Company Highlight - Grupo Aeroportuario del Centro Norte, S.A.B. de C.V. (OMAB)

Company Highlight - Grupo Aeroportuario del Centro Norte, S.A.B. de C.V. (OMAB)

*Note: all symbols are referencing the US-listed ADRs.

Hi everyone,

This is a name that I’ve had on my watchlist and have been meaning to write about this company for quite some time. Unfortunately, I was hoping that a pullback would come to time the publication but as we’ll see below, that hasn’t come to pass.

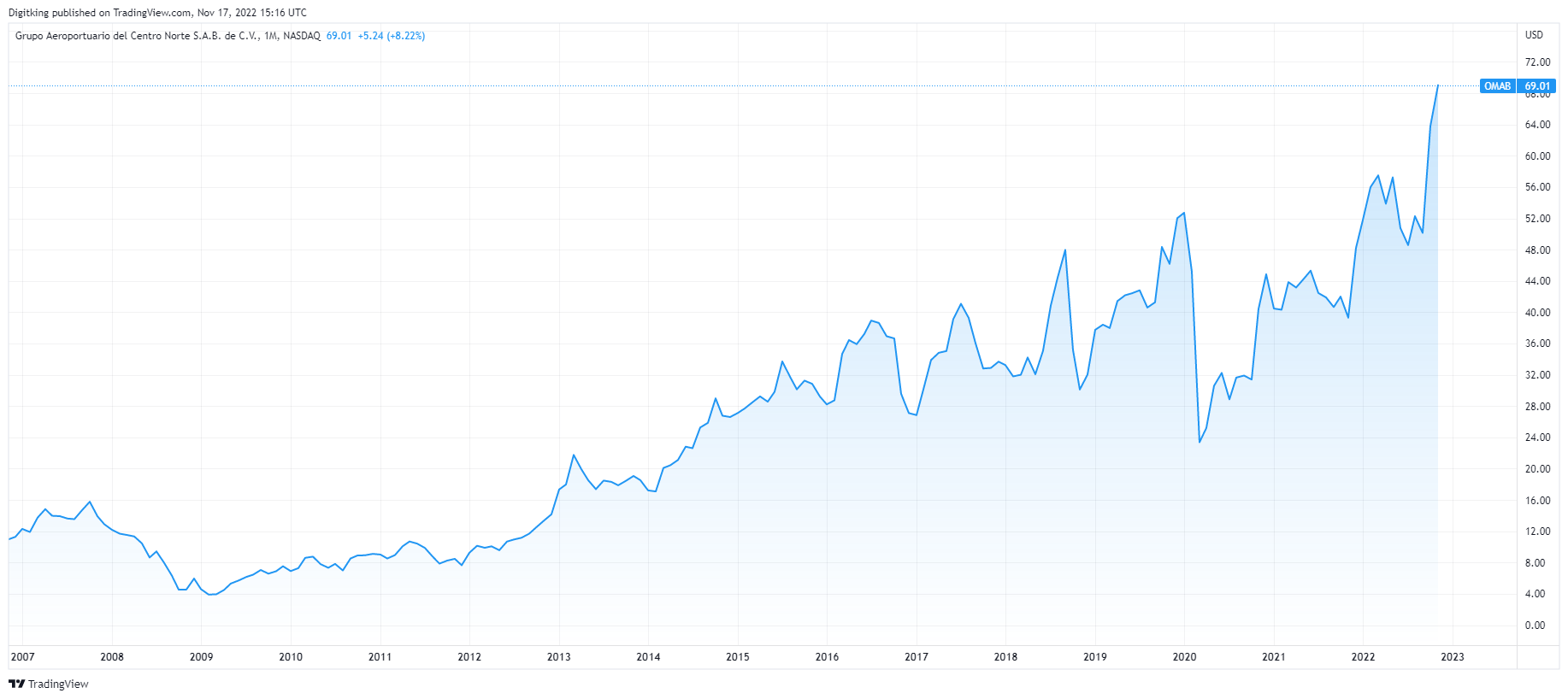

Grupo Aeroportuario del Centro Norte (from now on I’m just going to call it by its NASDAQ-listed symbol OMAB) has been in a serious uptrend (some might say parabolic).

Year to date, the stock is up just over 40%. Zooming out a little bit more, to five years, the chart looks pretty impressive as well.

So what exactly is OMAB?

It’s one of three publicly listed Mexican airports. The other two are Grupo Aeroportuario del Pacifico (PAC) and Grupo Aeroportuario del Sureste (ASR).

Why airports? And why Mexico? Well, back in July I wrote about the economic boom for American workers due to the reshoring of manufacturing and I thought that Mexico would also be a huge beneficiary in this process. I also wrote back in September about an economic boom in LATAM and highlighted Mexico along with Brazil and Chile as prime candidates to outperform over the long term.

I’ll dive into the numbers below, but if you believe that an economy will do well, then airports are a great way to get exposure. Unfortunately, there’s only a handful of publicly traded airports worldwide left. Most have been acquired by private equity as they’re one of the most prized infrastructure investments in the world.

Why OMAB over PAC or ASR?

Each airport operates in a different region (not surprising given the industry). OMAB is the smallest by market capitalization and is the most volatile.

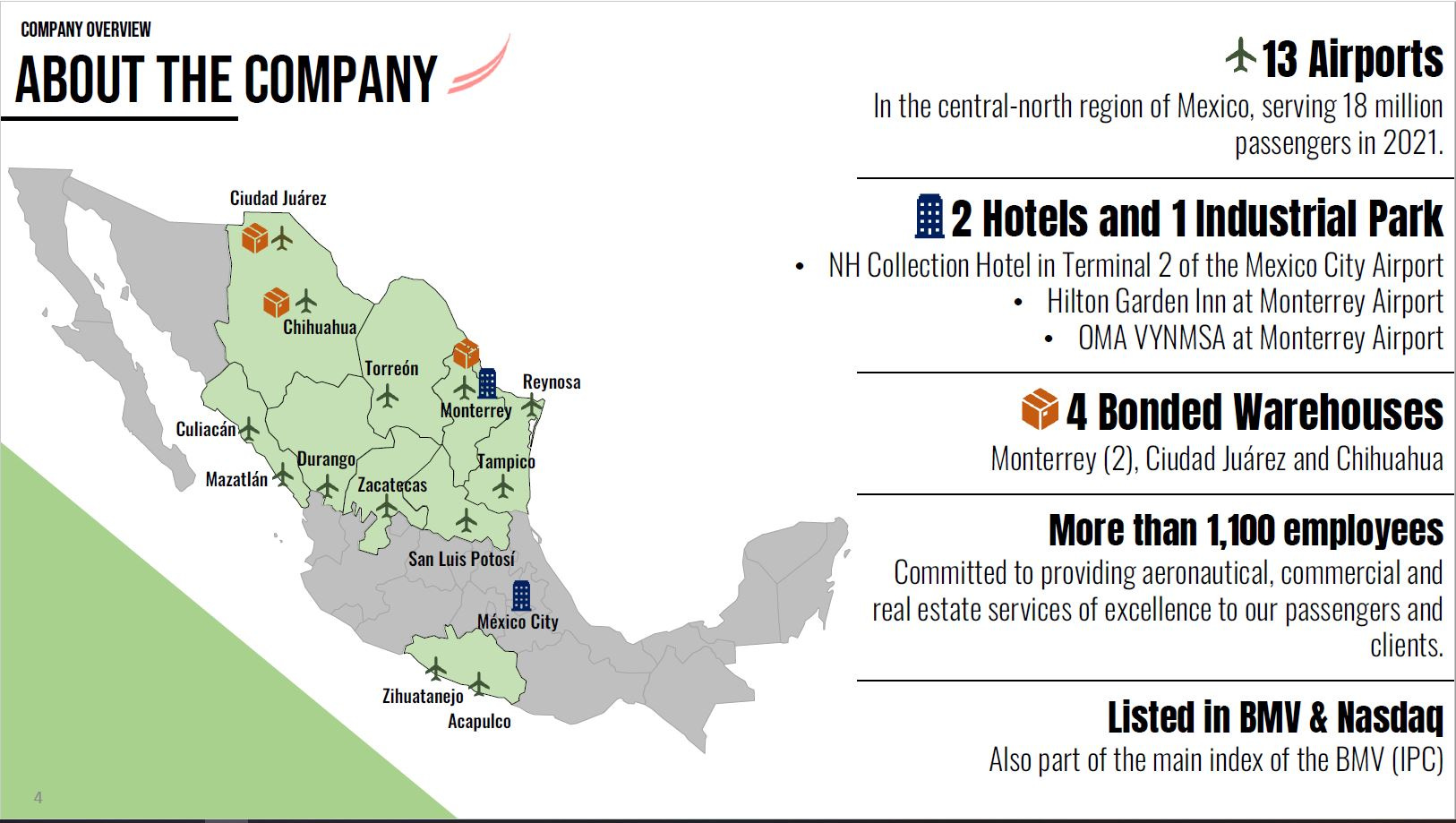

The company has concessions to operate and manage 13 airports plus additional services around the airports. The three most important are Cuidad Juarez, Chihuahua, and Monterrey (the largest and most important of all). All three are in northern Mexico. Northern Mexico is important for the investment thesis because it’s the country’s “industrial heartland” thanks to its close proximity to the United States border.

Grupo Aeroportuario del Pacifico (PAC) is the largest of the three (by market capitalization) and operates 12 airports. As its name suggests, its airports are spread out across Western Mexico (i.e. bordering the Pacific Ocean) with Los Cabos, Puerto Vallarta, and Guadalajara being its most important along two airports in Jamaica.

Lastly, there’s Grupo Aeroportuario del Sureste (ASR) which operates 9 airports throughout south & southeastern Mexico, including Veracruz and Cancun plus airports in Puerto Rico and Colombia.

So to sum it up, both PAC and ASR are larger than OMAB but have more exposure to tourism which is less geared to Mexican growth (but still a great way to get exposure).

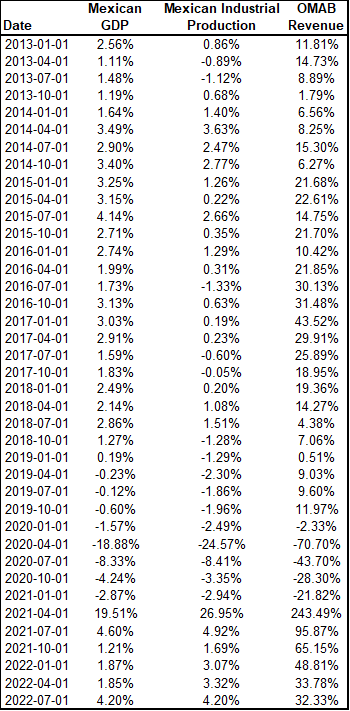

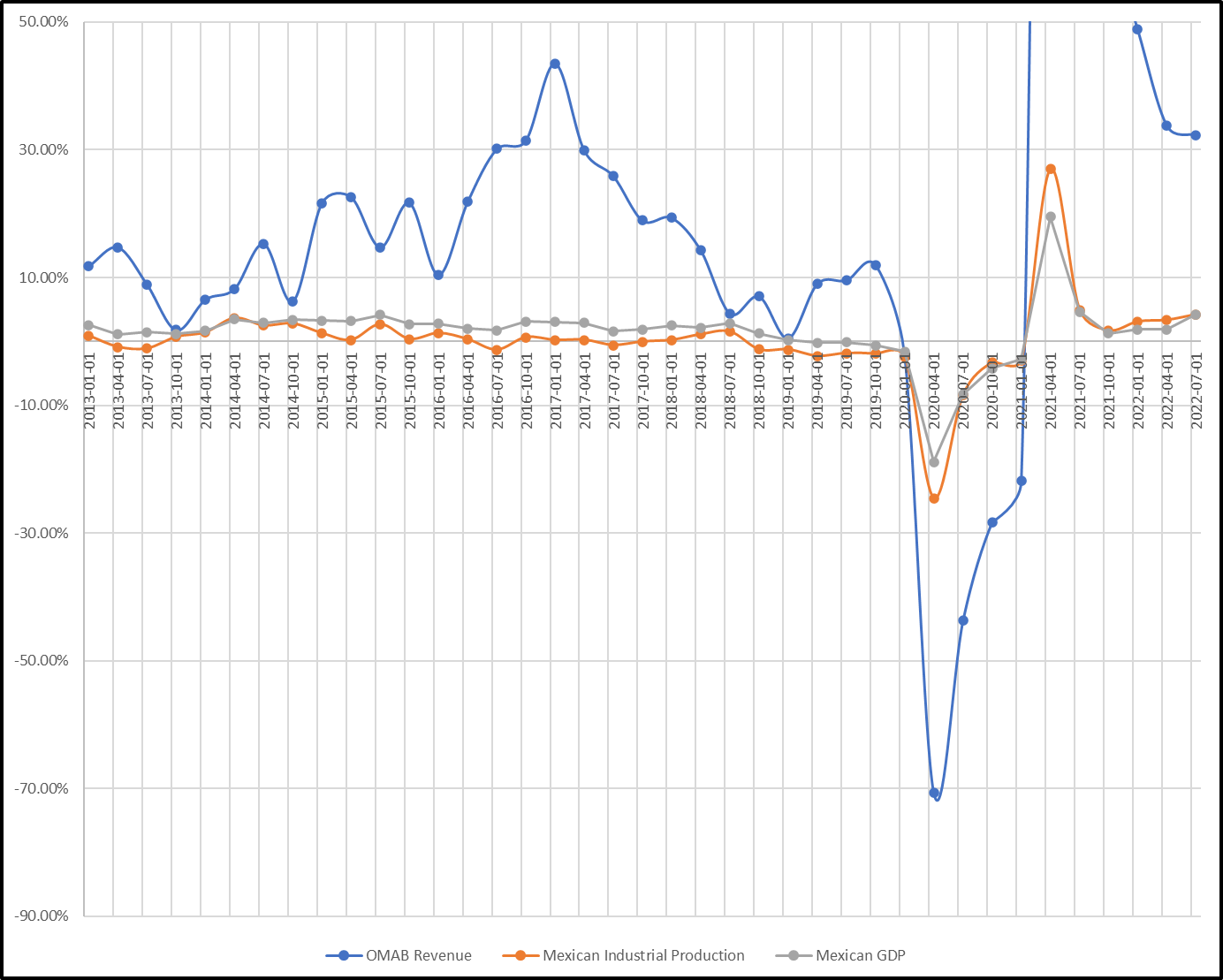

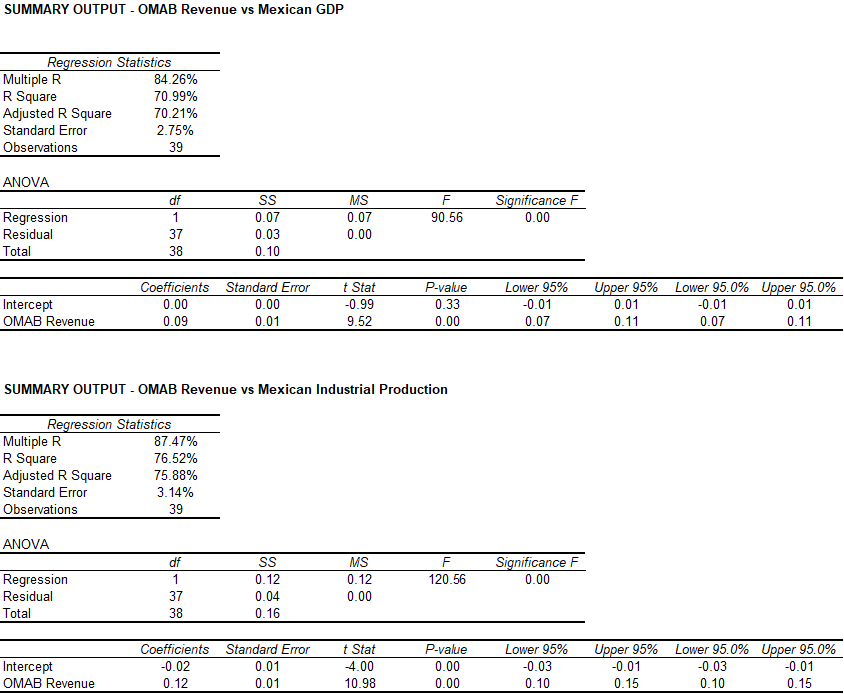

Returning to OMAB. Just how much exposure does OMAB have to the Mexican economy? Well here is the company’s quarterly YoY (year over year) revenue growth versus Mexican real GDP and industrial production for the last decade. I’ve also included a simple regression as well:

Mexican GDP and Industrial production growth rate alone explain ~70% and ~75% of OMAB’s revenue growth rate (nothing is perfect after all). And just by looking at the data and chart, you can see just how much “torque” OMAB has to the Mexican economy and manufacturing. Converting to numbers, OMAB has a ~7.5x beta (i.e. sensitivity).

So if you’re bullish on Mexican GDP and manufacturing, OMAB is a great way to play it! But many shareholders have already come to recognize this and have been bidding up the share price as we saw in the price charts at the beginning.

But wait, there’s more

Not only has OMAB increased its revenues from ~3 billion (Mexican Pesos) in 2012 to almost 11 billion today (a ~12.3% CAGR), but they’ve been consistently and extraordinarily profitable along the way. They’ve been so profitable that it would make many of the vaunted technology/SaaS companies jealous.

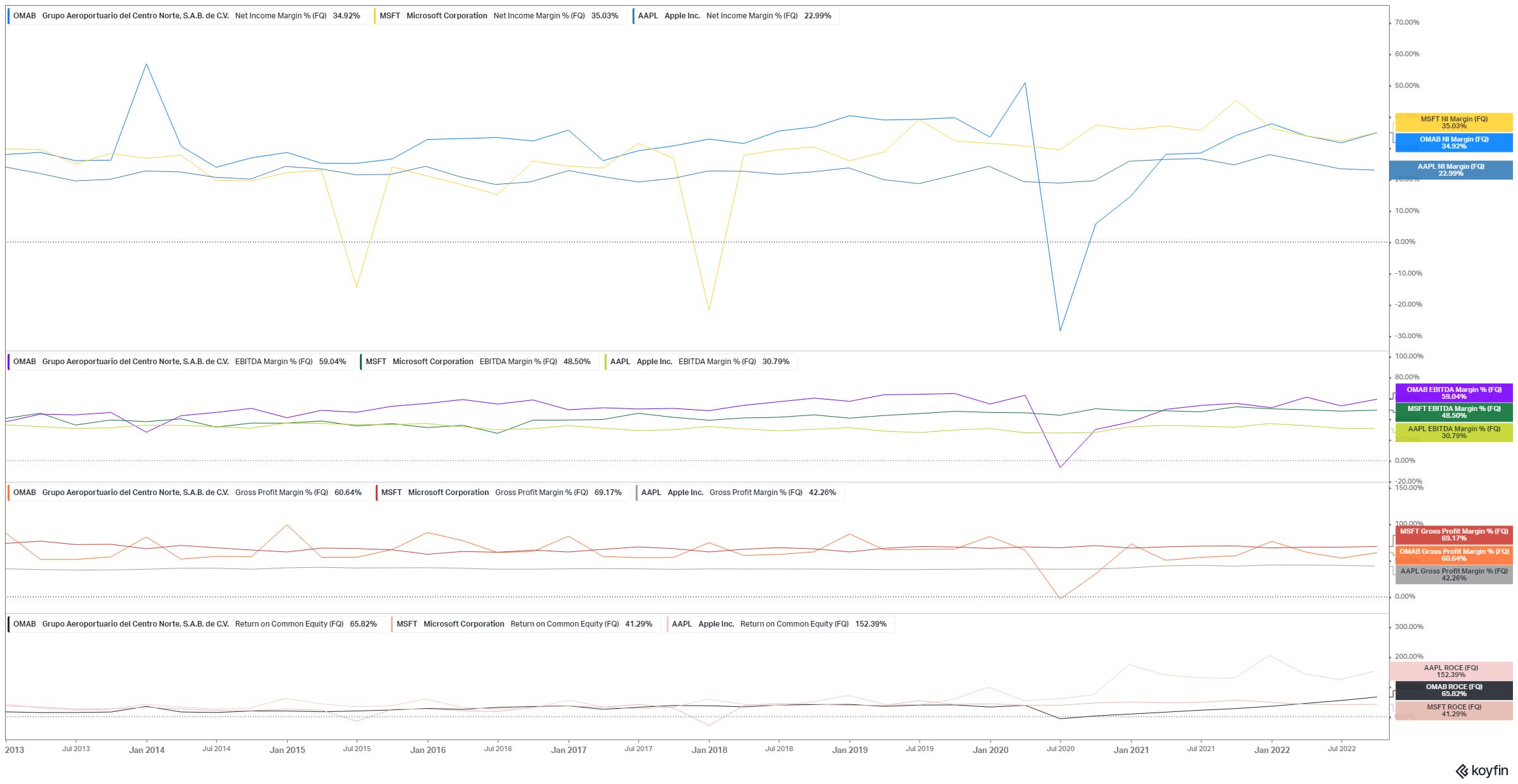

Here are graphs on OMAB’s gross profit margin, EBITDA margin, net income margin, and return on common equity versus Apple and Microsoft:

The fact that you can compare the profitability of OMAB versus two of the most profitable companies in history is stunning. Even more surprising is just how well OMAB holds its own.

This level of profitability does make me nervous about how sustainable it is long term though (something which I’ve written about before).

At least for now, OMAB’s management has been reinvesting much of the profitability back into the business to grow. They have an ambitious CAPEX growth plan for the next five years and it’s all internally financed. Much like CCU, the Chilean brewer that I highlighted before, per capita consumption in LATAM is much lower than the US or Canada. While there’s no way that it will reach the US levels in any meaningful investment timeframe (if ever), it still gives a great runway for future growth.

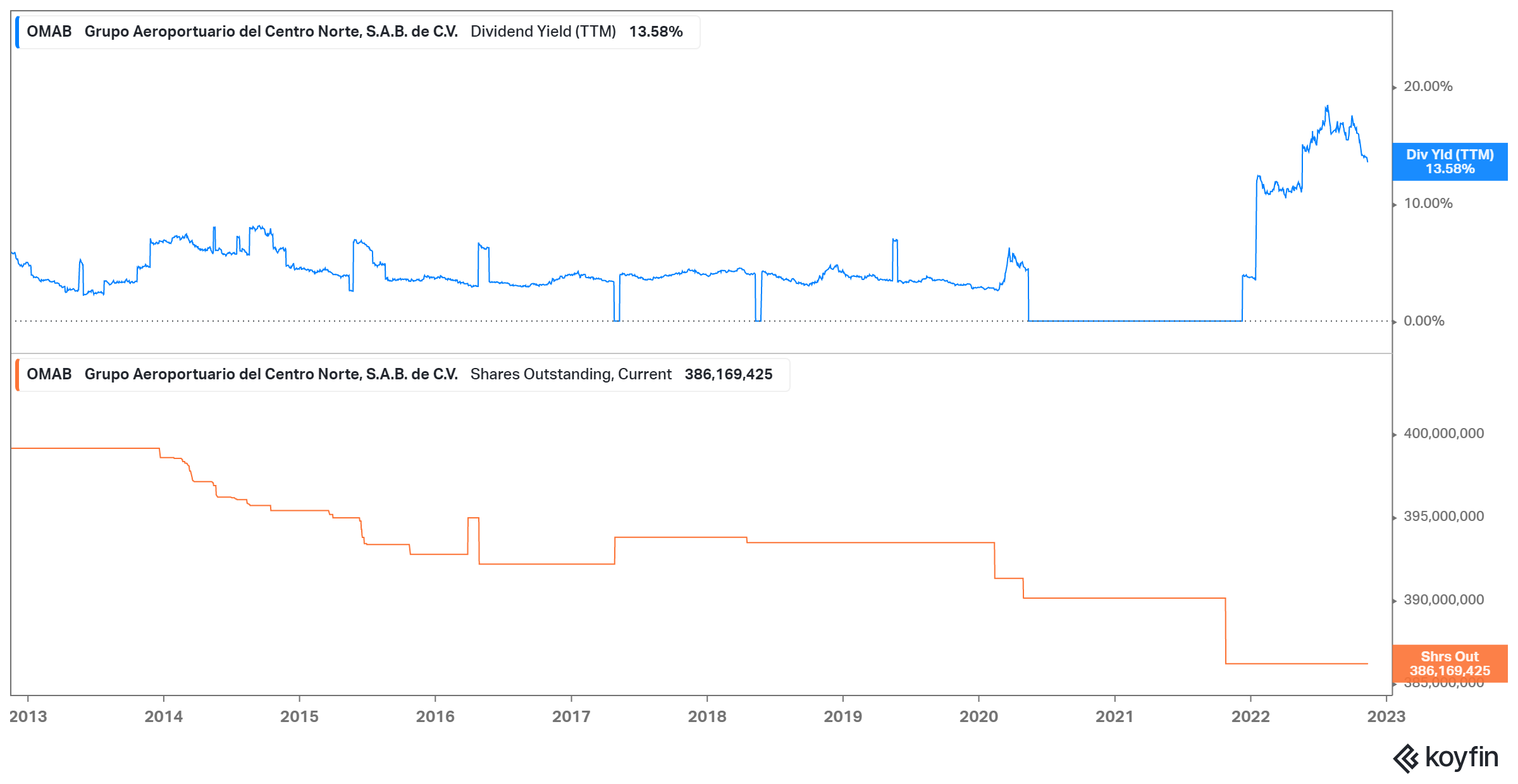

Management has also been returning capital to shareholders for well over a decade. Historically, OMAB has paid a dividend of ~3.5% - 5.5% while also very slowly (and opportunistically) repurchasing shares. Over the last decade, total shares outstanding have decreased by ~3.5%, which isn’t spectacular but at least it’s not growing (unlike many companies).

The company’s current return of capital framework is still largely focused on a base dividend plus special dividends to distribute out “excess earnings” which is quite common with LATAM companies.

So What’s It Worth (And Is It A Buy)?

This is obviously the hardest question to answer. Using a dividend discount model as well as a free cash flow model, I can get to a value of more than USD$100/share pretty easily. Meanwhile, the US-listed ADR is currently trading at just around USD$70/share. This would imply that there’s still another 50%+ of upside and making the shares still quite attractive to buy.

But, there’s a problem.

I still think there will be a mild recession in 2023. As a thought experiment, let’s say that US real GDP contracts by 1% to 1.5%. Mexico’s GDP is closely tied to that of the US and has a beta of about ~1.5x. So that would imply that Mexican GDP would decline by ~1.5% to 2.5%.

As I mentioned above, OMAB’s revenue beta to Mexican GDP and industrial production is around 7.5x. So that would imply that revenues decline by ~12.5% to ~20%.

So just to be safe, I assumed in my model that revenues would fall by 20% in 2023. We’d see a bounce back in 2024 and then further growth from 2025 to 2027 and beyond.

But here’s the dilemma. If the markets start to price in revenue down 20% next year, do they look past it and take a “long-term view”? Or will be a case of “sell first, ask questions later”?

My guess, and considering the extent of the move in the share price, is probably the latter. Investors will head for the hills which is why I’ve been hesitant to chase the share price here.

In many ways, this feels similar to another company that I wrote about back in August, Green Brick Partners. I highlighted the US homebuilder as a great long-term opportunity.

But at the time I cautioned in chasing the company’s shares as they had almost doubled off its June lows (were trading around $30/share at the time of publication). Of course, mortgage rates jumped and US real estate slowed dramatically since then. The stock is now at ~22.60/share which is a much more appealing entry point.

Zooming way out on OMAB’s share price, it’s a series of “staircases up and elevators down”.

So for me, I’m going to keep this stock on my watchlist and wait for a pullback. There’s always a risk that OMAB could be like the 2010s FANG names; where there’s never really much of a pullback and keeps grinding higher. But that’s a risk that I’m willing to put up with.

Disclosure: At the current time of publication, I have no beneficial interest in the above-mentioned securities. I may change my holdings at any time post-publication.

Disclaimer: This newsletter and/or any other articles that I publish should not be construed as investment advice. None of the strategies or securities mentioned should be considered as an investment recommendation to buy or sell. I am not an investment advisor and I highly recommend that anyone considering this investment strategy or any of the securities first consult with a registered investment advisor to assess both the suitability and risk of any strategies or securities that are mentioned.