Company Highlight - Green Brick Partners

Hi everyone,

I’m still working out what to write once a week and I think I’ve settled on the following four categories going forward:

Sleepy Canadian Portfolio

Macro Thoughts

Trade Ideas

Company highlights

I’ve already written about the first three so there’s not much more to say. The latest is company highlights; which are not meant to be in-depth research pieces but more so to connect my macro thoughts to individual stocks at a high level.

I’ve been working on this article for Green Brick for most of the last week and unfortunately, it’s not particularly timely as the stock is up almost 50% recently.

The stock jumped two weeks ago on news that it would be included in the S&P 600 small cap index and then continued to run after reporting earnings on Wednesday evening where they completely crushed expectations.

However, zooming out a little bit, the stock is still below its recent highs from December 2021 and a long way down from its pre-GFC price levels (although it’s admittedly a very different company and unlikely to get get back to $200+/share).

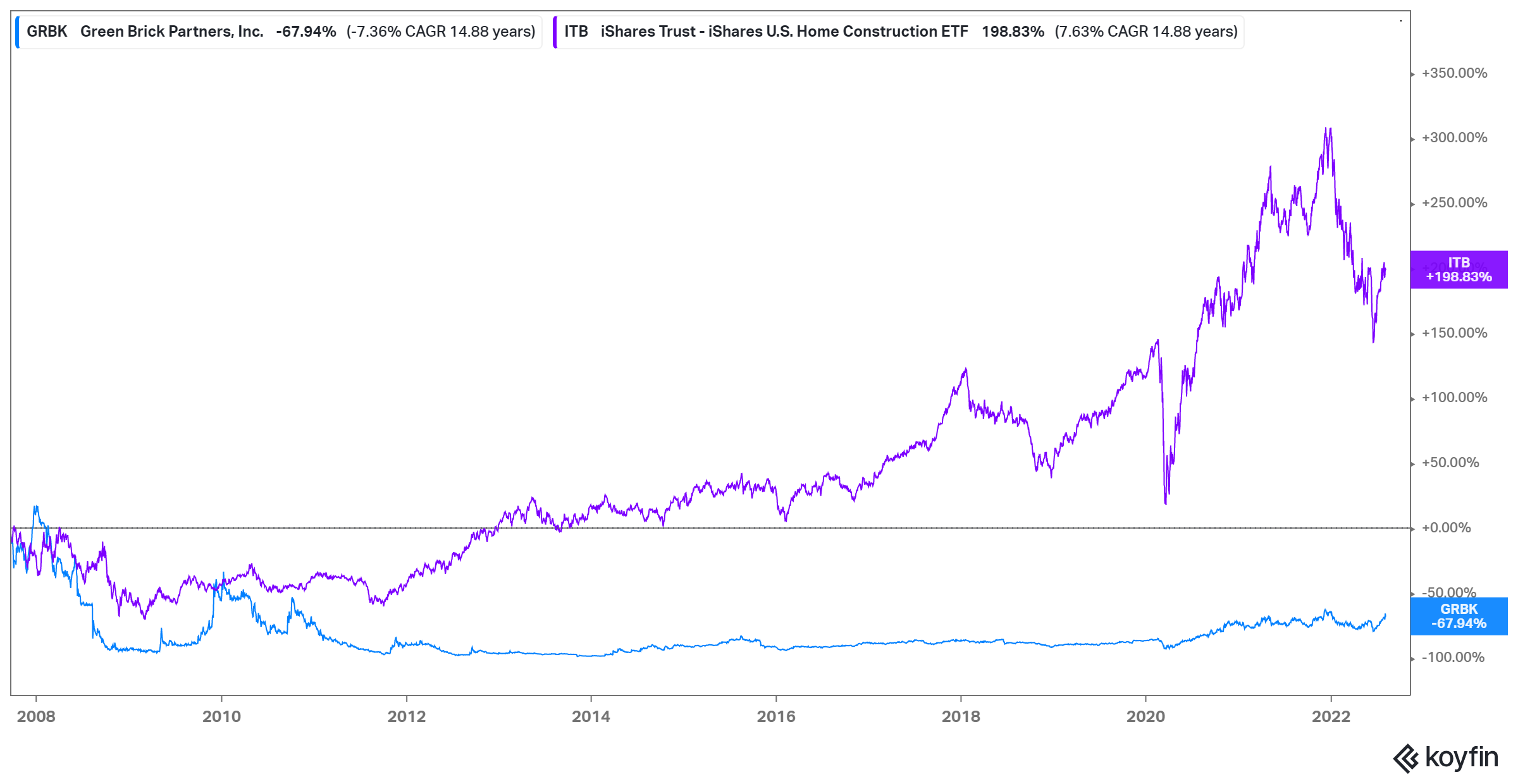

Here are the 10-year returns:

And here are the returns since pre-GFC to show that most of the gains on GRBK are just off a very low base. Amazing how much a chart can change when you just adjust the timeframe!

My recommendation would be to keep the name on your screens and wait for a pullback. But now, let’s dive into the company.

What is Green Brick Partners?

Green Brick Partners is a small cap US homebuilder that focuses on Colorado, Texas, Georgia, and Florida. I came across this stock a while ago while reading David Einhorn’s quarterly Greenlight Capital letters (more on that later).

The reason that I find this company intriguing is tied to what I wrote about two weeks ago, where a resurgence in US manufacturing will lead to a boom for US workers.

Since publishing that article, there’s been additional news that gives the story more traction. The WSJ reported that the new fiscal stimulus bill would include requirements on sourcing of both input materials as well as manufacturing them for electric vehicles:

But the biggest change is that the credit going forward will be contingent on where its battery materials are made. To qualify for $3,750 of the credit, an increasing share of a vehicle’s battery minerals such as lithium and nickel must be extracted or processed in the U.S. or in a country with which the U.S. has a free-trade agreement, starting at 40% in 2023 and increasing to 80% in 2027.

The other half of the credit will only be available for vehicles in which a majority of its battery components are made in North America, starting at 50% in 2023 and growing to 100% by 2029. Yet about 80% to 90% of battery components now are made in China, which also refines 68% of the world’s nickel, 73% of cobalt, 93% of manganese and 100% of the graphite in EV batteries.

Currently, the US has free trade agreements with 20 countries, but none of them other than maybe Canada and Mexico have the size and/or infrastructure to compete so it’s likely that much of the manufacturing will be done in the US. And within the US, most of the new manufacturing facilities are being developed in the southern US where costs are lower, regulations less stringent, and access to cheap and plentiful energy and natural gas.

On top of that, the US underbuilt housing by the tune of ~5.5 million homes during the 2010s due to the fallout of the Global Financial Crisis.

How does Greenbrick fit into all of this? Because as the famous saying goes, “all real estate is local”. While there is a lot of doom and gloom for the US housing market due to higher rates. Rising interest rates have very different implications for different regions of the country. A 5% 30-year mortgage rate has very different implications for high costs areas of the country than for lost costs areas.

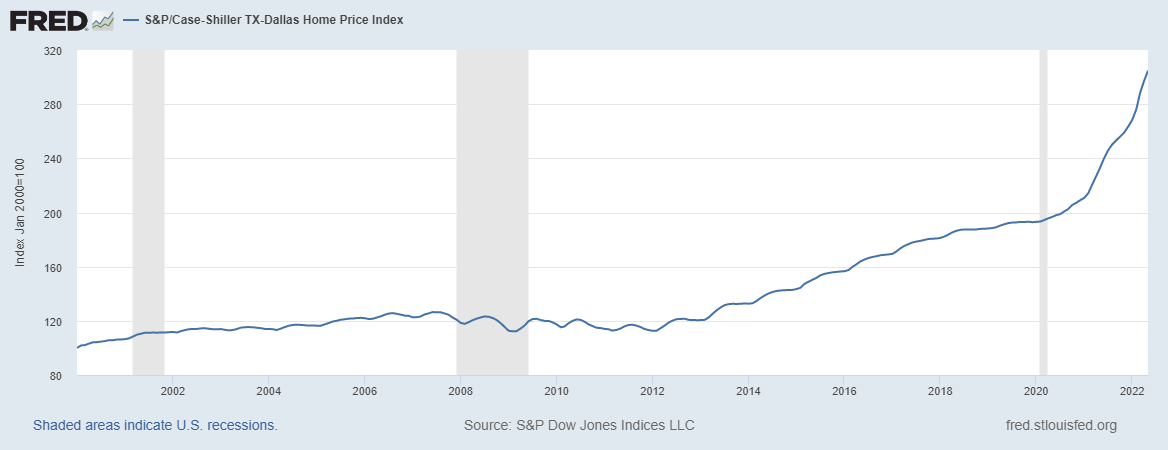

Homes prices have skyrocketed in lower costs areas like Dallas and that makes the charts like this look quite scary:

It’s worth keeping in mind that it’s starting from a relatively low base. When you compare with higher costs areas, the increase is hardly noticeable:

But as Harley Bassman succinctly put it, “people don’t buy houses, they buy a stream of mortgage payments”. So if we compare the various major metro markets, we can see why the rate hikes are less significant for where Green Brick operates.

This is just a hypothetical comparison assuming a 5% downpayment, this is what the monthly payments would look like in the cities that Green Brick operates in versus the large high-cost metropolitan areas. I also haven’t adjusted for mortgage tax deductions or anything else either.

In this chart, I’ve highlighted in orange the cities that Green Brick operates in versus other major cities in white. Monthly mortgage payments have definitely risen, but they are still far below the coastal cities which have seen far bigger rises in dollar terms.

A fair pushback would be that the big cities like New York and San Fransico have higher incomes so they can support higher levels of mortgage payments. And yet, looking at the Census data, the income difference it’s that dramatic. But the amount of household income that has to be dedicated to mortgage payments is:

The calculation is admittedly a bit flawed because I’m using 2020 Census data and median incomes are probably up 10-15% since then. But nevertheless, it shows that the areas that GRBK operates in are still reasonably affordable and can bear the brunt of higher mortgage rates better than many of the large cities on the coasts.

It won’t be all roses and rainbows though, as the bottom end of the property market is definitely struggling. Management discussed this issue at length on their recent Q2 conference call. In short, people are downgrading to smaller homes to fit their budget.

From the CC transcript:

Bill Dezellem

Thanks. And then what are you seeing in terms of buyer behavior in terms of their requesting smaller homes or any other actions that buyers may be taking to make homes more affordable or reduce the price?

Jim Brickman

Well three months ago when we opened up communities, we were really surprised in that we had floor plans ran from 1850 to let's say 2200 square feet. And we weren't selling any 1800 square foot houses low interest rates. We're driving these people to buy a bigger house. And Jed aren't some of these people now for the first time converting to smaller houses.

Jed Dolson

Yes. We're seeing people by 1600 to 1800 square foot homes that nobody wanted really a year ago.

But this is more a return to a long-term trend than an end of the (real-estate) world. Low mortgage rates over the last five years allowed people to acquire larger homes. Now with higher mortgage rates (some might say return to historical levels), we’re seeing a return to the long-term trend for smaller/beginner homes.

But demand is still there, and with strong population growth and wage growth, it should be very supportive long-term for the areas that GRBK operates in.

But Wait, There’s More

GRBK is operating in 4 of the fastest-growing metropolitan areas of the United States and as I just demonstrated, they’re still relatively affordable. This effect has shown up in GRBK’s financials with much faster revenue and net income growth than their peers. At the same time, they’ve been consistently more profitable with higher margins whether you’re looking at Net Income Margin, Return on Equity, or Return on Assets.

This trend will likely continue at least for the foreseeable future and yet the shares on a valuation basis largely trade in line with their peers.

I think there are a couple of reasons for this disconnect:

Einhorn’s Greenlight owns ~35% of the shares outstanding and based on disclosures represents ~20% of their assets. Corporate insiders meanwhile own ~6% so the actual float is quite a bit smaller and that makes the shares less liquid. There’s also always the risk that if Greenlight could see significant redemptions that it could be a forced seller (although they’ve survived this value bear market so far so it seems unlikely).

The company is also aggressively buying back shares which is great for long-term investors but further reduces the liquidity of the company’s shares. As I’ve noted in my Canadian Sleepy Portfolio. It seems that since last November when central bankers around the world started to tighten; we have seen small caps and less liquid securities largely underperform both the market and their underlying fundamentals.

GRBK’s shares have held up relatively well (up 21% YTD vs -3% for XBI), but at the same time, I don’t think the company’s shares will get the recognition they deserve until central bankers finish tightening (both by raising interest rates and quantitative easing).

Wrapping it Up

Hopefully, this (relatively) short piece piqued everyone’s interest. It’s again not particularly timely given the recent run-up in share price. But I think it’s a fantastic little home builder operating in all of the right markets and worth keeping an eye on and to add on pullbacks.

Admittedly, the home building industry is very volatile and a P/E of ~5x probably overstates the valuation a bit given their (near-term) peak earnings. But even a 50% haircut to earnings would still work out to a ~10x P/E ratio.

This would still represent a ~50% discount to the S&P 500 (at 20x P/E) with better prospects in terms of revenue & earnings growth over the next 3 to 5 years. Eventually, investors will take another look at the industry and patient investors will be rewarded, it just may take a little while!

Disclosure: I am long and have a beneficial interest in all of the above-mentioned securities. I may change my holdings at any time post-publication.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.