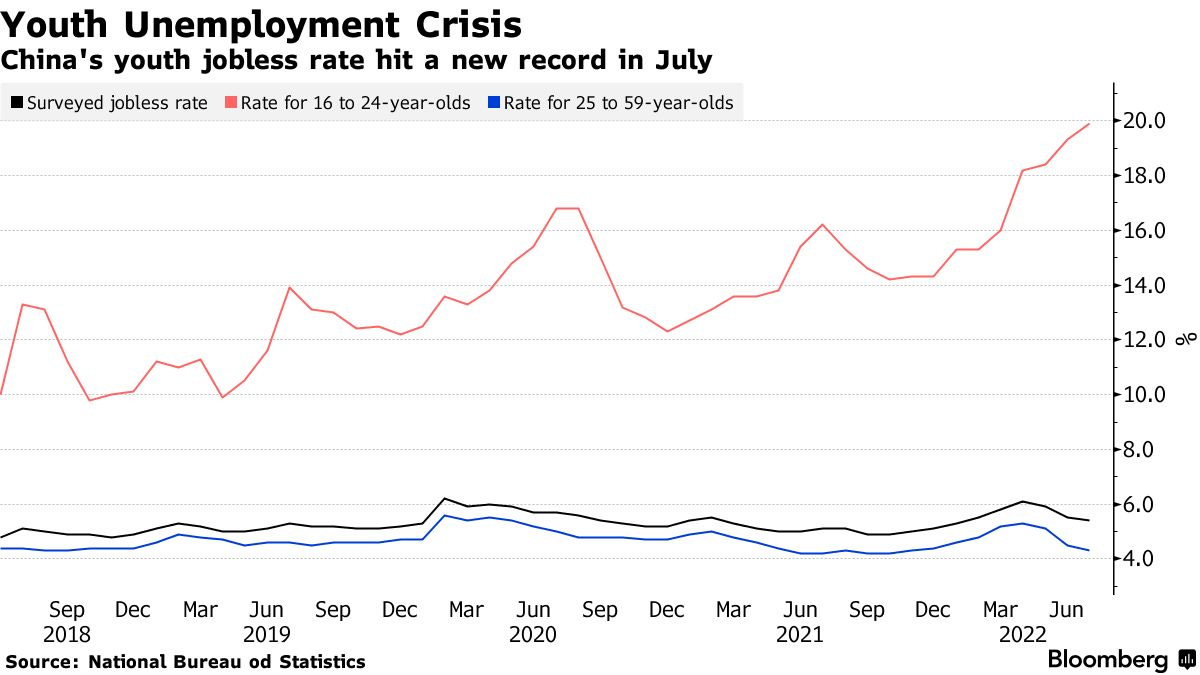

Youth unemployment just hit a record high.

So what’s your point?

I’ve highlighted just three instances of really bad crafting and enforcing of policies by politicians, bureaucrats, and regulators (and don’t even get me started on Canada).

I fear if this continues, the risk of a left-tail event (i.e. something bad) will continue to rise. And at some point, the markets will care. Or as Mark Twain once said: “Slowly at first, then all at once”. We are now venturing into the world of known unknowns (or is it unknown unknowns?).

Maybe the continued transformation of American capital markets into a lawless gambling den further galvanizes extreme politicians (both on the left and right) as proof of institutional failure. We bemoan how bad partisanship is now, but what if it gets worse?

In Europe, the situation is much, much more dire. If this winter is very bad (i.e. longer and colder than normal), could we see the dissolution of the entire EU project? It seemed unfathomable even 6 months again (<0.01% chance), but now? What kind of odds would you place if many European countries see a 10-15% drop in GDP (which would be on par with the 1930s Great Depression)? Is 5% odds too high or too low? What about 10%?

China is also facing enormous pressures, even though it’s outwardly claiming everything is fine. There has been a lot of discussion of China invading Taiwan, both to “reclaim its lost province” (albeit highly dubious) but also as a distraction from its ever-growing internal problems.

But what if it’s not an invasion? But instead a civil war or the collapse of the CCP? This seems crazy but just a decade ago, a lone fruit seller set himself on fire in Tunisia and kicked off the Arab Spring. Half a dozen dictatorships throughout the Arab collapsed and three brutal and bloody civil wars (Libya, Syria, and Yemen) are still being fought to this day.

I can already hear you say, “but that’s silly, the CCP will never collapse and they have total control over the Chinese people”. It sure seems like it! And while I’m no expert on China, I am a fan of history and would like to point out that the CCP itself rose to power from a civil war due to the failings of the previous government.

And China has a long history of internal conflict. Here is a list of historical (pre-1900s) civil wars and infighting, some of which lasted decades and even centuries (from Wikipedia):

Chen Sheng rebellion

Agrarian revolts during Wang Mang's reign

Divisions of Fanzhen

Li Zicheng revolt

Zhang Xianzhong rebellion

So the possibility of something really bad is still low (probably less than <1%) but it’s not zero, and that probability will likely continue to rise unless things change/improve. At the same time, it’s important to point out that dictatorships, especially totalitarian dictatorships such that Xi has created are inherently less stable and more prone to dramatic collapses (than say a democracy) given that there are no release valves.

But even if things don’t get really bad, what happens if there’s another Tiananmen Square massacre? What does something like that mean to the global economy and markets?

And the problems aren’t just limited to the US, Europe, and China. For instance, Europe is buying up every LNG shipment it can find. It’s on pace to hit its targets of reaching 90% storage by winter (storage would only make up about 1/3 of its winter needs but that’s another story).

The downside of this buying spree is that global LNG prices are soaring and poor countries have been completely priced out.

Take Pakistan for instance, it switched a big chunk of its power generation to natural gas over the last decade because LNG was cheap (and coal was dirty). Now, they can no longer afford to pay for the gas so they’re suffering with rolling 12 - 16 hour blackouts and mass protests each day. They also have nuclear weapons and aren’t in the most stable part of the world (to put it politely).

The rest of the developing world is struggling just as badly. Sri Lanka has already collapsed due to horrifically bad policy decisions made by the government (with the encouragement and backing of many in the West). Protests and riots are occurring all across Africa, South East Asia, and South America due to the high cost of oil, gas, and basic foodstuffs.

What Can I (and We) Do?

This is the hardest part though. Hedging extreme tail risks like the EU disintegrating or civil strife in China is really, really hard. I’m sure the Gold Bugs and Bitcoin Maximalists have a solution, but their solution is the same for every situation…

Tail risk hedging is another option and Benn Eifert over at QVR Advisors has a great high-level piece in the Q1 2022 called Common Hedging Discussions Part 2: Tail Hedging Return Myth Debunked. But this is new ground for me that I need to study more.

I remember how some hedge funds were made famous from the GFC and “The Big Short”. But nobody remembers any of the dozens of other hedge funds and investors that also bet against US housing, but they were just too early and ran out of capital.

Another issue with tail risk hedging that I need to investigate is that some of these events would be so big if they occurred, would your hedges even pay off? For instance, if the EU dissolves in an ugly manner, what exactly would be a good tail hedge? It’s such a momentous event that just the primary impacts, let alone secondary and tertiary impacts would be enormous.

A third option is just to increase cash and defensive positioning. However, as gloomy as this whole article has been, I’m still overall bullish on risk assets. It’s just that the distribution of returns is (in my opinion) changing.

My base case is that risk asset markets are still the place to be. Value stocks (energy, mining, financials) are likely to generate positive returns over the next 12 to 24 months. There will be more volatility, as days like today prove, but overall I think the trend is up (unless you own profitless “growth stonks”). It’s just that the tails are getting fatter, and if there is a downside it will be worse.

The last option is just vigilance and keeping an eye on the exit. Covid is a perfect example of this because it was spreading and looked severe. But the markets didn’t really seem to care until they were forced to care. And once the markets cared, the whole market got flushed out very quickly.

As John Tuld, the fictional character in Margin Call said:

“There are three ways to make a living in this business: be first, be smarter, or cheat”.

Now I’m never going to outsmart the markets. And I’m also never going to cheat. This leaves me with one option, to use my small size to get out when things look to be going south.

Right now, this seems like the best option while I continue to explore tail hedging possibilities. Next week, I’m going to cover a region that has seen lots of “left tail” events and why maybe it’s finally turning a corner (famous last words).